Capex opportunities remain concentrated in the public housing, mining, and security sectors

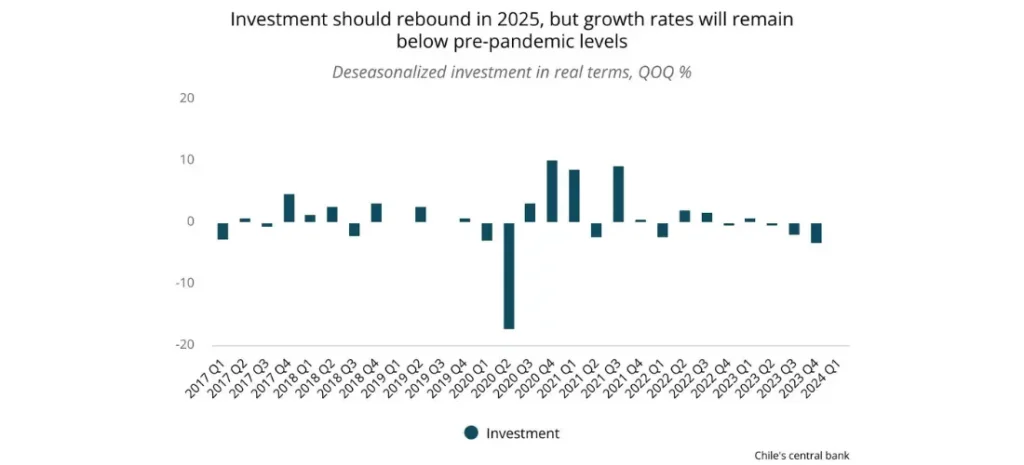

Although consumer spending and exports have strongly recovered, investment in Chile continues to register a notably weak performance. In 2024, investment in real terms is expected to decline by 1.0% YOY, accumulating two consecutive years of negative growth rate. Low levels of private investment mainly drive this result, while public investment has somewhat offset the negative outlook of the private sector. Our 2025 forecasts anticipate a muted recovery (1.7% YOY) as business confidence remains low.

Business Implications:

Multinationals should develop flexible CAPEX plans that are adaptable to changing market conditions, allowing companies to scale their investments up or down as needed. Additionally, firms should consider partnerships or joint ventures that can help share the financial burden of CAPEX projects. Given ongoing regulatory uncertainty, regular engagement with policymakers is advised to understand government priorities for future investments, particularly in construction. Furthermore, as sectors like security, housing, and energy continue to be government priorities, multinationals are encouraged to diversify their product and service offerings to cater to these growing sectors.

What are the economic and political indicators signaling?

- Business confidence: Businesses operating in key sectors remain clearly pessimistic. In July, the construction confidence index was 28.4 points, significantly below the optimistic threshold of 50 points. Similarly, confidence in the manufacturing sector remains within the pessimistic range at 42.1 points. However, it appears that the worst has passed, as confidence levels are slightly above 2023 levels, and companies in both sectors expect higher production and activity levels by year-end.

- Imports of capital goods: In the first seven months of 2024, imports of capital goods dropped by 10.4% YOY, marking 22 consecutive months of decline. This result is mainly driven by lower imports of motors, generators, and machinery for the construction sector. However, electric devices (31.6% YOY in July) and trucks and cargo vehicles (37.2% YOY) have started to recover, which should indicate a further reversal of the downward trend in 2025.

- Financial costs: In July, Chile’s central bank decided to maintain its policy rate at 5.75%, implying a real interest rate of around 2.15%. The institution stated that the majority of the planned rate cuts for 2024 were implemented in H1 2024. Given higher inflationary pressures, we maintain our view of a pause in the monetary easing cycle until Q4 2024.

- Public investment: In H1 2024, public investment rose by 26% YOY driven by higher execution in public housing, roads, and water and sanitation projects. This positive trend is expected to remain resilient in H2 2024 and 2025, with higher budget allocations for programs such as Mejoramiento Barrios and prison construction.

- 2025 presidential election polls: While the presidential election will lead to high levels of uncertainty, a market-friendly candidate is expected to win in the second round. President Gabriel Boric’s low approval rating (31% of respondents) makes a leftist candidate seem highly unlikely. Similarly, polls show that a far-right candidate like José Antonio Kast would likely lose against more moderate candidates like Evelyn Matthei or Michelle Bachelet. Low levels of political risk will bode well for private investment in the medium term.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.