The territory’s sluggish post-pandemic recovery has made its government reluctant to reduce fiscal expenditure

B2C companies should not revise their sales projections based solely on this budget, despite the upward revision of our GDP growth forecast for 2024. This is because the budget’s reduction in various subsidies and tax rebates for residents will offset the impact of higher economic growth on consumer spending. Firms that depend heavily on tourist spending should exercise caution in building their forecasts as well since the outlook for tourism remains muted, despite the government’s increased budget for more events to attract tourists. This is because the recent implementation of visa-free entry policies for Chinese tourists by several Southeast Asian countries, such as Malaysia, Singapore, and Thailand, is expected to divert a large number of high-spending mainland tourists away from visiting Hong Kong, placing further pressure on B2C firms’ sales.

In contrast, B2B companies will likely see more opportunities because of the government’s plans to stimulate infrastructure building and enhance investments and subsidies across various sectors. These sectors include artificial intelligence, microelectronics, life and health technology, advanced manufacturing, and new energy technology. In addition, healthcare companies will likely see more opportunities as the government has promised to revise regulations concerning drugs and medical devices in order to expedite their clinical applications.

Overview

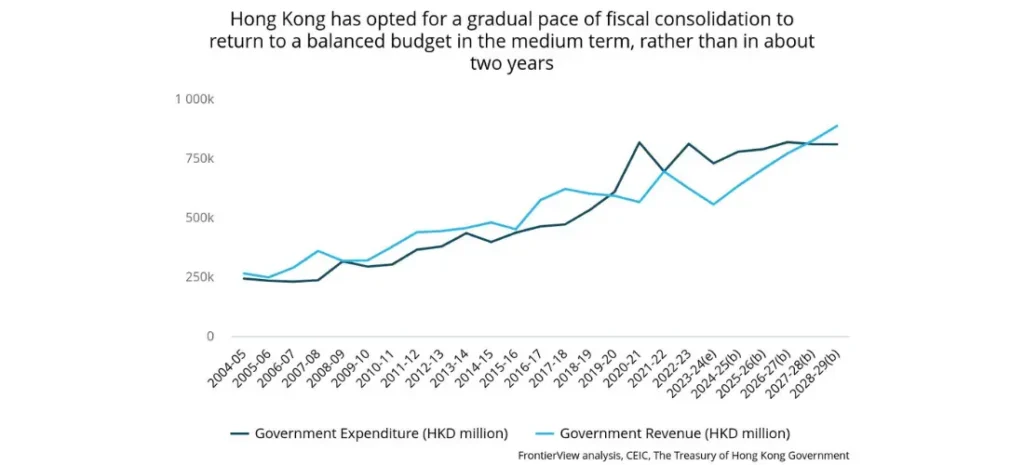

- In the fiscal year 2024–25, Hong Kong is set to increase its fiscal expenditure and sustain a fiscal deficit, with fiscal expenditure projected to rise by 6.7% YOY (previous fiscal year: -10.2% YOY), and the fiscal deficit expected to reach USD 18.4 billion (previous fiscal year: USD 22.2 billion).

- According to the budget proposal, Hong Kong’s fiscal deficit is expected to persist until the fiscal year 2026–27, a shift from the earlier projection of 2024–25 outlined in the previous budget.

- Fiscal expenditure for the fiscal years 2025–26 to 2027–28 is projected to increase by an average of 1.4% annually, markedly below the 3.6% growth outlined in the preceding budget.

- The distribution of consumption vouchers will be halted this fiscal year, together with a reduction in various subsidies and tax rebates. As a result, compared to the previous fiscal year, the average annual disposable income per citizen will be reduced by approximately USD 1,282 (equivalent to half of the median monthly income).

- An additional USD 139.7 million has been allocated to bolster tourism development and the hosting of events, including monthly fireworks and drone displays.

- The special stamp duty, buyer’s stamp duty, and new residential stamp duty on residential properties have been abolished, and regulations on property mortgage loans will be eased.

Our View

Hong Kong’s economy is expected to improve in 2024 with our forecast on GDP growth revised up from 1.4% YOY to 2.3% YOY, but the mid-term economic outlook will likely deteriorate. The decision to extend the timeframe for achieving budgetary balance essentially amounts to ‘borrowing from the future.’ While increased fiscal spending in the next two years is anticipated to stimulate economic growth, it comes at the cost of the government needing to further curtail expenditures in subsequent years to return to budgetary balance. This reduced fiscal spending is likely to decelerate economic growth in the mid-term.

Hong Kong’s property market, a key pillar of the city’s economy, has been notably weak in recent years, and the prospects for a quick and substantial improvement are bleak. The abolishment of all residential stamp duties (roughly equivalent to 7.5% of the property price) should boost the demand for property purchases and stabilize prices, at least in the short term. However, given the ongoing wave of emigration in Hong Kong, an oversupply in the real estate sector, and an uncertain mid-term economic outlook, these policies appear insufficient to rebuild developers’ confidence and generate increased revenue from land sales.

The reality could be even grimmer because the budget’s projections for Hong Kong’s mid-term economic growth are almost certainly overly optimistic. The budget assumes an average annual GDP growth of 3.2% from 2025 to 2028, which is higher than the 2.8% achieved pre-pandemic from 2015 to 2018. Should GDP growth fall short of these assumptions, fiscal revenues are likely to fall short of government forecasts. In that case, to achieve budgetary balance on schedule, the government would need to further reduce spending, which in turn could adversely affect the economy.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.