Despite a relatively limited impact on headline GDP figures, the recent uptick in tensions in the Red Sea is set to present significant operational challenges to multinationals in Europe. Companies that rely on trade with Asia, either in terms of exports or imports, will likely see a notable rise in transport costs and experience significant delays in the short term, as supply chain routes continue to adjust. Long-term renegotiation of shipping contracts, which normally occurs between March and May, may lock-in higher transport costs for longer, further complicating the supply outlook for 2024. Rising risk premiums are also set to bite into margins, with the ability of multinationals to pass through the price increases onto customers likely to be constrained by the soft demand environment across Europe. Most importantly, multinationals should monitor the situation closely; while the Houthis have so far abstained from targeting energy shipping, a potential escalation of tensions may lead to severe supply disruptions and an uptick in oil and gas prices throughout Europe.

Overview

- Rising tensions in the MENA region and the most recent string of attacks by the Houthis in the Red Sea are adding additional pressures on European manufacturers and supply chains.

- The attacks are mostly affecting cargo ships sailing between Asia and Europe, adding two weeks of travel to the otherwise average 35-day trip, as ships are taking the longer route around the Cape of Good Hope.

- The attacks have raised spot freight rates, with the Freightos Container Index seeing a jump of US$ 3,094 on January 18, 2024 from the US$ 1,270 during the first week of December 2023.

- The attacks have caused significant cargo delays and congestion in major European ports, and they are also increasing insurance premiums for ships still using the Red Sea—to 1.0% of the value of the ship from 0.05% prior to the crisis.

- The Houthi attacks seem to be predominantly targeting container ships and have avoided attacks on tankers or Chinese ships, but the latter have still been hit by the higher insurance premiums.

- US and UK attacks on the Houthis have exacerbated pressures, and while diminishing their ability to directly endanger ships, have not managed to prevent disruptions to supply chains.

- The EU is reportedly considering a joint naval mission in the region to secure safe passage, but details remain scant, and the response will be complicated by the bloc’s aim to increase pressure on Israel to deescalate the latter’s war in Gaza.

Our View

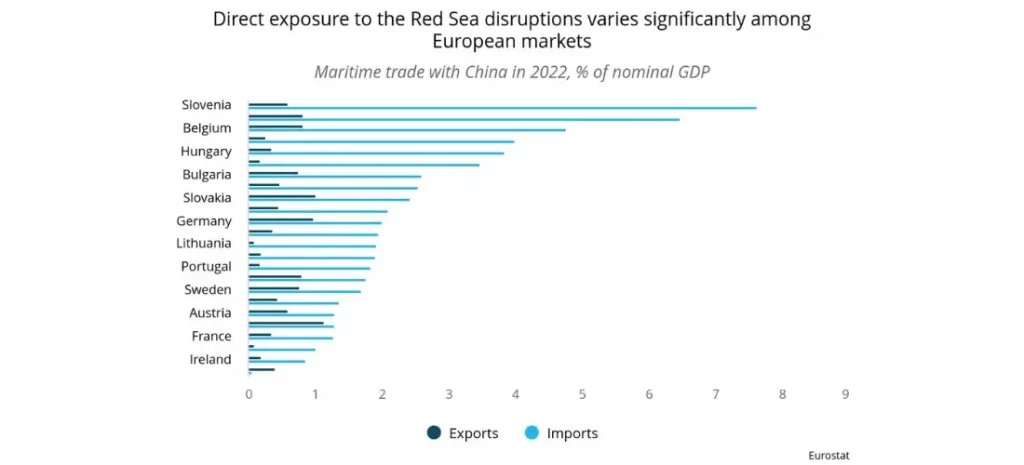

With 12% of global trade passing through Suez and the Red Sea, the recent bouts of supply chain disruptions, stemming from rising geopolitical pressures in the MENA region, are set to present another set of challenges to multinationals operating in Europe. With around 60% of Chinese goods shipped to the EU through the Red Sea, the ongoing disruptions are set to particularly affect manufacturers that are reliant on inputs from China. The most immediate impact of the crisis has been a notable jump in shipping costs and insurance premiums, which are likely to feed through European economies in the form of higher producer prices; however, the overall effect has so far remained relatively contained, with shipping companies adjusting routes at an expedient pace. Still, the ability of multinationals to pass through the jump in costs to customers will be constrained by the difficult price environment in Europe and the ongoing slump in demand, indicating that companies are set to see an exacerbation of margin pressures. Additionally, the jump in costs remains below the post-COVID-19 jump in shipping costs, which reached more than US$ 15,000 at the start of 2022, but supply challenges are likely to linger through the majority of 2024, with the risk of escalation of tensions highlighting the persistent danger to European supply chains. Germany, Hungary, Slovakia, and Belgium are particularly vulnerable to the disruptions, given their high direct exposure to Asian maritime trade, but the overall impact on growth should be fairly limited and, for now, has not necessitated substantial revisions to our forecasts for these markets. While broader CE direct export exposure is relatively limited, indirect exposure to supply chain disruptions through the CE’s integration into broader WEUR supply chains may weigh on the short-term manufacturing outlook. In terms of specific industries, the automotive sector’s reliance on “just in time” supply deliveries may complicate output planning and translate into notable delays in production, with major producers, such as Volvo and Tesla, announcing they will need to pause production in light of mounting shortages of components. Light manufacturing industries, including textiles and FMCGs, which are more likely to have built up their stock, are less vulnerable to the Red Sea disruptions, but they have indicated that they expect logistical costs to remain elevated along with delays in deliveries. The fall in just-in-time dependency (9.2% of companies in 2023 versus 14.0% in 2021) should also help alleviate some of the immediate pressures.

In terms of Russian oil, despite escalating fears, the Red Sea route remains the preferred option for traders transporting Russian crude oil to India. A Houthi politburo member has assured the safety of shipping lanes for vessels from China and Russia if they are not connected with Israel. In 2023, Russian oil constituted more than 35% of India’s total crude imports. If tensions escalate and insurance premiums rise, these may intensify competition between Russia and Saudi Arabia, whose tankers to Asia circumvent the Suez Canal, for the Indian market. Given that India currently stands as the second-largest buyer of Russian oil, any loss in market share will hit Russian export revenues hard. Meanwhile, a portion of Ukrainian food exports, mainly grain, is directed toward Asia and Africa through the Red Sea. The Ukrainian agriculture minister anticipates a 20% MOM decline in maritime grain exports for January due to disruptions in the Red Sea and seasonal factors. Before the war, about one-third of Ukrainian food exports were going to these regions, meaning that disruptions may lead to a notable revenue loss for the war-torn Ukrainian economy.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.