An increasingly expansive fiscal policy, coupled with diminishing tax collection, has reduced government treasury levels to historical minimums

On June 6, the Colombian government announced partial and temporary restrictions on the transfer of budget allocations. The government will require so-called Certificates of Budgetary Availability, which confirm the availability of funds to cover planned expenses. Allocations without this certification cannot be transferred until tax collection conditions improve.

Although the government anticipates improved tax collection in H2 2024, overall tax collection has only increased by 5% YTD, while government operating expenses and investment have risen by 22%. Recent estimates from Banco de Bogotá suggest that to comply with the national fiscal rule—a legal constraint that prevents public debt from surpassing 55% of GDP—the government will need to cut US$ 12 billion.

Business Implications

Multinationals operating in Colombia should prepare for a slight depreciation of the COP due to the country’s precarious fiscal situation. They should include currency hedging clauses in their contracts agreed in international currency and prepare for a future tax reform in 2025.

B2G companies should brace for the cessation of projects, especially those contracted with local governments that depend on central government transfers. Nevertheless, we expect most spending cuts will be focused on reducing operating expenses rather than investment.

What’s behind the fall in tax revenue and how will it impact the market?

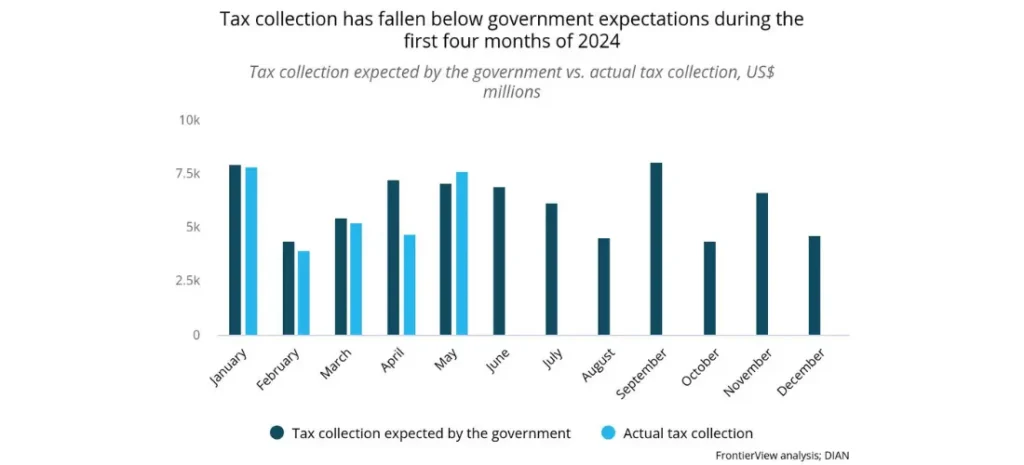

Following congressional approval of the 2024 General Budget, the government was expecting total tax revenue to be close to US$ 90 billion, with an allowance for spending up to US$ 127 billion. However, given the current growth rates, it is projected that annual tax revenue will only reach US$ 73 billion, a 19% shortfall from the expected figures.

Subdued growth has also contributed to lower-than-expected tax collection, as evidenced by the meager 0.9% YOY growth for Q1 2024, a figure below the government’s estimated average of 1.5% YOY growth, translating into an additional gap of US$ 4.6 billion in tax collection. According to Banco de Bogotá’s estimations, Colombia’s general budget for 2024 faces a financing shortfall of US$ 7.5 billion.

This shortfall is already impacting the National Treasury, which typically averages deposits of US$ 5.6 billion in the central bank at this point in the fiscal year. However, by April 2024, the deposits had fallen to below US$ 1.8 billion.

To comply with Colombia’s fiscal rule threshold, an additional reduction of US $7 billion in overall spending will likely be announced in this year’s Medium-Term Fiscal Framework, slated for publication in mid-June.

For the moment, the government has ordered all its ministries to cut 5.6% of its operating expenses. Finance Minister Ricardo Bonilla has stated that the purpose of these extended cuts its to save up to US$ 5 billion.

Considering that the investment budget stands at US$ 25 billion and 49.8% has already been committed, there remains US$ 12.6 billion yet to be allocated. If the strategy to meet the Fiscal Rule involves cutting investment spending, no further spending should occur in this category for the rest of the year, a scenario that seems unlikely and highlights the government’s need to start cutting its operational expenses.

The freeze on transfers declared by the Ministry of Finance has the potential to curb operating expenses and public investments, given that 59% of current budget allocations lack a Certificate of Budgetary Availability. However, there are doubts about whether the government possesses the political will to limit its own spending policy.

The ongoing fiscal situation may embolden the government to request that Congress extend this year’s debt threshold under the fiscal rule, arguing that without approval, the executive will be forced to declare an economic emergency.

Although the measure is likely to be deemed unconstitutional by the Constitutional Court, the indication of an increasing reliance on debt to finance the state’s operations could negatively affect the value of COP-traded assets in the bond markets.

Markets are already factoring a risk premium into Colombia’s sovereign debt securities. Although the country maintains a BB+ credit rating, since late May, Colombia’s credit default swaps have been trading at a higher premium than the average for BB- markets, signaling a potential credit downgrade in the coming months.

Failure to adjust spending in the Medium-Term Fiscal Framework could precipitate a credit downgrade, as agencies might view the lack of fiscal prudence as a sign of deteriorating financial health. This would likely increase borrowing costs due to a higher risk premium on government securities. Additionally, a lack of confidence in fiscal management could lead to depreciation of the COP.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.