While Asia Pacific is likely to post strong growth relative to other regions, most risks tilt to the downside

In addition to the pertinent risks outlined in our Global Events to Watch for 2024 (e.g., China Blockades Taiwan, Chinese Growth Decelerates Sharply), companies should take note of several additional risks that could impact their operations in the region. While these events span the realms of economics, politics, and security, they generally tilt to the downside, suggesting more potential for disruption than opportunity. Here are the most important potential events to monitor in APAC (beyond those mentioned in our global report):

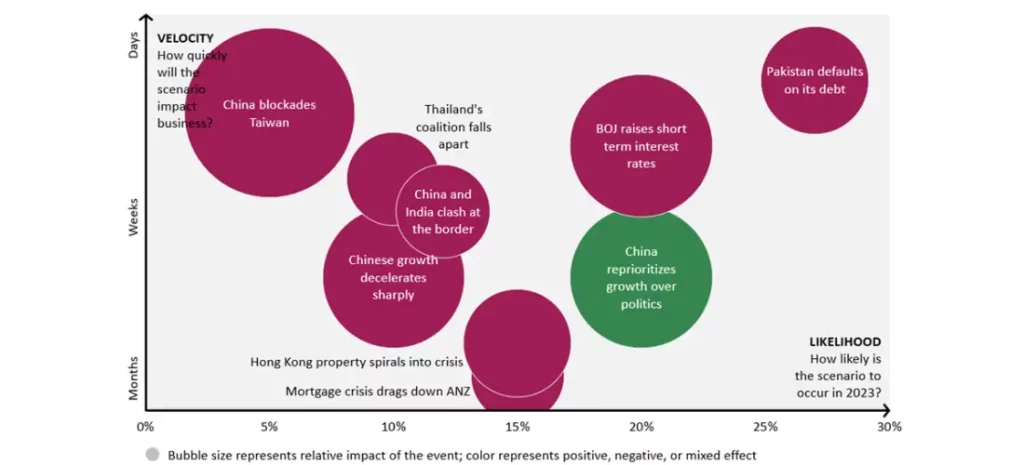

- China blockades Taiwan: While Beijing clearly intends to reunite Taiwan and the Mainland, we believe it’s unlikely to take direct action in 2024. China is not currently operating from a position of strength militarily or economically. However, if Beijing were to move on Taiwan next year, it would likely begin with a blockade to soften its target. In this scenario, China would establish air and naval blockades around the island, gradually cut its connections with the outside world, and strangle its economy. While other countries—namely the US and select allies—would protest and possibly run the blockade to provide crucial supplies, assistance would be limited. Companies would come under immense pressure to limit their investment on the Mainland while protecting their global operations.

- Chinese growth decelerates sharply: China is starting to bolster its economy with fiscal and monetary stimulus, suggesting that it will put a floor under growth. As a result, we believe it’s unlikely that the country will experience a sharp deceleration. However, if the government does not continue moving aggressively, the faltering real estate sector could drag down the economy due to falling housing prices, dwindling transactions, and increasing developer defaults. This would weigh heavily on industrial production, which is already under pressure from weak global demand. It would also further undermine local government revenues and therefore local government spending. Finally, it would cause consumption to slow as households saw their wealth levels decline, job security fade, and earnings prospects deteriorate.

- China reprioritizes growth over politics: While China is starting to bolster its economy with fiscal and monetary stimulus, its measures have been limited due to leaders’ concerns about debt, moral hazards, and “welfarism.” Were political priorities in Beijing to change, the government could easily accelerate growth through a range of measures (e.g., removing property investment restrictions and saving developers, actively relieving pressure on local governments’ finances). In this scenario, industrial production would accelerate, particularly for construction products; local government spending would increase as revenue pressures eased; and consumption would accelerate as households gained confidence in their earning prospects, job security, and real estate–linked wealth.

- Hong Kong property spirals into crisis: After falling substantially from their 2021 peak, we expect Hong Kong’s property prices will begin to stabilize as the US Federal Reserve begins to cut interest rates in 2024. However, if US rates don’t decrease as anticipated (or, even worse, if they rise higher), a further dip in Hong Kong’s property prices will be unavoidable, and the threat of continuous declines in housing prices, coupled with the territory’s uncertain long-term outlook, could precipitate panic selling among homeowners. In this scenario, a drastic drop in property prices would lead to a swift rise in negative equity cases and weigh heavily on domestic consumption. As land sales deteriorated further, government revenues would decline, and with them spending on services such as social welfare and healthcare provision.

- Mortgage crisis drags down ANZ: Interest rates in Australia and New Zealand have rapidly risen to the highest they have been in decades. The record pace of monetary tightening has caught a large proportion of households, particularly those that bought their homes during the pandemic, completely off guard. Already, some households are falling behind on their mortgage payments or defaulting on them altogether. Under our base-case scenario, we do not expect the magnitude of defaults to be large enough to raise cause for concern. However, the risk of a crisis still looms over the region, especially as more mortgage holders flip onto higher interest rates. In an event where a large portion of mortgage holders default on their loans, a series of ripple effects would disrupt the regional economy. Consumer spending would drop, property prices would tumble, and banks highly exposed to the sector would suffer―thus stifling new investments.

- The BOJ raises short-term rates: Conditions today are stronger than ever for a hike in short-term interest rates in Japan. Inflation is higher than it’s been in decades, the yen has fallen past 150 against the USD, and wage growth is picking up. Yet, a rapid hike in short-term interest rates is not part of our base-case scenario due to the risks associated with such a move. Inflation in Japan is due to supply shocks in the global economy, not excess demand within the market. In this environment, raising interest rates would drive down tepid consumer demand further and stifle growth. Higher rates would lead to other disruptions as well, with downstream effects that would be impossible to predict. The burden of higher interest rate payments on its mountain of debt would strain the Japanese government. Financial markets and other businesses accustomed to rock-bottom interest rates would have to change how they operate. Not only would higher interest rates stifle new investments and fundamentally redefine “ROI” in the Japanese context, but they would also raise the potential for crippling shocks to both domestic and international financial markets.

- Pakistan defaults on its debt: Pakistan narrowly escaped a default earlier this year after clinching a last-minute deal with the International Monetary Fund (IMF). Nevertheless, there is still a distinct possibility that the country will default on its debt in 2024. In this event, Pakistan would fail to meet the IMF’s stringent requirements for additional funding needed to keep the economy afloat. The nation’s ongoing political crisis would worsen, and elections would be delayed indefinitely, prompting major protests around the country and a lack of focus on policies required to get the economy back on track. As a result, we would expect widespread erosion of confidence among consumers and investors, severe depreciation of the rupee, extreme inflation, restriction of capital movement, and supply shortages, creating a very difficult operating environment for businesses.

- China and India clash at the border: India-China border relations have been intermittently fraught with clashes over the past few decades. The latest bout in 2020 turned deadly and involved some retaliatory trade measures by India. In the event that border tensions see major escalation again, we would likely see some form of trade penalties (e.g., intensified border checks, tariffs, import bans) from both sides. Firms operating in India would be more affected than those in China, considering that India is heavily dependent on China for critical imports in sectors like electronics, pharmaceuticals, and chemicals. As a result, companies operating in or serving these sectors would likely experience supply chain disruptions and demand volatility.

- Thailand’s coalition falls apart: After a bruising election followed by long negotiations, Thailand appears to have a stable government. The military establishment and the Pheu Thai Party are uncomfortable bedfellows, but they do not have easy alternatives if they want to stay in power. Nevertheless, considering that the two blocs have been rivals for well over a decade, there is a low-likelihood risk that infighting in the government could lead to a collapse of the recently formed coalition, resulting in a call for fresh elections. In such a scenario, election proceedings would be prolonged—similar to those Thailand just witnessed—as no party would garner enough support for a smooth victory. During this period of political stasis, the Thai economy would face major challenges, including widespread protests, weakening consumer and investor confidence, a volatile baht, policy uncertainty, and a likely delay in government projects.

Watch a video overview of the APAC Events to Watch for 2024

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.