Impacts will vary across industrial sectors as overcapacity persists

The collapse of China’s real estate sector has led to a broad economic slowdown marked by weak domestic demand. In response, government policies have focused on boosting production over consumption, creating a significant supply-demand imbalance. This approach has resulted in overcapacity in multiple industries, a critical issue in China’s business environment that is spilling out to the global economy. To help businesses navigate this challenge, we have developed an index using official Chinese data. This tool tracks and analyzes trends in overcapacity across various sectors, offering vital insights for strategic decision-making.

Business Implications:

Overcapacity continues to pressure profit margins to record lows for Chinese manufacturers, increasing their vulnerability to fluctuations in production costs. B2B companies should expect sustained pricing pressure, manage their accounts receivables conservatively, and incorporate flexibility in their financial forecasting. Where possible, they should explore opportunities in less affected industries.

B2B firms that are exposed to sectors with significant overcapacity should act at both the regional and global levels to monitor product outflows from China and potential protectionist measures in their operating regions. Rising trade tensions between China and Western countries are likely to introduce further complications for multinationals in these industries.

B2C companies are likely to see a mixed impact from China’s industrial overcapacity. Firms that face direct competition from Chinese companies should brace for intensified price pressure from local firms, which remain focused on securing market share over profit, while those that source components or intermediate parts from China should evaluate opportunities to cut their COGS, either through renegotiation or by changing suppliers.

Overcapacity levels overall in Q2 2024:

China’s overcapacity issues showed signs of reverting to the less severe levels observed in Q4 2023, following a notable deterioration in Q1 2024. This improvement primarily stemmed from robust external demand, which compensated for faltering domestic demand. Export growth in Q2 2024 showed an uptick from the previous quarter. However, with tariffs rising and the US economy weakening, we anticipate a drop in external demand. Coupled with the lack of effective policies from the Chinese government to stimulate domestic demand, we do not expect China’s overcapacity to see significant improvement in the near term.

Overcapacity levels across industries in Q2 2024:

Severe overcapacity: Industries such as Non-metal Mineral Products, Automobile, Food, and Electric Machinery & Equipment continue to struggle, with overcapacity indices remaining below -2 for three consecutive quarters. The Food industry, in particular, has seen a consistent decline in its overcapacity index, indicating worsening conditions.

Moderate overcapacity: Industries including Textiles, Computer, Communication & Other Electronic Equipment, Pharmaceuticals, Ferrous Metal Smelting & Pressing, and Chemical Material & Product exhibit moderate overcapacity, with indices around -1. Notably, Textiles, Computer, Communication & Other Electronic Equipment, and Ferrous Metal Smelting & Pressing have shown signs of improvement over the past two quarters.

No overcapacity: Industries such as Special Equipment, Chemical Fiber, General Equipment, and Non-Ferrous Metal Smelting & Pressing are performing well, with indices at around 0 or higher.

Research Methodology:

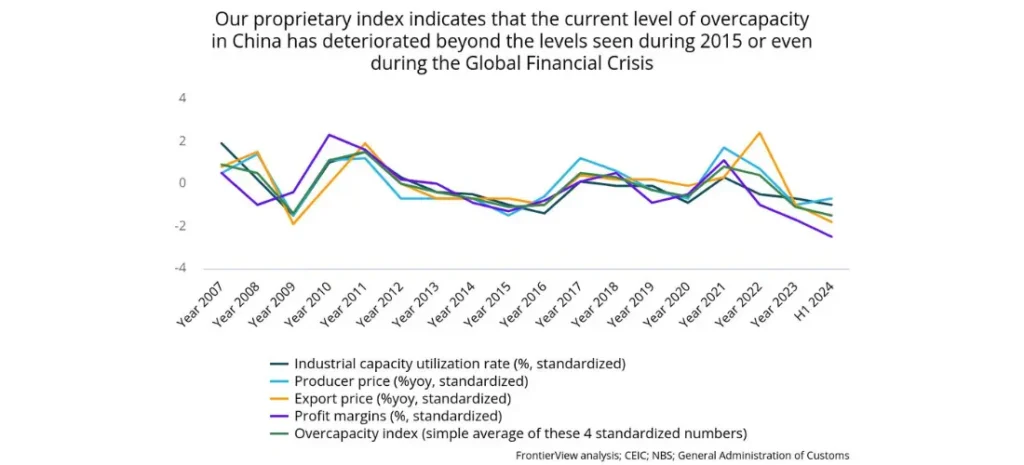

Our proprietary “Overcapacity Index” quantifies overcapacity across various industries in China, utilizing a simple average of four standardized official data points: industrial capacity utilization, profit margins, producer price growth, and export price growth. Standardization involves subtracting the pre-pandemic mean from the values and then dividing by the pre-pandemic standard deviation. An index value rounded to -1 or lower indicates overcapacity, while values rounded to 0 or higher suggest no overcapacity.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.