Uncertainty surrounding the approval of a 2025 budget will continue to pose risk of a credit downgrade

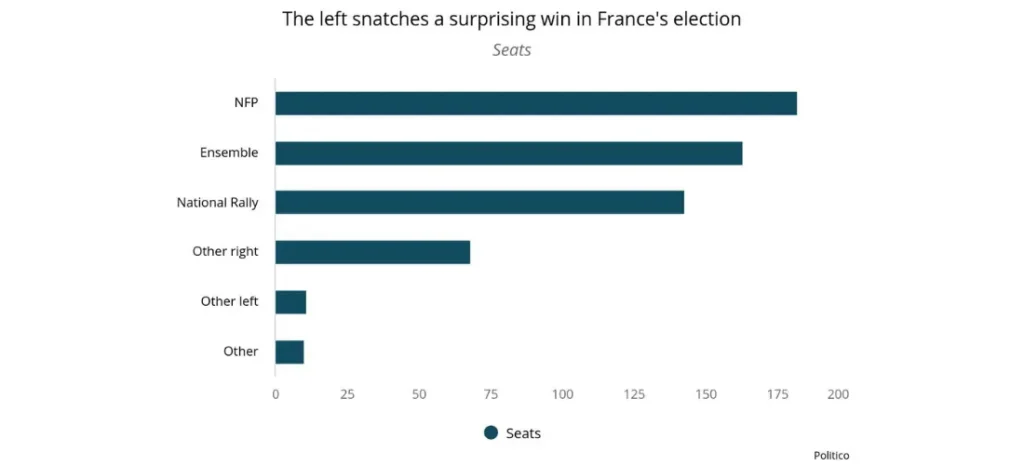

While the results of the second round of the French parliamentary elections are in line with our expectations that no single party will command a majority, an NFP victory was a definite surprise. The left-wing alliance managed to win 182 seats, following a pre-election decision by both the left and the center right to withdraw candidates strategically to prevent a National Rally victory. The latter came in third, behind President Emmanuel Macron’s Ensemble, and won 143 seats, falling significantly behind our earlier expectations of at least 180 seats. While the potential of a National Rally victory has spooked off markets due to its radical proposals when it comes to immigration and fiscal policy, the current situation continues to be a source of considerable uncertainty, especially given the persistent threat to public finances.

Business Implications

As we have maintained, an early election has been one of the key risks for businesses to monitor in 2024 and its implications could derail the otherwise relatively positive outlook for the market. France’s mounting deficit, which stood at 5.5% of GDP at the end of 2023, and rising public debt have already sparked a cutting spree by the government, but a recent credit downgrade by S&P and the launch of an Excessive Deficit Procedure (EDP) by the EU has increased the urgency to address public finances. France has until the end of September to present a long-term plan to address the mounting fiscal imbalances. Given the current political situation, the latter will be exceedingly difficult. Businesses should note that additional credit rating downgrades could not only have a negative impact on B2G demand but also lead to short-term EUR volatility and derail the European Central Bank’s (ECB’s) rate cutting trajectory, increasing projected borrowing costs through 2025 and weighing on domestic demand opportunities. The results will also likely stall the ongoing reform momentum, while the potential for policies that further erode public finances will weigh on the operational environment in the long term.

No decisive winner—what’s next?

Forming a new government is likely to take weeks and there are several options, but none of them provide a clear way out of the challenging economic situation. In the first scenario, the NFP could attempt to form a minority government but will require difficult-to-obtain support from other parties. Passing legislation will then be possible only through Article 49.3—a move the NFP has criticized the outgoing government and the president for. The NFP’s own fiscal program, which includes a drastic increase in minimum wages and pensions, a weaker pension reform, and a wealth tax, is likely to rattle markets and further deepen France’s fiscal challenges.

Alternatively, and more likely, the NFP and Ensemble could opt for a grand coalition based on compromise, but such a move would still require substantial concessions on both sides and may exacerbate existing fractures within the NFP. Equally likely is for President Macron to appoint a technocratic government to handle current affairs, but all his choices are likely to be seen as political and will likely mean that he would be forced to call another snap election in June 2025—the earliest time he can call for another vote. Finally, should political parties fail to reach a working agreement, Macron himself may be forced to resign, which will translate into another period of volatility and likely mobilize National Rally supporters, many of whom see the snap election as being practically stolen due to the de facto pre-electoral alliance between the NFP and Ensemble.

It is safe to say that high policy uncertainty will weigh on the market’s outlook and create an increasingly downside scenario for the economy. While we have abstained from revising our economic forecast significantly, based on the assumption that parties reach a cohabitation agreement that includes necessary fiscal adjustments and dissuade credit agencies from downgrading France’s credit rating and, at least partially, satisfy the EC’s call for fiscal restraint, risks are heavily tilted on the downside.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.