Milei’s recent announcement has helped dissipate dollarization fears; however, his proposed fiscal shock will likely face governability challenges

After the national holiday on Monday, the parallel foreign exchange (FX) markets experienced upward pressures due to uncertainties about the current administration’s FX policy leading up to December 10 and Milei’s anticipated approach to correcting the macroeconomic misalignments. Between November 17 and November 21, the MEP (for local bond transactions) and CCL (for overseas bond operations) rates increased by 15.7% and 7.1%, respectively. Similarly, the “dollar blue” depreciated 13.2%, standing at around 1,075 ARS:USD. Nevertheless, the Merval Index, measuring the performance of the most liquid Argentine stocks, soared by approximately 23%. Conversely, sovereign dollar bonds climbed around 1.9 cents, buoyed by Milei’s announcement that his government would meet all its commitments and respect private property. As inflation and FX pressures are expected to persist, clients should prepare for a challenging operational environment in the upcoming months. Multinationals should include the effects of the anticipated shock approach in their scenario-based planning, considering trigger points related to demand destruction and the risk of hyperinflation.

Overview

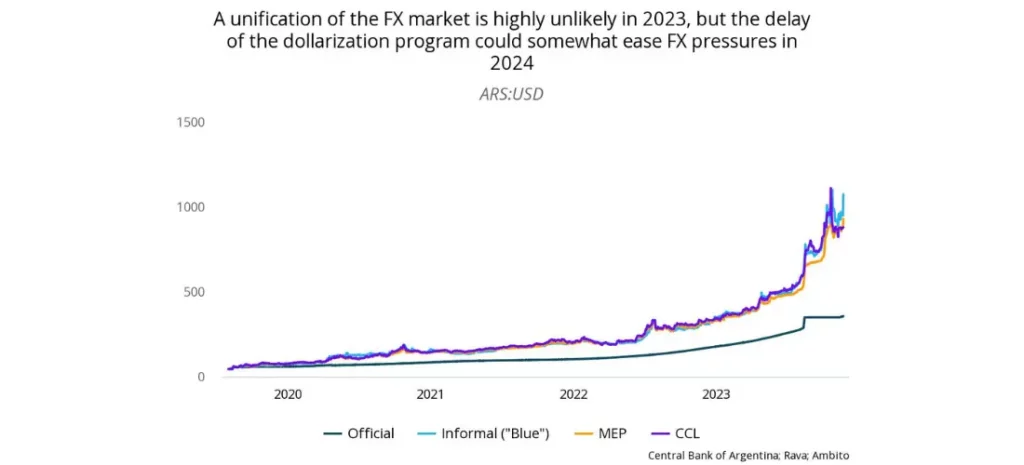

- Before the presidential election, the government resumed the gradual devaluation of the official exchange rate, allowing a monthly devaluation of approximately 3%. Additionally, the current administration updated the preferential exporter FX regime after the election. In this updated regime, 50% of the counterpart value of exported goods must be traded to the MULC market, while the remaining 50% is freely available. Given the current official (356 ARS:USD) and CCL (904 ARS:USD) rates, the updated regime implies an FX rate of around 630 ARS:USD.

- In recent announcements, Milei has declared his intention to maintain the current currency controls until the issue with Leliq, a financial instrument utilized by the central bank, is resolved. While the specifics have yet to be clarified, his statement has stabilized the demand for pesos and reduced the stock of Leliqs. The announcements have led the market to anticipate a delay in the dollarization program, suggesting it won’t be a short-term policy.

- Thus, Milei’s shock approach will primarily focus on the fiscal sector. The new president has mentioned a significant reduction in public investment (approximately 1.3% of GDP) and a rapid privatization of the state-owned airline, media outlets, and oil company.

Our View

While currency controls are expected to persist at least until Q1 2024, we do not anticipate that Milei’s administration will continue with the current system of gradual devaluation. Given the significant gap between the official and parallel rates, we foresee the implementation of a second devaluation after December 10. This is likely to result in an end-of-year official exchange rate ranging from 546 ARS:USD to 640 ARS:USD. In 2024, with the dollarization program framed as a second-generation reform, we project a year-end rate ranging between 944 ARS:USD and 1,193 ARS:USD. Moreover, we expect the current negative GDP trend to persist throughout 2024, marking a drop of 2.2% YOY in 2023 and a further 2.0% decrease in 2024. Finally, concerning the fiscal shock, the reduction of public investment can be implemented relatively quickly. However, the privatization program will likely face governability challenges, as the new government will encounter legislative gridlock and may also face significant backlash from unions.

Key actors within the Milei economic team:

- Finance minister: The two leading candidates are Federico Sturzenegger, president of the central bank between 2015 and 2018 and former congressman for the PRO party, and Guillermo Nielsen, president of the state-owned oil company YPF between 2019 and 2021 and former secretary of finance from 2002 to 2005.

- Central bank president: Milei has nominated Emilio Ocampo as the Central Bank of the Argentine Republic’s (BCRA’s) president. Emilio Ocampo is a professor of finance at the University of CEMA and a former investment banker.

- Economic advisors: The economic team comprises Carlos Rodriguez, former secretary of economic policy during Carlos Menem’s second term and director of the research center at the University of CEMA; Roque Fernández, who served as president of the central bank during the convertibility and as minister of economy during Carlos Menem’s second government; and Dario Epstein, president of the National Securities Commission (CNV) between 1992 and 1994.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.