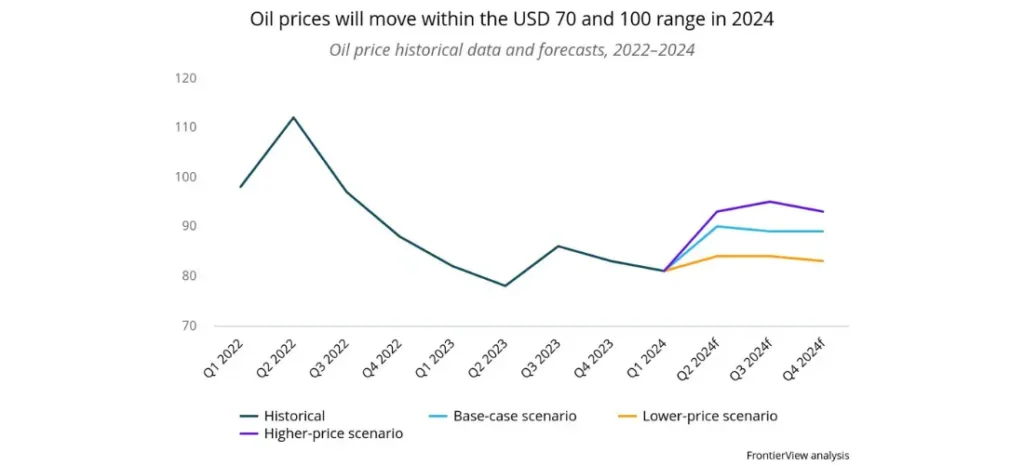

Our new base case assumes Brent crude will average USD 87 over the course of 2024

While global oil markets have come into better balance in the past 18 months, they remain subject to disruptions, notably from geopolitical events. Given the uncertainty around the global supply of oil, B2B multinationals who rely heavily on petroleum products as a source of inputs should continue to engage in scenario planning when it comes to their input costs. B2Cs, particularly those in the discretionary goods space, should monitor the trajectory of oil prices; higher spending at the pump will displace spending on other categories—this will be particularly acute in commodity-importing countries in the Middle East and Africa, as well as in Southeast Asia, and Latin America.

Overview

- Oil prices have rallied in recent weeks, reaching USD 90/barrel (Brent crude), which marks a rise of nearly 20% since the start of 2024.

- Tensions in the Middle East have been increasing following an Israeli strike on an Iranian embassy in Syria. At the same time, Russian output has fallen by around 400,000 bpd following Ukrainian attacks on Russian refineries.

- Meanwhile, OPEC announced it was extending its output cuts to Q2 2024, and likely beyond.

- In the world’s major economies, macroeconomic data has been strengthening; in China, while overall activity remains sluggish, industrial production is picking up, as evidenced by the first PMI expansion in six months. In the US, consistently strong labor market data points to continued economic resilience, while several markets in Europe are experiencing improving manufacturing conditions.

- We have revised up our base-case forecast for Brent crude from USD 82 to 87 for 2024.

Our View

Following several weeks of quiet where Brent hovered around the low USD 80s, oil prices have rallied to reach the USD 90 threshold for the first time in six months.

The main culprit is continued geopolitical tensions and uncertainty in two of the world’s major oil-producing regions, Russia and the Middle East. Both situations show few signs of abating and, if anything, the risk to oil supply has ticked up. In Russia, Ukraine has launched drone attacks on oil refineries, which Russia will struggle to repair given ongoing sanctions. In the Middle East, the increase in tensions is fueling fears that Iran could get more directly involved in the conflict.

Supply is tightening elsewhere: alongside the expected continuation of OPEC cuts, US sanctions on Venezuelan oil exports will be reimposed this month after President Nicolas Maduro’s government failed to implement electoral reforms. In an unexpected move, the Mexican government also announced that it would be reducing its exports of crude oil to global markets in an effort to produce more gasoline domestically. In the US, producers will struggle to replicate the drastic increase in oil production experienced in 2023.

Tightening supply comes amid an improving growth outlook for the global economy. The global manufacturing sector posted its highest PMI since July 2022, buoyed by increases in new orders; manufacturing conditions will improve throughout 2024, as demand recovers and interest rates fall. The Chinese manufacturing sector in particular will continue to be a resilient source of oil demand, as the country places additional emphasis on boosting industrial production. Air travel, which has already surpassed pre-pandemic levels in terms of passenger numbers, will continue to grow strongly in 2024, particularly in Asia.

The question now becomes: to what extent will higher oil prices derail the downward trend of inflation, and therefore interest rates? We expect higher oil prices to have an impact, but a minimal one. Most central banks are now focused on the trajectory of so-called “core” inflation, which excludes oil prices. Still, higher prices at the pump will continue to displace spending on other categories and delay the recovery of purchasing power, notably in markets where gasoline represents a higher proportion of the consumer basket.

Given the volatility in oil markets in recent years, we continue to assess a range of scenarios when it comes to oil prices in 2024. Our higher-price scenario (USD 91) assumes significant overperformance of the global economy, paired with a marked escalation in the Middle East conflict, which would greatly increase the risk premium on Brent. Our lower-price scenario (USD 83), meanwhile, assumes significant delays to monetary easing from central banks, which would weigh on oil demand and allow a more balanced oil market.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.