The latest major policy rate hike highlights deepening inflation concerns and economic pressures

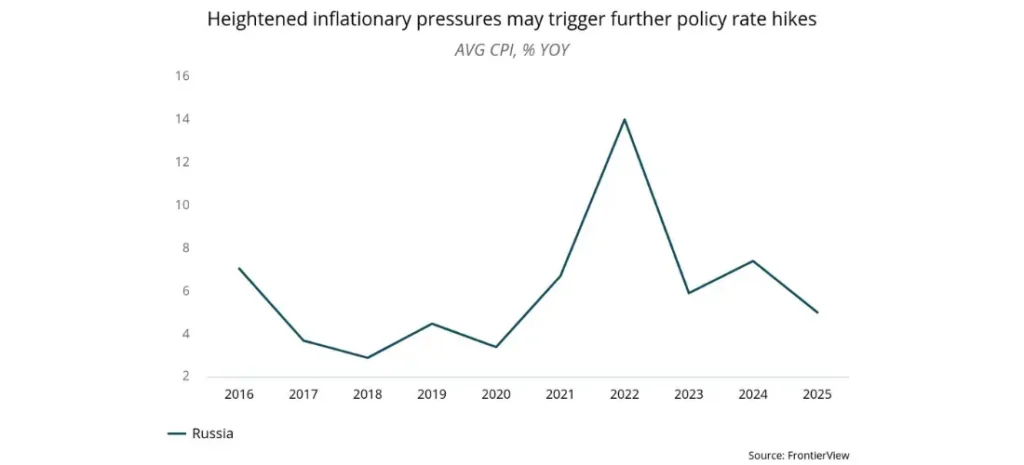

In response to persistent inflation, the Central Bank of Russia (CBR) has raised the policy rate by 200 basis points to 18%, the highest level since May 2022. Inflation remains a key concern, with the annual rate accelerating from 8.3% in May to 8.6% in June. While recent inflation has been partly driven by temporary factors, underlying inflation trends are also troubling, with seasonally adjusted core inflation rising sharply from 6.8% YOY in Q1 to 9.2% in Q2. Given these developments, the CBR has significantly revised its 2024 year-end inflation forecast upward to 6.5-7.0%, from a previous estimate of 4.3-4.8%, and expects the annual average inflation for the year to reach 7.8-8.0%, up from 6.2-6.4%. Projections for 2025 have similarly been adjusted, although the Bank still anticipates returning to its 4% inflation target by late 2025.

The CBR has also indicated that further policy rate hikes may be necessary, with rates expected to remain above 16% by year-end. The Bank has cautioned that the economy faces the risk of stagflation due to ongoing supply-side constraints, which could potentially lead to a deep recession. To counter these risks, the CBR will be maintaining a tight monetary policy for an extended period.

Business implications

Businesses should prepare for a prolonged period of elevated interest rates and high inflation, which will increase operational costs and tighten profit margins, particularly for local partners. For multinational corporations (MNCs), it is crucial to recognize the growing capacity constraints driven by labor and capital shortages. These challenges are exacerbated by factors such as mobilization, emigration, and the ongoing impact of international sanctions.

Given the current geopolitical landscape, it is unlikely that sanctions will be lifted in the near term. Although there may be minor relief as part of potential negotiation packages, significant changes are unlikely. Furthermore, MNCs should anticipate that the war will extend into 2025, with no major breakthroughs on the battlefield expected in 2024. Despite recent diplomatic rhetoric and increased efforts by non-aligned intermediaries, a decisive resolution that will bring resolution remains far away. In this environment, businesses should focus on adapting to prolonged instability by diversifying supply chains, strengthening local partnerships, and preparing for the ongoing economic and geopolitical volatility that is likely to continue shaping the market landscape.

Will the Central Bank be able to fight inflation?

Inflation Outlook: We maintain our view that inflation may gradually slow starting in Q3 2024, driven by the delayed effects of high policy rates and a high base year effect. We project annual inflation to average 7.4% in 2024 and 5% in 2025. However, the balance of risks remains tilted to the upside, particularly due to stronger-than-expected demand fueled by fiscal stimulus.

Overheating Economy: In Q1 2024, the economy recorded a robust 5.4% YOY growth, following a 3.6% YOY growth in 2023. The CBR raised its 2024 growth forecast to 3.5-4% from 2.5-3.5% and lowered its 2025 estimate to 0.5-1.5% from 1-2%. While growth should moderate in the following quarters, the economy continues to operate above its sustainable capacity, exacerbated by acute labor and capital shortages. Since the start of the war, at least 650,000 people, primarily young adults aged 20-40, have left Russia, further straining the labor market. Mobilization and an aging population have compounded these shortages. Additionally, payment issues are straining Russia’s trade relations with China, Turkey, the UAE, and other so called “friendly nations”. As of July 1, China has tightened export controls on certain industrial items, complicating supply chains and increasing costs for Russian importers.

Banking Sector: Despite high interest rates, robust lending has been a major driver of consumption growth. Both retail and corporate loans have maintained their growth trajectory, with consumer lending increasing by 9.7% since the start of the year, and corporate lending accelerating to 7.5%. This year, consumer loans have consistently sustained a growth rate slightly above 20% YOY, reflecting a robust demand for such loans. The termination of subsidized mortgages from July 1, which had been a significant market-distorting factor, alongside previously adopted macro-prudential regulations, is expected to moderate lending growth. However, demand is likely to remain elevated due to ongoing war-related payments.

Future Policy Rate Decisions: It appears increasingly likely that the Central Bank will raise interest rates again in the upcoming September meeting. Anticipation of further rate hikes may prompt consumers to accelerate borrowing, which could keep inflation elevated for longer than expected and necessitate additional rate increases. While the Central Bank seems less inclined to implement shock therapy with one-off substantial rate hikes, its appetite for larger hikes may grow if inflation persists at high levels.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.