Higher shipping costs and supply chain snarls threaten the disinflationary trajectory underway in the global economy

With shipping prices at nearly double their 2023 level, and delays to deliveries globally, the impact of tensions in the Red Sea are likely to be felt across the global economy. MNCs in sectors such as autos and consumer durables are most at risk, particularly in European markets. Should the disruptions be prolonged and input cost inflation increase substantially, businesses will face precarious pricing decisions given rising price sensitivity among a range of customers.

Overview

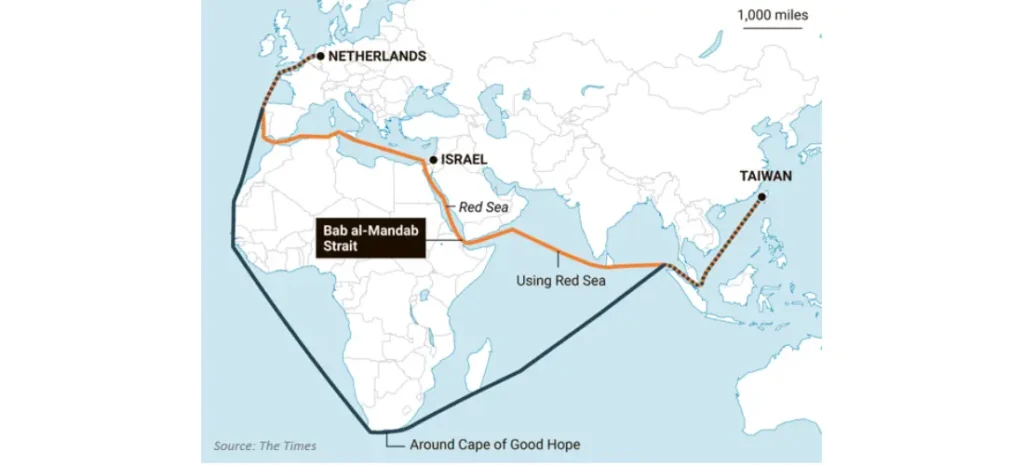

- Since December 2023, attacks from Houthi militias on Western container ships in the Red Sea have forced several major shipping companies to divert their vessels away from the route and sail around Africa instead, adding between 7 and 20 days to transit times.

- The Red Sea and the Suez Canal see 12% of global trade pass through them, accounting for around US$ 1 trillion of goods each year.

- The situation has led to a spike in global shipping rates, which are 77% above their 2023 level—this increases to 166% for the East Asia–Northern Europe route, a critical artery of global trade. This is in addition to the spike in insurance premiums.

- Major shipping companies, such as Maersk, Hapag-Lloyd, and MSC have all temporarily halted transit through the Red Sea. Meanwhile, several multinationals have already felt the impact of these disruptions: Tesla and Volvo have both had to halt production in European factories, while IKEA has warned consumers they could face delays and reduced availability.

- Oil prices have remained stable amid the tensions.

Our View

While the war in Gaza had until now been contained to the Middle East, the Red Sea shipping disruptions have now become the conduit through which it spills over into the global economy.

There are three pieces of good news: first is that, while shipping prices and supply chain disruptions are both increasing, this will come nowhere close to the scale of the shock of 2021–2022. Second, there is a notable amount of slack in global supply chains at the moment, in large part due to sluggish goods demand and manufacturing activity. This means supply chains will be able to absorb, to a certain extent, some of the current disruptions. Third, there is evidence that, since the pandemic, multinationals have started to carry more inventory in order to protect themselves from issues such as this one.

Still, executives should be acutely aware of the potential that this situation can have on the global economy. Further escalations in the Red Sea could force global trade to be diverted from the crucial route for several months, and potentially oil supply as well. In turn, this would force businesses to pass on (or absorb) higher costs, and lead to higher prices at the pump for consumers—in other words, higher inflation. Depending on its severity, this could derail the upcoming monetary easing cycle, with negative implications for global growth in 2024 and beyond. While we aren’t there just yet, the stakes are high.

We assess that Europe is most at risk, for two reasons: first, due to its proximity to the Suez Canal, it is more exposed to the shipping routes where prices have spiked. Second, Europe has become more reliant on Qatar’s LNG since Russia’s invasion of Ukraine: it accounts for around 13% of Western European gas consumption. Yet, Qatar has started to divert shipments away from the Red Sea, potentially placing pressures on hitherto elevated levels of gas storage.

Despite the tensions, oil prices have barely budged. This is thanks to the fact that, despite the rerouting of a handful of oil tankers, there have been no attacks on oil infrastructure. Oil markets are also enjoying significantly more balanced fundamentals, thanks to heightened US production and lower global demand. Still, any major escalation, say involving Iran, would likely lead to a spike in oil prices, both from reduced supplies and heightened risk premia, although we currently assign a low level of likelihood to this event.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.