Growth will pick up in H2, followed by a more pronounced rebound in 2025

B2Cs will see increasing opportunities region-wide into H2 2024 as consumption continues to trend upward. Consumers remain broadly cautious, but confidence is gradually increasing amid an ongoing moderation in inflation, with further opportunities likely to present themselves into H2 2024.

B2Bs should monitor region- and sector-specific developments in the near term, with industry broadly remaining weak.

B2Gs should continue to monitor opportunities on a national basis, with an increasing trend of fiscal consolidation generally hampering demand in 2024. However, large disbursements of EU funds continue to offer opportunities across Central Europe (CE) within infrastructure development.

Multinationals should further ensure strong positioning ahead of H2 in anticipation of broader monetary easing, which will support both consumption and industry alike in H2 2024.

Overview

- Preliminary Q1 GDP estimates released so far indicate Q1 performance is stronger across CE than Q4 2023. Hungary grew 1.1% YOY in Q1 from stagnation in Q4 2023; meanwhile, the Czech Republic continued to grow modestly at 0.5% YOY in Q1 2024 from 0.4% YOY the quarter prior. Lithuania exited recession in Q1 2024, growing 0.8% YOY.

- Poland and Serbia experienced rapid retail sales growth in Q1 2024, recording YOY increases of 5.1% and 6.5%, respectively. Meanwhile, Romania reported an average retail sales growth of 6.5% YOY in January and February 2024. However, Hungary exhibited more modest growth, with an average monthly retail sales growth of just 0.85% YOY, mirroring weaker YOY performance in the Czech Republic (2.4%) and Slovakia (3.6%) during the same period.

- Industrial production continues to flounder in CE, following a reversal in what was increasingly looking like an industrial recovery in Poland and Lithuania, which saw YOY industrial output fall 6% and 3.4%, respectively, in March, following two months of growth.

- Elsewhere, industrial production growth continues to be tepid, with March output growing by only 0.7% YOY following three months of contraction in the Czech Republic and 0% YOY growth in Slovakia in February; Romanian output continued its downward trend, falling 2.2% YOY in February.

Our View

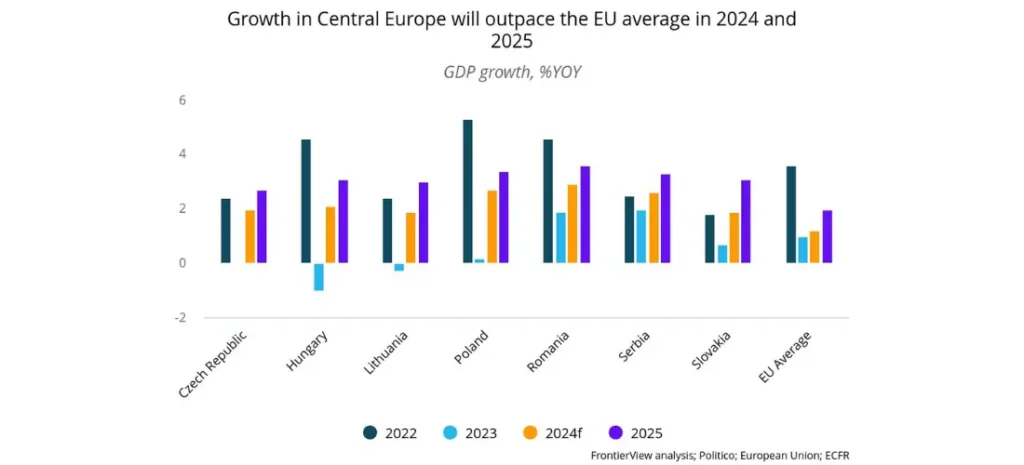

We expect moderately strong growth across CE to outpace broader growth across Europe throughout 2024, with a higher average growth of 2.4% for 2024, and 3.2% in 2025, against the European average of 1.2% and 2.0%, respectively. Still, both upside and downside threats have potential to significantly alter annualized growth into 2025, but in either eventuality, CE should see greater growth prospects than the European average.

The primary catalyst for growth in the region this year continues to be the resurgence in consumer spending, fueled by robust double-digit wage growth across CE. While first-quarter indicators suggest a promising rebound in consumer activity across the region, with all countries reporting growth in retail sales in 2024 following contraction in Q4 2023, the pace of this recovery varies among nations. Although this trajectory signifies progress, it also reflects lingering consumer apprehension, which remains prevalent across the region. As we progress into Q2 2024, we anticipate an improvement in consumer confidence, translating into an increased consumption.

Another key driver of the consumption rebound is the ongoing trend of moderating inflation across the region, with the consumer price index (CPI) nearing or falling within central bank tolerance bands. However, the potential resurgence in inflation later this year poses a notable risk to consumer spending. Factors such as diminishing statistical effects and the expiration of support measures implemented in recent years threaten to reverse the downward trajectory in inflation. Additionally, recent currency depreciation in the Czech Republic and Hungary, where currencies have fallen 4.86% and 5.48%, respectively, against the dollar since the start of 2024, is driving up import costs, while robust wage growth continues to exert inflationary pressures, particularly in the service sector.

Despite more encouraging trends in consumer spending, industrial activity remains subdued across CE. While Hungary and the Czech Republic showed minor growth in industrial activity in February, Romania’s industrial sector continues to decline due to weakening external demand. In Poland and Lithuania, initial signs of recovery following robust growth in January and February abruptly halted in March, whereby industrial production unexpectedly plummeted, primarily driven by a sharp decline in mining output, alongside considerable falls in manufacturing output. Although March’s downturn may be partly attributed to calendar effects, it underscores the lingering concerns that short-term activity has yet to fully rebound. We still anticipate a rebound in industrial activity in H2 however, supported both by easing interest rates and by stronger external demand in Europe, as the wider region sees a pickup in activity.

Government spending dynamics across the region display a nuanced pattern, overshadowed by persistently high budgetary deficits and escalating debt-to-GDP ratios. In Poland, a robust expansion in government investment is anticipated for the current year, buoyed by the recent disbursement of EUR 6.2 billion in EU funding, earmarked primarily for infrastructure development. Similarly, Romania is experiencing a surge in investment propelled by unprecedented levels of EU funding, marking a remarkable 70% increase in investment from January to March 2024 compared to the preceding year. Conversely, Hungary grapples with mounting budgetary strains aggravated by escalating debt costs, culminating in the collapse of the 2024 budget. A revised budget is on the horizon by the end of Q2 2024, with strong indications pointing toward imminent fiscal consolidation measures.

The broader economic trajectory for 2024 hinges significantly on external factors, particularly the timing and magnitude of global interest rate adjustments. These adjustments will afford European central banks the flexibility to enact further rate cuts, bolstering industrial resurgence and reinforcing consumer spending. Furthermore, the response of Europe, notably Germany, to these rate cuts will be pivotal, as any uptick in German industrial activity could catalyze growth in export demand from CE.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.