However, “borrowing new to pay old” won’t resolve the root causes of China’s debt problem

Special refinancing bonds should give local governments issuing them some fiscal space to pay overdue bills to key suppliers. Multinationals waiting on money transfers from these local governments should consider gently pressing their contacts for payment.

Multinationals that rely on opportunities created by government expenditures should also benefit from the special refinancing bonds’ issuance. Given that these bonds carry lower interest rates and longer repayment cycles, they should allow officials more flexibility to pursue top policy priorities.

On a broader note, the issuance should also help stabilize consumption at the local level. Public sector employees, who are normally envied for their stable jobs and income but have recently faced salary cuts and concerns about their job security, are likely to regain some confidence and feel more comfortable spending again.

Overview

- Local authorities across China have—with Beijing’s blessing—begun to issue special refinancing bonds in recent months.

- Unlike other special bonds, special refinancing bonds have longer maturities and lower interest rates and are issued primarily to help fund the repayment of old debts, especially those carrying high interest rates.

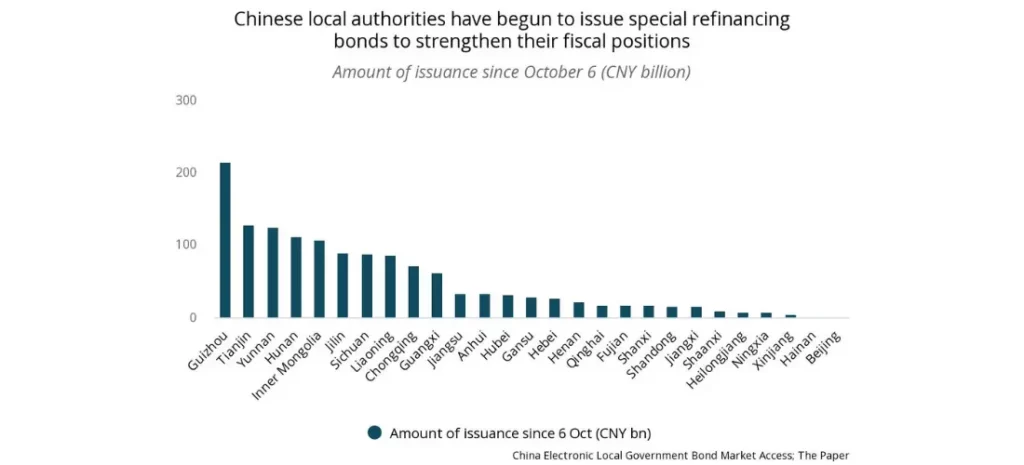

- Since the beginning of October, 28 regional authorities have disclosed relevant documents about their issuance of special refinancing bonds. Total proceeds have reached more than CNY 1.3 trillion.

- This trend is likely to continue, with an increasing number of provinces issuing additional such bonds to cover their debt repayments.

- While these special refinancing bonds alone will not be sufficient to address China’s debt issues (the IMF estimates that off-balance-sheet borrowing via LGFVs alone could be as high as CNY 60 trillion), the initiative is still encouraging, because it signals the central government’s willingness to intervene more actively than before on behalf of cash-strapped local governments.

Our View

The fact that local authorities have received approval from the central government to issue special refinancing bonds to repay old debts underscores the urgency of the debt problem, as this is a rarely seen occurrence. It implies that China’s local governments, collectively, are struggling to manage their finances. A few of them (notably Guizhou, one of China’s poorest provinces) have even publicly acknowledged their inability to repay their debts and have sought assistance from the central government. Their finances have been stretched so thin that they are struggling to pay suppliers on time and maintain a normal level of public services (e.g., keeping buses running).

Issuing special refinancing bonds is a relatively quick and easy way to address immediate problems. With lower interest rates and longer maturities, the bonds help alleviate the burden of repaying some imminent debts. The fact that 28 regional authorities have so far used this approach underlines just how widespread the debt repayment pressures are. With the proceeds from these bonds, local authorities should at least be able to repay some of the debts due imminently and remain afloat for now. Longer maturities also mean that local governments have bought more time to figure out how to tackle the debt issue in a fundamental way. This will help maintain confidence in and uphold the credibility of local governments. Unfortunately, the sheer scale of local governments’ debt loads is so huge that the amount issued so far won’t make a significant impact on total debt reduction. Thus, local governments will need to keep issuing more special refinancing bonds to buy more time for debt repayment, perhaps under better terms.

Ultimately, employing the strategy of “borrowing new to pay old” will not solve China’s debt issues. Essentially, it’s just kicking the can down the road, banking on the hope that a strong rebound in growth will generate sufficient revenues to cover debt repayments. Given the current dynamics of the Chinese economy, we do not believe the country will be able to grow out of its massive debt anytime soon. Special refinancing bonds are more likely to be salves than saviors for China’s local governments.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.