The yen is likely to remain under pressure through Q3 2024, with a protracted rebound from Q4

Firms should prepare for sustained pressure on the yen through Q3 2024, with the potential for spells of short-term volatility like we saw last week.

The yen’s prolonged weakness will have a variety of implications for the Japanese economy:

- Import costs: Import costs will remain elevated and undermine profits of firms that bring products into Japan for the domestic market. These firms’ ability to pass on price increases to end-customers has also weakened, as price sensitivity has grown in the market. Moreover, local distributors will continue to face huge FX risks, which could disrupt their day-to-day operations (a challenge that will be made more acute by higher domestic interest rates).

- Export costs: Japanese exports will remain highly competitive, as they become relatively cheaper for international customers. Those exporters that rely heavily on domestic inputs in their production processes will have greater ability to compete on price than those that rely on imported inputs.

- Tourism: The tourism sector will continue to flourish in the coming quarters as international travelers flow in, attracted by the weak yen. In March 2024, monthly tourist arrivals hit their highest level in history at 3.1 million visitors. Not only are more people visiting Japan, but they’re also spending more due to their increased purchasing power. Per capita spending among tourists has risen by 50% compared to 2019 levels. The tourism sector will see a further boost from heightened domestic tourism, as many Japanese residents choose less expensive domestic destinations over more expensive international destinations.

- Sentiment: Confidence, among both businesses and consumers, will take a hit due to the yen’s recent fall. In fact, even Japanese exporters that traditionally benefit from a weak currency are concerned that the yen has fallen too far. As confidence in the domestic market erodes, more Japanese firms are investing their foreign earnings abroad rather than repatriating their profits or investing in the domestic market. Moreover, wage growth momentum in the market will likely suffer, as domestically oriented SMEs question their ability to manage the dual pressures of rising labor costs and rising import bills.

Overview

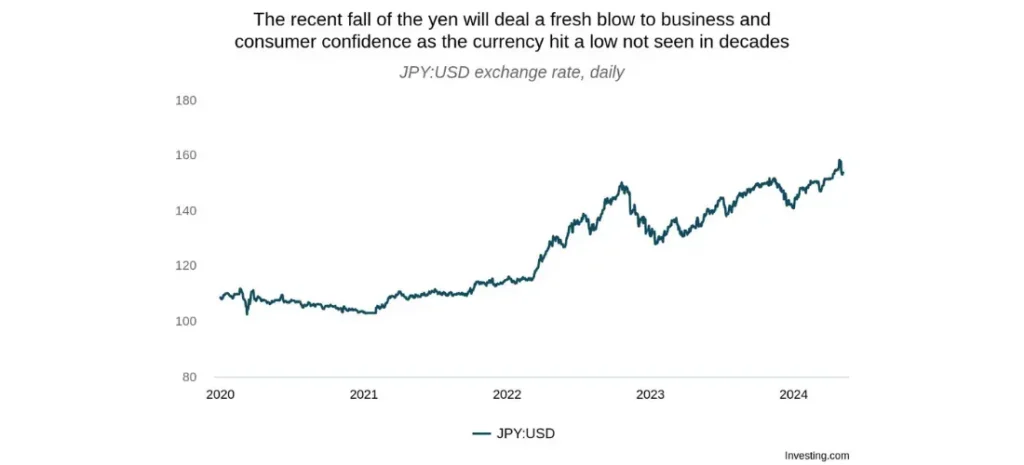

The Japanese yen has had a rollercoaster ride over the past two weeks. Market expectations shifted dramatically as the Bank of Japan (BOJ) and the US Federal Reserve delivered policy statements that resulted in a flurry of trading between April 26 and May 2. The yen briefly even fell to 160 against the USD (for the first time since 1990) before stabilizing near the 154 mark.

Our View

The events of the past two weeks suggest that the JPY will continue to face depreciation risk over the coming months. The yen will trade lower than previously expected, and its rebound will also be delayed into Q4 2024 and 2025.

The main driver of this outlook is a change in market expectations around US monetary policy. Inflation data in the US consistently came in above expectation through Q1, showing that progress against inflation is stalling. As a result, market rate cut expectations for the Fed have been pushed further into 2024, and in some cases to 2025. FrontierView’s own forecasts for the Fed also predict fewer rate cuts (of 75 bps) in 2024, which will only begin late in Q3. This was revised from a 100-bps rate cut forecast where rate cuts would begin in June 2024.

These shifting market expectations have had a negative impact on the yen and will continue to do so until clear timelines and expectations are established for US rate cuts. Japan’s own policy decisions will be less meaningful in determining the strength of its currency. The BOJ has repeatedly stated that further interest rate increases will only come on the back of strong inflation and wage growth data. Moreover, its rate hikes will be slow and measured to limit disruptions to the Japanese economy. Therefore, markets do not expect meaningful interest rate changes to come from Japan. The Japanese government may decide to directly intervene in currency markets to prop up the yen, but with the weight of the markets against it, these moves will only lead to short-term reprieves rather than sustainable appreciation.

Thus, firms should prepare for continued volatility in JPY:USD exchange rates over the coming months, with the risks tilted against the JPY. Only when interest rates begin coming down in the US do we expect to see a protracted recovery of the yen, likely over the course of Q4 2024 and 2025.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.