Medium- and long-term fiscal stability could be at risk due to the government’s expansive spending agenda

Colombia faces a heightened risk to its financial stability stemming from the increasing likelihood of the government’s non-compliance with the fiscal rule. This risk is driven by the decline in tax collection following the nullification of several articles of the recent tax reform by the judicial branch, coupled with lower-than-expected extraordinary revenues. Additionally, there is a growing inclination from the government to increase public spending despite prevailing financial constraints.

The inability of Colombia’s government to comply with the existing fiscal rule could result in higher borrowing costs and inflationary pressures, thereby increasing operational costs for multinationals. Additionally, diminished market confidence may lead to financial instability and reduced consumer spending, impacting companies’ operating income. Over the long term, multinationals should engage in scenario planning to contend with a high probability of further tax increases to finance growing government deficits.

Overview

Colombia’s Fiscal Rule serves as a strategic tool for the national government’s financial planning, primarily aiming to set precise targets for fiscal balance relative to the level of public debt.

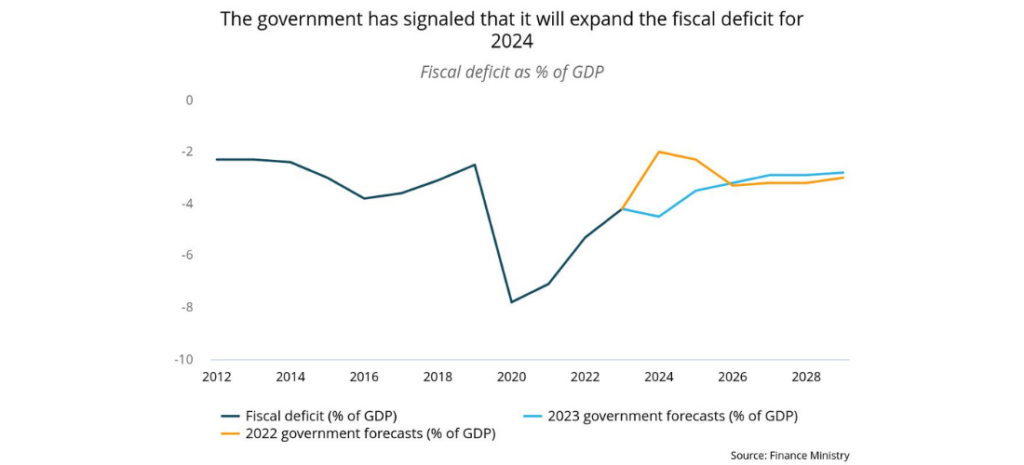

Looking ahead to the fiscal outlook for 2024, President Gustavo Petro’s administration plans to significantly raise public spending to COP 409 trillion (USD 104 billion), representing a 12.7% increase from 2023. Nevertheless, the government’s forecasted income for 2024 has been revised down 32% in its last financial plan, released in March. This revision suggests increasing reliance on debt to finance government spending expansion.

The revision of forecasted income for 2024 was prompted by the anticipated reduction in tax collection projected by the National Directorate of Taxes and Customs (DIAN), amounting to approximately COP 25.6 trillion (USD 6.6 billion). This anticipated decline can be attributed to several factors, including:

- A reduction of COP 6.3 trillion (USD 1.6 billion) due to a Constitutional Court ruling on the non-deductibility of royalties from oil, gas, and mining projects.

- A COP 3.0 trillion (USD 769 million) decrease because of a recent Council of State decision that impacted tax return review deadlines, which led to a surge in requests for credit balance refunds.

- A COP 4.0 trillion (USD 1 billion) drop from the hydrocarbon sector, mainly driven by the effects of a lower nominal exchange rate.

- A COP 7.3 trillion (USD 1.8 billion) decrease in non-oil revenue collection.

- A COP 5 trillion (USD 1.3 billion) decline in arbitration settlements related to litigation cases.

Our View

Despite these shortfalls, the government projects net tax collection for 2024 to reach COP 290.3 trillion (USD 74 billion), representing an increase of COP 27 trillion (USD 6.9 billion) compared to 2023. Notably, the government expects to raise up to COP 10 trillion (USD 2.5 billion) from litigation arbitrage, and approximately COP 13.5 trillion (USD 3.5 billion) from anti-evasion measures and enhanced efficiency endeavors. If these initiatives substantially miss the government’s forecasts, Colombia risks non-compliance with its fiscal rule. Additionally, Colombia’s Autonomous Fiscal Rule Committee (CARF) notes that additional tax collection from litigation arbitrage proceedings is being considered by the government as steady income when it should be deemed an extraordinary income.

To assess compliance with the fiscal rule, the CARF considers a metric known as the Net Primary Structural Balance (NPSB), which refers to the difference between total government revenues and expenditures, excluding debt interest payments and extraordinary incomes. Given the economic cycle, the CARF evaluates the government’s NSPB against a preset target aligned with medium- to long-term fiscal sustainability. Significant deviations signal potential risks to Colombia’s medium-term fiscal health, necessitating adjustments to spending or revenue.

If the additional forecasted tax collection from arbitrage proceedings is set to be considered an extraordinary income, the government’s NSPB will deviate 10.1% from the CARF’s target. In this case, to comply with the fiscal rule, the government will need to cut spending by COP 10 trillion (USD 2.5 billion) in 2024.

The government’s reluctance to curtail spending in 2024 could raise concerns about whether it will significantly increase the deficit to expand social transfers and public investment, and therefore miss its fiscal rule target. The government’s potential non-compliance with the fiscal rule could result in adverse outcomes such as higher borrowing costs, capital outflows, currency depreciation, and hindered economic growth. This situation would undermine investor confidence and restrict the government’s capacity to implement countercyclical policies in the long run.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.