Fiscal pressures will remain across SSA despite debt restructuring progress offering some relief to governments’ spending capacity

Multinationals should review their demand assumptions to ensure they reflect potential improvements in opportunities in countries currently in the process of exiting default. Regular market monitoring of the latest debt-related developments will allow multinationals or their local partners to be in a position to capitalize on sudden and sustained revivals in both public and private sector demand conditions. This may necessitate expanding product portfolios or helping local partners raise their technical capabilities or business development skills. Conversely, firms should ensure they account for the effects that protracted austerity measures will have on their commercial performance in countries seeking to avoid default. For example, preparing drawn-out and tough pricing negotiations and offering cost-saving solutions to public sector customers will help multinationals remain competitive.

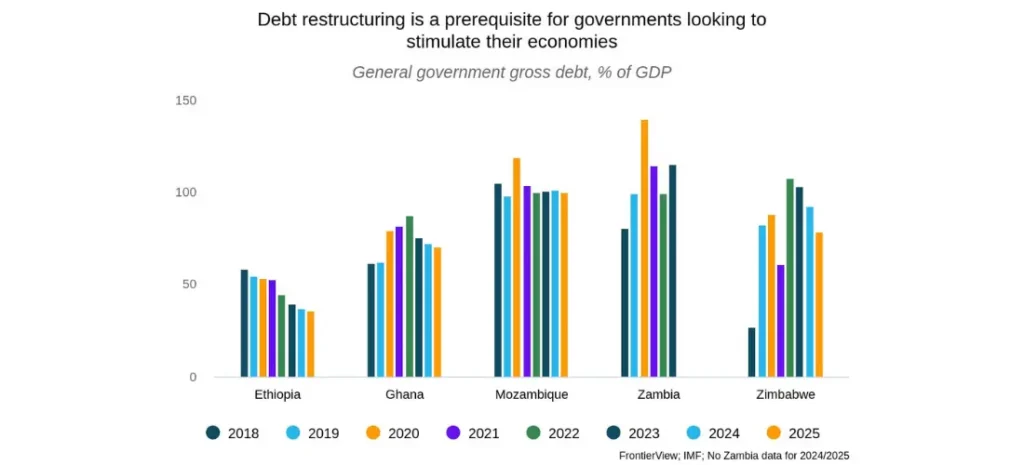

Overview

- The double shock of the COVID-19 pandemic and supply chain disruptions caused by the Russia-Ukraine war significantly increased fiscal pressures across Sub-Saharan Africa, leading to a series of debt defaults in SSA including Zambia (2020), Ghana (2022), and Ethiopia (2023).

- Zambia and Ghana are restructuring their debt under the newly introduced G20 framework that helps highly indebted low-income countries coordinate debt restructuring among their oft-disparate creditors. While Zambia is on the verge of finalizing its restructuring process following an agreement with the Eurobond-holder’s creditor committee in March 2024, Ghana has yet to reach an agreement with its private creditors.

- Ethiopia has been in negotiations with the IMF involving a loan and reform package since the start of the year, but progress has been slow, likely because the government has resisted implementing painful structural economic reforms such as depreciation of the birr.

- Zimbabwe is still negotiating with debt holders on its external debt worth an estimated USD 18 billion following its default in 1999, whereas Mozambique has battled to raise its credit rating and access external financing since technically exiting default in 2019.

Our View

FrontierView does not expect additional SSA countries to default on their external debt obligations this year because of extensive IMF support, falling global interest rates, and concerted efforts by governments to slash budget deficits through austerity measures. However, fiscal pressures will persist across several of the region’s largest economies, including Angola, Kenya, Mozambique, Nigeria, and South Africa. This will restrict government capacity to stimulate economic growth, raise prospects of tax hikes, and constrain public sector investment and procurement of goods and services. Nonetheless, progress made by countries that are currently in default but that are seeking to regain access to international capital markets will boost GDP growth and offer new opportunities for multinationals. Following Zambia’s March 2024 deal with Eurobond holders to restructure its debt, the country will likely exit default in early H2 2024 after a three-year process. This will provide some relief to the kwacha in the long run, but the severe drought will impact the currency’s outlook in the immediate term as copper production stagnates. Moreover, government spending priorities for the rest of 2024 will shift toward securing electricity, food, and support for residents. Conversely, Ghana is expected to formally exit default only in late H2 2024, as it is still negotiating with private bondholders, who hold the majority of the country’s external debt (estimated at USD 13 billion). Ghana’s economy will reap the benefits of exiting default in 2025, allowing it to regain access to global credit markets, slightly increasing the government’s spending capacity, and attract FDI, which will support the cedi’s value. Ethiopia’s government is expected to begrudgingly agree to devalue its currency in Q3 2024 in order to secure IMF and World Bank funding that will boost public finances, ease FOREX shortages, and improve investor confidence.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.