Labor market resilience and housing inflation are slowing the path down to the Fed’s 2% inflation target

Multinationals should ensure they consider the possibility of fewer-than-expected rate cuts in the US in 2024. While it is all but guaranteed that the Fed is done hiking rates, the loosening cycle is likely to be slow and tentative, and subject to developments in inflation.

Multinationals both in the US and abroad should keep a close eye on US inflation data in the next few months. In the US, a later-than-expected start to cutting would delay expectations of a pickup in sectors sensitive to interest rates such as housing and autos, as well as for overall business investment. It would also place further strain on the commercial real estate sector, which is already showing signs of buckling. At the global level, higher US interest rates would keep pressure on currencies, and potentially force other central banks to delay their own cutting cycles, choking growth for longer than they would want.

Overview

- Following one of the most aggressive tightening cycles in history, the Federal Reserve is now done with hikes and looking ahead toward cuts. However, the US’s central bank faces both economic and political considerations.

- With the downward trajectory of inflation appearing to stall, and continued resilience in hiring activity, monetary loosening is close but not here just yet.

- The timing of rate cuts will need to be mindful of major political events in the run-up to the election.

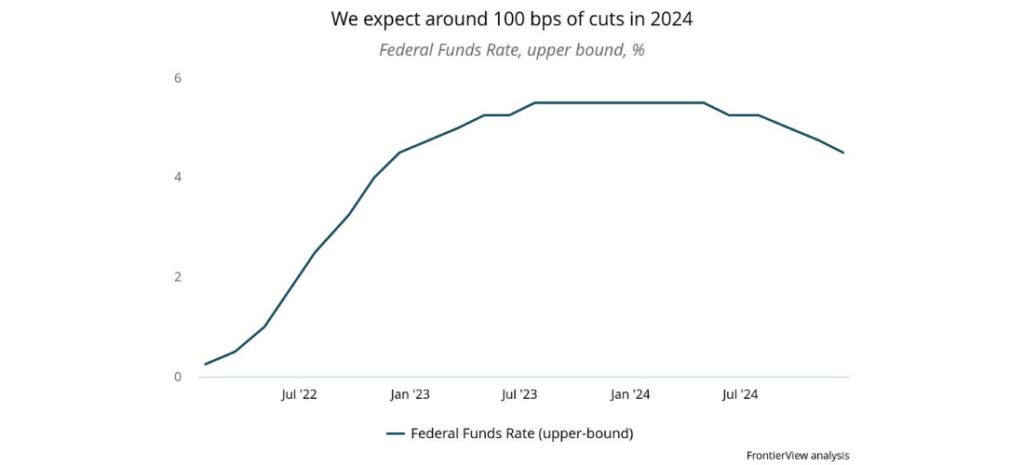

- We expect around 100 basis points of cuts from the Fed in 2024, starting from around June. However, an alternative scenario emerges, whereby the Fed is unable to cut until after the election in November.

Our View

Recent data in the US has highlighted the challenges of the “last mile” down to the Fed’s 2% inflation target: while the inflation rate initially fell rapidly from its June 2022 peak of 9.1% YOY, it has been stuck in the 3’s for the past nine months. Much of that has to do with stubborn housing inflation; the US’s limited housing stock is keeping both home and rent prices high. Meanwhile, price growth in the service sector also remains elevated, as businesses continue to pass on the costs of higher wages.

There are reasons for optimism: forward-looking indicators of rent prices indicate an easing in upward price pressures, which should slowly trickle through into official data in the coming months. Oil prices have remained relatively stable and are set to remain so for the remainder of 2024 thanks to more balanced global oil markets, and goods will continue to provide downward pressure to inflation. Overall, the economy appears to be cooling slightly, which will help loosen the labor market and reduce wage pressures for businesses.

We continue to believe that inflationary pressures, notably housing and services, will ease throughout the second quarter of the year such that the Fed will be able to reduce its benchmark interest rate by June. From then on, we expect to see around 100 basis points of cuts over the course of 2024, taking the Fed’s rate to 4.50% (upper bound) by the year’s end. Crucially, we do not expect the Fed to wait until inflation is back to exactly 2% before cutting. We also expect the Fed to hold firm against political pressure from both Republicans and Democrats in the run-up to the 2024 election.

Signposts to monitor:

- _CPI and PCE reports in Q2 and early Q3: I_n particular, keep an eye on month-on-month figures, and sub-indicators such as housing inflation and so-called “supercore” inflation, which excludes energy, food, and housing.

- Labor market data: Watch for any substantial upside surprises to payrolls, as well as wage growth.

- _Oil prices: A_ny substantial and sustained increase in oil prices, say from an escalation of geopolitical tensions in the Middle East, would increase the likelihood of the Fed keeping rates steady for longer than expected.

- Q1 GDP data: Q1 data will be released in time for the Fed’s meeting, which will allow for clues as to their assessment of growth and the restrictiveness of rates on the US economy.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.