Benchmark interest rate hike to 14.75% likely marks peak

Monetary Policy Update:

On May 7, Brazil’s Central Bank (BCB) unanimously raised the benchmark interest rate (Selic) by 50 basis points to 14.75%—the sixth consecutive increase, pushing rates to their highest level since 2006. While the decision reflects ongoing concerns about persistent inflationary pressures, we believe this marks the end of the tightening cycle.

Main Drivers:

External factors:

- Though less exposed than some trade-dependent economies, Brazil faces indirect consequences from tighter financial conditions and slowing external demand. The BCB noted an expected slowdown in US growth due to tariffs and ongoing uncertainty around global demand, supply chains, and consumer behavior.

Domestic factors:

- Inflation expectations remain de-anchored, with short-term pressures acute in services, industrial goods, and food. The headline rate has consistently exceeded the 3% target (and 4.5% upper bound), signaling persistent demand-side pressures.

- The economy continues to operate above potential.

- Expansionary fiscal policy remains a key stimulus, with the BCB explicitly calling for decreased government spending and better monetary-fiscal coordination.

Business Implications:

- Tighter credit conditions: Elevated interest rates and high bank lending costs will continue to constrain consumer and business credit, especially in interest-sensitive sectors like retail, autos, and housing.

- Weaker consumer demand: Rising debt burdens and a cooling labor market are slowing household spending. Companies in consumer-facing sectors may see reduced revenue growth or trading down effects in H2 2025.

- Higher cost of capital: Financing costs for local operations and investments have surged. Multinationals should reassess capital allocation strategies and consider hedging interest rate and FX exposure.

- Investment reallocation: High real rates are attracting capital to fixed income, potentially reducing equity market liquidity. Firms with financial arms may need to adjust portfolio strategies accordingly.

The Turning Point: A Pause Ahead?

For the first time since the tightening cycle began in September 2024, the BCB presented a more balanced view of inflation risks, moving away from an exclusively hawkish stance. It outlined three key upside risks: persistent de-anchoring of inflation expectations, resilient service inflation tied to a stronger-than-expected output gap, and potential domestic or external shocks (ex., currency depreciation), alongside three downside risks: a sharper domestic slowdown, a deeper global downturn, and falling commodity prices that could ease inflation.

Against this backdrop, we believe the May hike likely marks the end of the tightening cycle. The BCB acknowledged the growing impact of high interest rates on corporate balance sheets, credit availability, and the labor market. Meeting minutes highlighted early signs of a credit contraction, especially in consumer finance where rising debt burdens are dampening household borrowing. With unemployment rising to 7% in Q1 2025 and financial conditions tightening meaningfully, the central bank appears increasingly confident that policy is now sufficiently restrictive. Barring a renewed inflationary shock, we expect the Selic rate to remain at 14.75% in June.

Fiscal Policy Update:

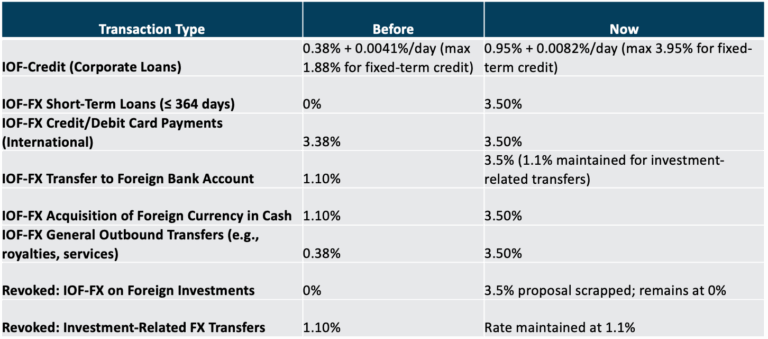

On May 22, Brazil’s Finance Minister Fernando Haddad announced significant increases to the Tax on Financial Operations (IOF) applicable to both credit transactions (IOF-Credit) and various foreign exchange transactions (IOF-FX). Shortly after the announcement, the government partially reversed course, revoking the increase related to the use of investment funds abroad and maintaining the previous rate for companies transferring funds overseas for investment purposes.

These tax changes were introduced as part of a broader fiscal package that includes a BRL 31.3 billion budget freeze. The measures aim to rein in public spending, reduce the fiscal deficit, and support the government’s fiscal targets.

Most changes took immediate effect, except for new supplier financing rules, which will be implemented from June 1.

Business Implications:

- Higher borrowing costs for both businesses and consumers.

- Increased costs for cross-border payments and international operations.

- Need for compliance reviews in credit and supply chain finance strategies.

- Policy uncertainty remains regarding the long-term direction of Brazil’s FX regime.

While not all cross-border transactions are affected, the overall rate structure for outbound FX transactions has shifted sharply upward, increasing the tax burden across a range of financial activities.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.