Lower inflation and a robust labor market will keep the US economy in expansive territory

Overall, the US will continue to present significant growth opportunities compared with other major markets, notably in Europe. Firms in the B2B and B2C space, however, should draw up their 2024 plans for the US with heightened price sensitivity in mind and aim to decrease reliance on price increases for bottom-line growth. B2B firms should ensure they are capturing opportunities in value chains benefiting from IRA-related subsidies and incentives, such as clean energy, electric vehicles, and semiconductors, and steering clear of at-risk sectors such as commercial real estate. Multinationals should also ensure they begin to prepare for a potential Trump presidency, notably by assessing their exposure and sensitivity to tariffs, as well as their reliance on IRA-related incentives.

Overview

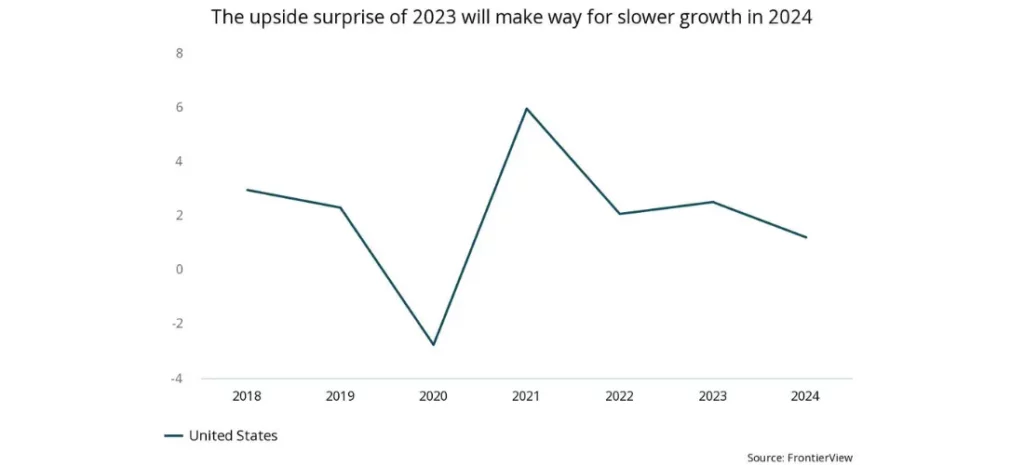

- The US economy has been the strongest-performing major Western economy in 2023, with growth accelerating throughout the year: Q3 GDP data showed the US economy grew at a rate of 4.9% (QOQ, annualized).

- However, we believe that growth is set to slow in 2024, down to 1.2% YOY from 2.5% YOY in 2023.

- Meanwhile, inflation has registered a sizable fall from its peak of 9.1% YOY in June 2022 to 3.2% YOY in October 2023, although it remains above the Federal Reserve’s target of 2%.

- The Fed has likely ended its monetary tightening cycle as it assesses the cumulative impact of past rate hikes. However, rates are unlikely to come down until at least Q2 2024, and cuts will happen slowly.

- 2024 will be an election year in the US: our base case assumes a very close contest between Donald Trump and Joe Biden, which we expect Trump to narrowly win.

Our View

Globally, 2023 has been a story of resilience, and no market exemplifies this better than the US. American consumers have remained free-spending in the face of elevated inflation, buoyed by the excess savings from pandemic-era stimulus programs and a historically strong labor market. Elsewhere, falls in business investment and housing activity have been partially offset by strong growth in industries such as clean energy, electric vehicles, and semiconductors, in part thanks to industrial policy measures passed by the current administration.

However, there is reason to believe that the pace of growth is likely to slow. While Americans continue to spend, credit card data shows that this is increasingly being fueled by borrowing, posing questions as to the sustainability of the current trajectory, especially in an environment of elevated borrowing costs. Savings are also being depleted, reducing the buffer that Americans have against the higher cost of living. However, a return to positive real wage growth and only limited deteriorations in the labor market will help to sustain some spending growth, which we expect to remain tilted toward services.

The trajectory of inflation has been overwhelmingly positive in recent months: both headline and core inflation have fallen substantially, without the deterioration in demand and labor market conditions that many thought would be necessary for lower price growth. Looking ahead, we expect further moderation in inflationary pressures thanks to falls in housing inflation, as well as a rebalancing of labor market conditions that will return nominal wage growth to less inflationary levels.

Nevertheless, there is still a long way to go to return to the Federal Reserve’s target of 2% inflation. As a result, the Fed is likely to keep its benchmark interest rate at 5.50% until at least May 2024; its loosening campaign thereafter will be slow and conservative, and rates will remain in the 4–5% range well into 2025. In turn, this will keep the dollar strong, weighing to a certain extent on exports and providing modest inflationary pressures abroad. High rates will also limit growth in business investment, as well as in rate-sensitive sectors such as real estate, autos, and big-ticket durable goods. More positively, much of mortgage and corporate debt in the US is fixed and at a low rate, thanks to pandemic-era refinancing; this should limit, to a degree, the pressure of high interest rates on the US economy.

The state of the economy will be of particular importance in 2024, given the presidential election in November: we expect the contest to be a repeat of 2020, although we believe Trump will return to the White House in 2024 despite the legal troubles currently befalling him. Joe Biden’s popularity has been dwindling in recent months amid worries that his advanced age could impede his ability to govern effectively. While policy details remain sparse, a second Trump presidency would likely ramp up protectionist trade policy (including a blanket 10% tariff), focus on tax cuts, and seek to undo most of the policies in Biden’s Inflation Reduction Act.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.