Despite the expected slowdown finally having arrived, Brazil remains a market of opportunity. Amid a resilient yet decelerating consumer landscape, multinationals should continue targeting wealthier consumers less prone to ongoing price sensitivity. Multinationals should also consider minimizing price increases to protect market share among lower- and middle-income consumers. Within the B2B sector, companies should remember that investment recovery will be slow and mostly materialize in H2 2024; therefore, ensuring the industry-level target properly reflects specific segment demand outlooks will be critical. Finally, despite the beginning of monetary easing, multinationals should prepare for still-high interest rates throughout 2024, creating additional financial strain on actors across the supply chain.

Overview

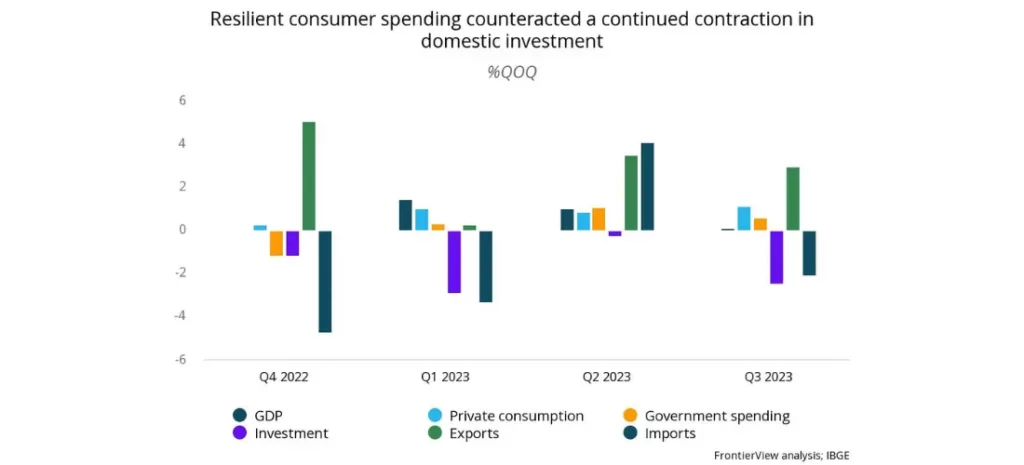

Brazil’s economy grew 0.1% QOQ in Q3 2023, decelerating from the stronger-than-expected results posted in H1 2023. The results were aligned with FrontierView’s expectations and slightly above market consensus, which forecasted a contraction of -0.3% QOQ. From the demand side, the positive highlight was private consumption, which posted its third quarter of growth, registering 1.1% QOQ, boosted by fiscal expansion and a resilient labor market. On the negative side, domestic investment saw another quarter of contraction (-2.5% QOQ), impacted by contractionary monetary policy. On the supply side, deceleration was observed across most sectors, but more forcefully so in agriculture (-3.3% QOQ), which was expected after significant growth registered in H1. Services grew 0.6% QOQ (down from 1% growth recorded in Q2), with most deceleration coming from transport activities. Lastly, output from Brazil’s industrial sector slowed to 0.6% QOQ (down from 0.9% registered in Q2), with stagnation in manufacturing and a strong contraction in construction.

Our View

While Q3 GDP confirmed an economic slowdown is beginning to take hold, Brazil’s economy still decelerated less than expected, with higher-than-expected consumption figures compensating for the decline in the agricultural sector. For 2024, we maintain our GDP forecast at 1.9%; as earlier demand shocks continue to wane (e.g., fiscal spending), we expect consumer spending to be supported by strong labor market dynamics and lower inflation. However, a high level of consumer debt will temper household spending in the upcoming year. On the investment side, prospects for lower interest rates and government spending programs looking to jumpstart manufacturing and public infrastructure will help investment grow 1.9% YOY. While external conditions will remain favorable in 2024, an expected slowdown amid Brazil’s important trade partners (China and the US) will limit the resilience of Brazil’s trade balance and growth dynamics. Finally, the latest results will likely not impact the pace of the central bank’s monetary easing, particularly because they portray a picture of consumer-led growth supported by fiscal stimulus while investment is declining. The end-of-year Selic is expected to reach 9.5% and remain above the neutral rate for the next 12 months.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.