Boycott waves are spreading across MENA, with the war in Gaza stretching into its third month; FrontierView sees more intense and longer-lasting impacts from boycotts compared to previous Israeli wars on Gaza

Despite a successful temporary ceasefire—which was extended twice—the war on Gaza has resumed, risking a return of heightened humanitarian casualties in Gaza, continued military and illegal-settler attacks on Palestinians in the West Bank and elevated regional security risks. Many multinationals have already experienced some supply chain disruptions, and consumer goods companies are facing volatile consumer behavior. Some Western brands have also seen significant backlash from consumers and local businesses in the form of boycotts. Consumer sector firms will see their operating environment impacted well into H1 2024, and below are key assumptions to take as they plan for the next few months.

The need to pause or reduce marketing and events will likely continue into Q1 2024: Over the past two months, multinationals have been proactive in canceling or postponing events and marketing campaigns in the MENA region due to the sensitivity of the humanitarian catastrophe in Gaza. Without a permanent ceasefire or solution in Gaza, multinationals will remain at risk of boycotts and adverse consumer reactions if they resume marketing or campaigning in an insensitive manner. FrontierView expects the base-case timeline to last into late February at least.

The continued boycotting of some multinationals products will lead to consumers adopting local alternatives: Lebanon, Egypt, Syria, Jordan, Kuwait, Qatar, and Iraq have seen the sharpest rate of boycotting activity against well-established brands (franchise or otherwise) in the wake of the war on Gaza. Some consumer beauty, F&B, and other FMCG categories have seen as much as a double-digit decline in their sales across various geographies. Fast-food chains in Egypt, Kuwait, Qatar, and Lebanon have seen a drop in demand and are undertaking promotional and discounting campaigns to incentivize consumers. Some businesses in Jordan are substituting beverages for domestic alternatives to safeguard their customer foot traffic. A continuation of this highly sensitive period will give consumers time and incentives to try new brands and local alternatives. Some of this shift in preferences could remain beyond the war in Gaza as consumers get acquainted with new products that they may enjoy and result in a structural shift in behavior.

The severity of boycotting is likely to remain relatively weaker in the UAE, Saudi Arabia, and Morocco: The large and diverse expat population in the UAE, communication of the role of franchises in Saudi Arabia, and the far proximity of Morocco render a more moderate adoption of boycotting; nonetheless, targeting activity against the likes of Carrefour saw foot traffic into the supermarket chain drop. FrontierView expects that if Israeli aggression in Gaza intensifies, the level of boycotting—especially in Saudi Arabia and Morocco—would increase. Multinationals are advised to maintain mitigation plans, as the risk of boycotting extends into 2024.

Consumer exhaustion and a return to boycotted brands is likely to be delayed compared to previous episodes: Though there are no qualified metrics defining how long boycotts last, a number of factors are influential in its length. Some of these include severity of the cause (the level of Israeli military aggression/death toll), social media reach, state-level opposition and policies, consumer purchasing powers, and ease of substitution. Compared to previous Israeli wars on Gaza, the severity of this event is far greater—nearly 15,500 Palestinians are dead, among them nearly 9,000 children. The widespread social media information campaigns have also amplified the reach despite the Israeli internet ban on Gaza. Therefore, FrontierView expects the impact of boycotts to last well into Q1 2024 at a minimum, with a longer-lasting effect than previous Israeli wars.

The risk of boycotts trickling through to other sectors remains: While most boycotting activity has been largely contained to the consumer space, multinationals must monitor the risks for their business carefully regardless of their sector. So far, government-level sanctions or boycotts and embargoes have not been announced, and FrontierView expects the likelihood of implementing legal and formal measures for tenders and public projects to remain low. However, this does not mean individual perceptions and de facto decision making will not be influenced by current political and humanitarian tendencies. For example, some industry associations in Jordan have begun to evaluate reducing purchases from brands perceived to either have a presence in illegal settlements or are investing in such regions, or that are vocally supportive of Israeli military actions against Palestinians in the West Bank or Gaza. Similar approaches could be taken by some private sector business customers.

Implications:

- Expect to see weaker recovery in consumer sentiments for Western brands in markets closest to Palestine or where state-level opposition to the Israeli war on Gaza is vocal.

- Competition from domestic brands will likely rise in 2024 accompanied by competitive marketing campaigns, risking loss of market share. A prolonged war in Gaza along with strong competition from domestic brands could make the loss in market share permanent (into the medium term), as brand loyalty in some MENA markets continues to erode.

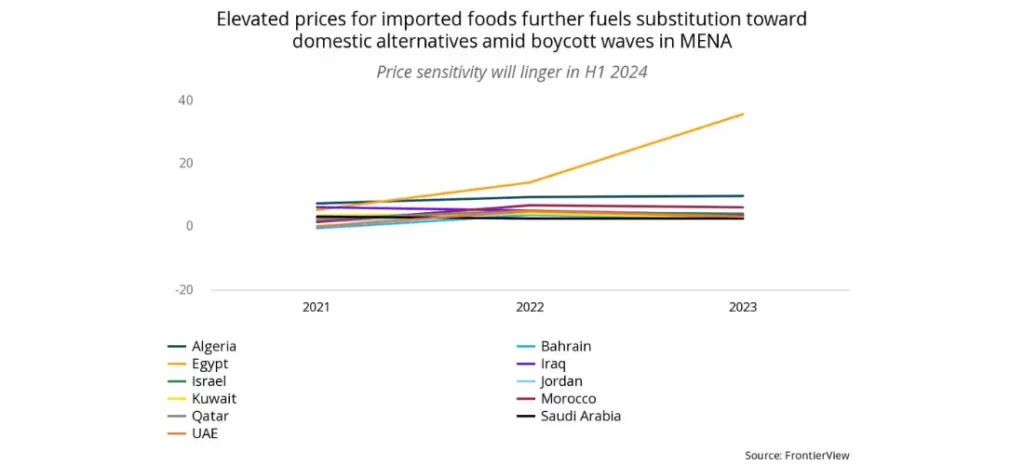

- Lingering price sensitivity in the region will further motivate some consumers to try out alternatives.

Actions to Take:

- Avoid insensitive marketing campaigns or events should the intensity of Israeli airstrikes on Gaza worsen.

- When resuming marketing campaigns, ensure to effectively align marketing with domestic and regional cultural trends to avoid the categorization as a purely foreign body. Some companies are already working with their local JV partners to ensure this, such as Carrefour.

- Undertake widened ESG activity, community-based practices, and/or charitable actions to further increase proximity to the domestic market and consumers.

- Evaluate if you have any risk of Israel-affiliated businesses among their suppliers of services and in their customer chain, and prepare mitigation plans in case of reputation damage in the region.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.