Despite diminishing concerns about Europe’s energy supply, underlying risks continue to weigh on the outlook for 2024

While many of Western Europe’s acute risks in 2023, especially when it comes to energy security, did not materialize, risks will continue to weigh on the outlook for 2024. While these risks are not a part of FrontierView’s base case, they continue to necessitate a significant focus on medium- to long-term scenario planning. The fact that some of these risks stem from a mix of intra-EU and global factors also highlights the complicated operational environment that MNCs will continue to experience through 2024. Here are the most important potential events to monitor in Western Europe (beyond those mentioned in our global report):

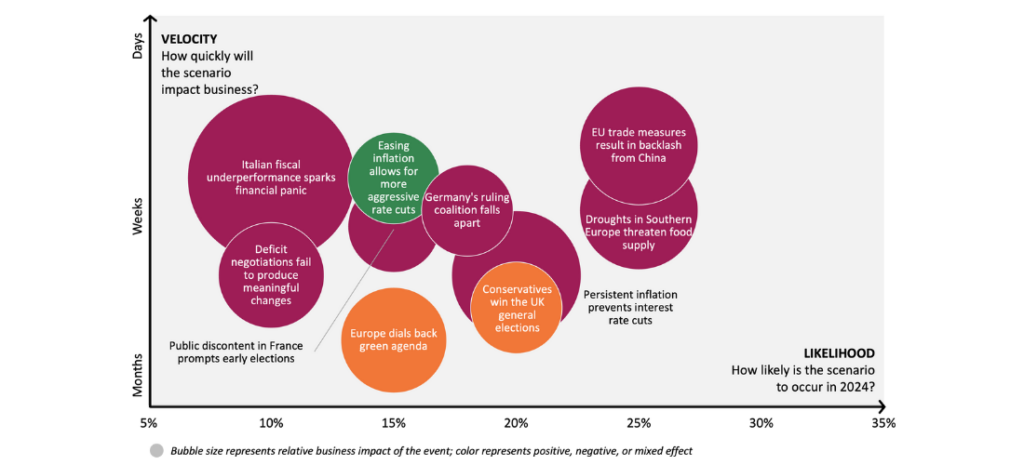

- Italian fiscal underperformance sparks financial panic (10%): Attempts to renegotiate the EU’s fiscal framework fail, and it becomes increasingly evident that Italy is set to miss its deficit targets. A downgrade of Italian bonds by rating agencies leads to a spike in the cost of new debt for Italy and makes servicing existing debt significantly more difficult. Financial panic spreads and affects French and Spanish long-term interest rates, exposing large and vulnerable banks, and forcing the European Central Bank (ECB) to introduce another bond-buying program to depress the spread in the 10-year bond yields, which leads to a notable easing in the EUR rate and inflation, followed by an eventual shallow recession through 2025.

- Droughts in Southern Europe threaten food supply (25%): Acute weather conditions across the globe and a heatwave during the summer months of 2024 lead to a notable shock to the agriculture sector in Southern Europe. Constrained global and European supply leads to another spike in food prices, which causes an uptick in headline inflation, preventing the expected gradual monetary easing and, in turn, depressing consumption across Europe.

- Deficit negotiations fail to produce meaningful changes (10%): Ongoing attempts to renegotiate the EU’s Stability and Growth Pact and introduce a set of fiscal adjustments to the requirements collapse, prompting the return of the previous 3.0%-of-GDP deficit target. The constraining nature of the rules severely hampers the ability of governments to introduce fiscal amendments and to introduce measures to support local economies, resulting in a more pronounced budgetary tightening. In some instances, governments refuse to comply with the deficit and debt rules, leading to increased tensions between policymakers and the European Commission (EC), which dampens investors’ confidence.

- EU trade measures result in backlash from China (25%): Ongoing attempts to de-risk and localize European supply chains, combined with individual governments’ attempt to support domestic industries to taxes and levies, especially when it comes to EV manufacturing, prompt a trade response by China, which may involve stricter regulations on EU companies operating in China or targeted trade measures against European exports. The situation leads to a tit-for-tat exchange between China and the EU, leading to supply-chain disruptions and a drop in investments from China, which negatively affects European exports and raises the prices of imports.

- Europe dials back green agenda (15%): A spike in energy prices leads to another inflationary shock that exacerbates cost-of-living challenges and results in pushback to the EU’s Green Deal from businesses, who emphasize the cost of compliance’s impact on the price of goods. Far-right and center-right parties across the EU see a political opening and manage to capitalize on their growing popularity during the EU parliamentary elections. The implementation of the Green Deal is hampered by pushback on both the national and EU levels, resulting in delayed or dropped aspects of the proposals, and leading to a reduction in the environmental conditionalities of EU-related funding.

- Persistent inflation prevents interest rate cuts (20%): Elevated commodity prices and rising food costs continue to weigh on the inflationary outlook, preventing key policy rate cuts through Q1–Q3 2024. Inflation across the eurozone picks up again through Q2 2024 and remains in the 3.0–3.5% YOY range, leading both the ECB and the Bank of England (BOE) to signal that lending rates will remain higher for longer, leading to a dampened lending activity outlook, and depressing economic growth through H2 2024.

- Conservatives win the UK general elections (20%): The Conservatives manage to snatch a narrow win over Labor, following the introduction of a more ambitious Spring 2024 budget and supported by easing macroeconomic pressures, especially inflation.

- Public discontent in France prompts early elections (15%): Ongoing fiscal reforms and tighter budget expenditures, plagued by a fractious legislature, result in another wave of public discontent across France. The use of presidential executive powers to pass through legislation emboldens far-left and far-right parties, further fueling existing social pressures and prompting the government to call new elections, resulting in a period of prolonged policy unpredictability.

- Easing inflation allows for more aggressive rate cuts (15%): A pronounced easing in commodity prices and subsiding food inflation lead to a more significant moderation in headline inflation. The normalization in the price environment prompts the ECB and the BOE to begin easing their key policy rates as early as mid-Q2 2024 and pursue additional cuts through H2 2024, leaving policy rates in the 3.75–4.25% range at the end of 2024. The substantial easing in lending rates leads to a more pronounced recovery in lending activity through H2 2024, paving the way for a much more substantial uptick in activity through Q4 2024 and 2025.

- Germany’s ruling coalition falls apart (20%): Existing disagreements over budget expenditures, exacerbated by a budget transfer ban by the constitutional court, result in deep divisions within the ruling coalition and prompt the FDP and/or the Greens to exit the coalition, which is followed by a period of heightened policy uncertainty, and raises the prospects of extreme political parties finding a stronger presence in parliament.

Watch a video overview of the WEUR Events to Watch for 2024

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.