MNCs should plan for a wide range of oil price outcomes in 2025 and 2026

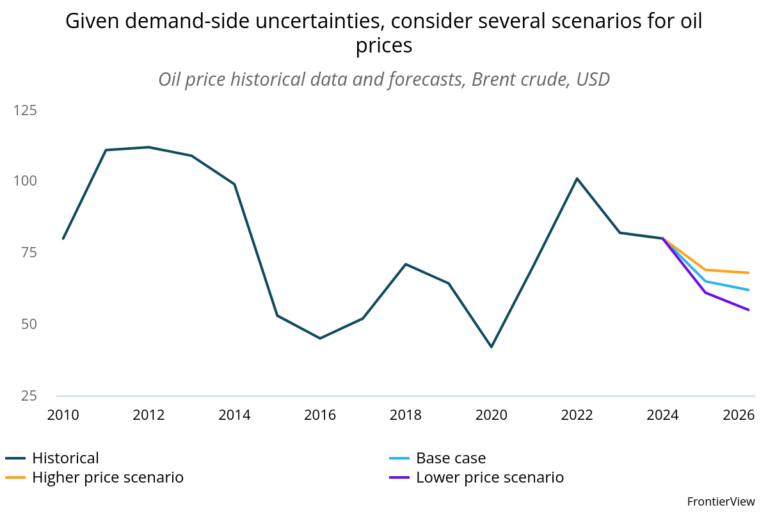

Global oil prices are entering a period of heightened volatility, as Trump’s tariffs redraw global trade and lead to a substantial slowdown in global growth, particularly in the US and China. This has led us to revise down our base case forecast to US$ 65 per barrel (Brent crude) in 2025, and US$ 62 in 2026. We explore in detail the driving factors behind this revision to our base case in our recent insight bite.

In this insight bite, we develop three different scenarios for oil prices in 2025 and 2026. These revolve around the main uncertainties plaguing the global economy and the oil price outlook, namely the path forward for US tariffs, the scale of the slowdown in US growth, the strength of fiscal stimulus in China, and internal cohesion within OPEC+. Depending on the outcome of these factors, oil prices could range between US$ 61 and US$ 69 in 2025, and between US$ 55 and US$ 68 in 2026 (more detail below).

Business implications:

Multinationals should prepare for a large range of possible oil prices, which will shape input costs, shipping rates, consumer prices, and energy sector performance. Firms in energy-intensive industries such as chemicals, manufacturing, and logistics should stress-test operations under all three scenarios below.

In oil-exporting markets, executives should be ready for downward revisions to economic growth and government spending targets, potentially weakening consumer demand and delaying public projects. Multinationals should proactively engage with customers and distributors in these markets to assess demand risks, adjust inventory or payment terms where needed, and get ahead of potential receivables issues.

In commodity-importing markets, lower oil prices may ease inflation and support faster monetary loosening, improving consumer purchasing power. However, the overall macroeconomic outlook will remain fragile.

Finally, given the current global economic environment, executives should expect volatility and large swings in oil spot prices – however, in order to avoid overreacting to short-term fluctuations, they should ensure their scenario plans include robust signpost monitoring frameworks that track broader oil market fundamentals, rather than short-term market volatility.

Oil price scenarios:

Base case (55% likelihood): Oil prices average US$ 65 in 2025 and US$ 62 in 2026 as global demand softens amid economic slowdowns in both the US and China. Trump’s broad tariffs weigh heavily on trade, manufacturing, and shipping volumes, while China’s stimulus efforts fall short of offsetting the hit to growth. OPEC+ continues to increase production modestly (+130k bpd), but internal tensions remain contained. The result is a subdued oil market shaped more by weakening demand than dramatic supply shifts.

Lower-price scenario (25% likelihood): Brent prices drop to US$ 61 in 2025, and decline further to US$ 55 in 2026. The US falls into a full-blown recession as tariffs bite deeply into investment, hiring, and consumer sentiment. Chinese stimulus remains limited, and global manufacturing continues to weaken amid trade tensions and a sharp slowdown in global demand. On the supply side, Saudi Arabia accelerates production hikes (multiple 400k bpd increases) amid growing frustration with quota non-compliance among fellow OPEC+ members. The oil market is oversupplied, and prices slide further.

Higher-price scenario (20% likelihood): Oil prices rise to US$ 69 in 2025 and US$ 68 in 2026 as global economic conditions improve. The US de-escalates key trade disputes, China delivers stronger-than-expected stimulus, and global sentiment rebounds. Demand for oil picks up across sectors, including manufacturing and travel. OPEC maintains its disciplined but modest production increases (+130k bpd), helping tighten the market just as demand recovers. This scenario lifts prices and rekindles pressure on energy-importing economies.

Signposts to monitor:

- US tariff policy: Major escalations or de-escalations would significantly alter demand forecasts and pricing pressure.

- OPEC+ strategy: Watch for breakdowns in cohesion, or pivots in production policy (especially if prices fall below $50/barrel).

- Chinese stimulus: The scale and effectiveness of stimulus measures will shape demand recovery and commodity market sentiment.

- Global demand indicators: Shipping volumes, manufacturing PMIs, and air travel data will provide early signals of demand resilience or weakness.

- MENA geopolitics: A regional escalation (e.g. direct Iran-Israel conflict) could lead to supply shocks and rapid price spikes.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.