Geopolitical shocks and policy shifts are reshaping the global economy faster than expected

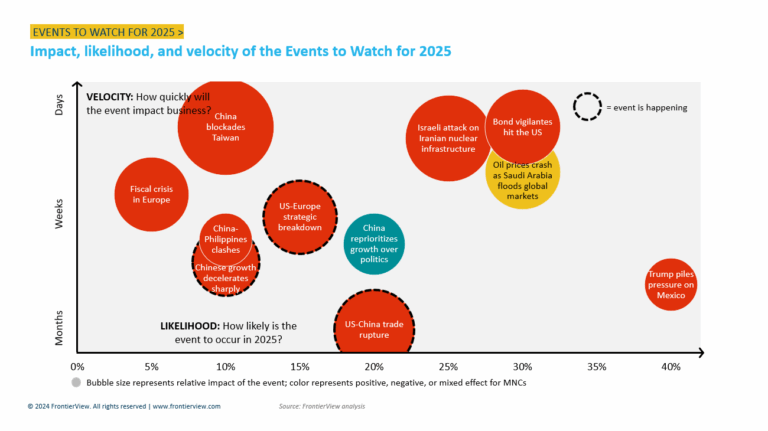

It has been almost six months since the release of our 2025 Events to Watch, our annual report that highlights events that sit outside of our base case but have the potential to be highly disruptive to the global outlook and to multinationals. As we approach the halfway mark of 2025, we take stock below of how these events have progressed, whether or not they have materialized, and how their probabilities have changed.

Donald Trump’s return to the White House has proven to be a global inflection point. Escalating US-China tensions and sweeping tariffs on both rivals and allies – such as Mexico, Canada, and the EU – have fundamentally altered global trade dynamics. Meanwhile, geopolitical flashpoints from Ukraine to the Middle East and Taiwan continue to represent a high-risk environment.

Multinationals are increasingly exposed: trade barriers are increasing costs and disrupting supply chains, while political pressure is mounting in key markets. With volatility rising, our mid-year update assesses how each event has evolved, what has materialized, and how companies should adjust their contingency strategies going forward.

US-China tensions lead to a trade rupture:

Probability: Event is happening.

Our View: The imposition of 145% tariffs on Chinese goods goes far beyond even our worst case scenario, and will lead to the virtual elimination of US-China bilateral trade. As envisaged in our Event to Watch, growth in both the US and China will see a sharp deceleration as a result.

A strategic breakdown in US-Europe relations:

Probability: Event is happening.

Our View: Several of the signpost for this event appear underway. From a trade standpoint, the situation remains very delicate – Trump has indeed applied high tariffs on European goods, but the EU has so far withheld on retaliation, in the hope of avoiding escalation. Geopolitically, however, the situation is clearer: US-EU relations are near an all-time low, notably following the high-profile spat between Trump and Zelensky, and JD Vance’s highly controversial Munich speech.

Chinese growth decelerates sharply:

Probability: Event is happening.

Our View: China’s growth is indeed going to see a higher-than-expected deceleration, although not on the scale envisaged in our Event to Watch (we expect 4.1% growth, above the 2.7% in the Event), nor for the reasons outlined (the Event highlights primarily domestic factors). China’s growth slowdown will instead come from abrupt fall in US-bound exports as a result of tariffs, and the ensuing drop in consumer and business confidence.

Saudi Arabia floods global oil markets:

Probability: Increased from 20% to 30%

Our View: Two of our signposts to monitor are materializing. First, oil prices have fallen to around USD $65/barrel (as a result of the tariff-related global slowdown). More importantly, there is increasing internal discord within OPEC+ – Saudi Arabia has sought to punish and pressure overproducers such as Kazakhstan and Iran by increasing its oil output more than expected. With few signs of this abating, there is an increasing likelihood that Saudi Arabia will increase output substantially.

China blockades Taiwan:

Probability: Unchanged (10%)

Our View: While military activity surrounding Taiwan has increased in recent months, we continue to assign a 10% likelihood of a Chinese blockade of Taiwan in 2025. For one, recent developments in China’s military, notably the removal of several high-ranking officials, suggest that the military would not be ready to execute a blockade of the island. Chinese leadership is also likely to hold off on any action regarding Taiwan until the outcome of its trade war with the US is clearer – we expect negotiations to last into H2 2025.

Europe faces a fiscal crisis:

Probability: Reduced from 10% to 5%.

Our View: The likeliest epicenter of this Event to Watch, France, has seen an improvement in both its political and economic situation, which has led us to reduce the likelihood of this event. The country managed to form a government and pass a budget, and its fiscal situation does not appear to be of immediate concern to financial markets. Still, the situation remains a precarious one.

The AfD enters government in Germany:

Probability: Reduced from 5% to 0%

Our View: The German federal election went according to our base case – the CDU came first, while mainstream opposition parties (notably the SPD) gained sufficient seats to form a coalition with the CDU, keeping the AfD out of government.

Attacks on Iranian nuclear infrastructure trigger an all-out war:

Probability: Unchanged (25%)

Our View: One of the key signposts for this Event to Watch is continued tit-for-tat attacks between Israel and Iran like the ones seen in 2024, which would escalate and lead to a strike on Iranian nuclear facilities involving US military intervention – direct confrontation between the two countries has in fact quietened down in 2025. Meanwhile, the Trump administration is looking to revive the Iran nuclear deal, and is therefore likely to withhold support for such strikes in the short-term. Still, tensions remain elevated, and a breakdown of US-Iran talks could trigger this event, particularly given Israeli insistence on such action in the short-term.

The Trump administration maximizes pressure on Mexico:

Probability: Increased from 15% to 40%.

Our View: The Trump administration has indeed applied high tariffs on Mexican goods, and engaged in harsh rhetoric on topics such as immigration and drugs. However, Mexico’s response so far has been conciliatory, and President Sheinbaum has opted against substantial retaliation, which has prevented an escalation and breakdown of relations.

Turbocharged US growth forces the Fed to pause its rate cuts:

Probability: Reduced from 30% to 0%.

Our View: The US’s growth outlook has deteriorated dramatically since January, following the announcement of a broad range of tariffs which will disrupt the US economy, and slow both consumer spending and investment. Having said that, we do expect the Federal Reserve to move forward with few cuts this year, as a result of tariff-related inflationary pressures.

Bond vigilantes hit the US:

Probability: Increased from 15% to 30%.

Our View: The Trump’s administration inconsistent and disruptive policymaking have damaged investor confidence and, in doing so, set the scene for a potential fiscal event – bond yields soared in the week following the Liberation Day tariff announcement. Our attention now turns to the budget process: should Congress attempt to pass a budget which pairs tax cuts with unclear revenue-raising measures, bond yields could once again see strong upward pressure.

China-Philippines clashes spiral out of control:

Probability: Unchanged (10%)

Our View: No major events have occurred that would make us either increase or decrease the probability of this event.

China reprioritizes growth over politics:

Probability: Unchanged (20%)

Our View: We are waiting to see the scale, but more importantly the composition, of Chinese stimulus to see whether this Event to Watch will materialize.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.