A substantial portion of China’s output is likely to find its way to global markets

Multinational manufacturers in China should build flexibility into their production plans and revenue forecasts this year so they can pivot to account for changing market conditions. At the same time, they should proactively communicate what they are seeing to headquarters. This year, what happens in China is unlikely to stay in China, so corporate needs to be prepared for potential disruptions in the global marketplace.

B2B companies in most industries should prepare for local Chinese competitors to continue reducing prices this year and brace for aggressive negotiations. In some cases, firms should be prepared to accept reduced profits in 2024. Firms should also be aware that these challenging price and profit conditions may extend beyond this year and, depending on the specific sector, may prompt some re-evaluation of corporate strategies at the board level concerning production chain restructuring.

Firms that are looking to expand their presence in China should take advantage of the current soft labor market to fill job vacancies if they need to recruit. They may also want to allocate additional resources to their government public relations and intelligence gathering initiatives in China. More so now than in years past, multinationals must closely monitor the development of industrial policies and regulations, continually evaluating their impact on their business operations on the ground. They should also engage headquarters to understand how corporate is thinking about potential trade tensions between China and other key markets.

Overview

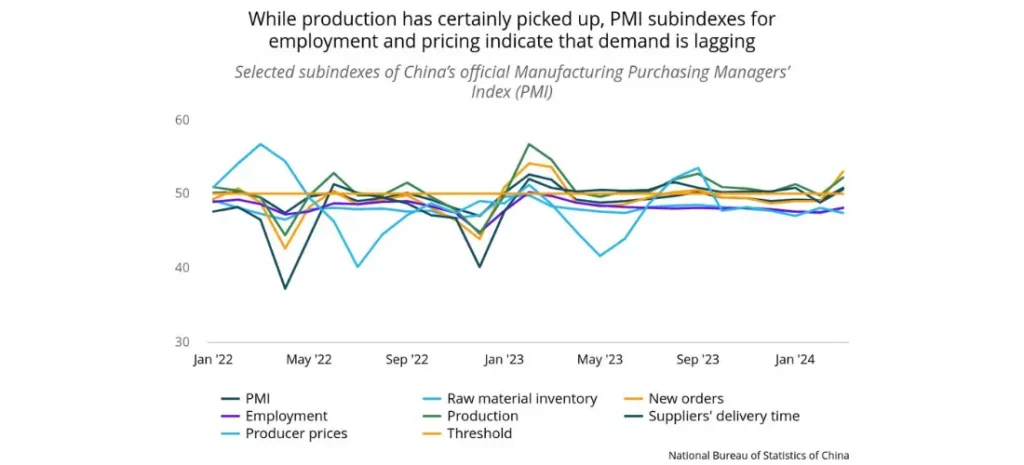

- China’s Purchasing Managers’ Index (PMI)—the official measurement of the country’s manufacturing activity from China’s National Bureau of Statistics (NBS), primarily reflecting the performance of state-owned enterprises (SOEs)—hit 50.8 in March, the first expansion in six months’ time.

- Among the subindexes, production and new orders showcased outstanding performance, soaring to 52.2 and 53.0, respectively, from the previous month’s 49.8 and 49.0, respectively.

- Conversely, the subindexes for raw materials and employment remained in contractionary territory, both registering 48.1 for March.

- The subindex for producer prices, which measures executives’ outlook for their products’ prices, fell from 48.1 in February to 47.4 in March.

- Another PMI index, which is compiled by Caixin and primarily focuses on small and medium-sized enterprises, likewise reported ongoing expansion in manufacturing activities. The index registered at 51.1 in March, marking an increase from 50.9 in February, and maintaining growth for five consecutive months.

- However, mirroring the pattern observed in the numbers from NBS, the Caixin PMI’s employment subindex also remained in contraction in March.

Our View

China’s rapidly improving PMI figures align with our prior prediction that, in contrast to last year, manufacturing growth will outpace consumption growth this year. This prediction is especially relevant now, as senior leaders clearly expressed their intention to prioritize industrial development and production at the recent “Two Sessions,” China’s annual legislative meeting.

The remarkably positive readings in subindexes such as production and new orders indicate that China’s industrial production has been performing robustly since the Lunar New Year holidays, likely exceeding expectations and signaling an overall robust and positive recovery within the manufacturing sector of the economy.

However, the persistently lagging subindex for employment suggests that the labor market in the manufacturing sector remains weak. In fact, employment readings have been in contraction for nearly a year now, indicating a clear hesitance among producers to fill vacant positions. This trend is also supported by the PMI subindex for producer prices, which has been consistently in contraction since the end of last year, signifying that executives are pessimistic about the potential pricing of their products. The profitability of manufacturers will therefore remain under pressure, necessitating active cost management.

In summary, China’s industrial production is poised to continue accelerating through at least the first half of this year. However, domestic demand will likely lag behind, in part because of the bleak outlook for employment. Consequently, China will have to export a significant proportion of its industrial output, resulting in an elevated risk of trade frictions with other countries worldwide.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.