Egypt’s government will remain severely constrained in spending capacity by its large debt load

B2G firms targeting Egypt should maintain a conservative risk management approach during the 2024/2025 fiscal year. Pressures to reduce pricing and lengthen payment schedules will remain significant as the state deals with record debt payments and copes with the fallout from reduced FX receipts from the Suez Canal and gas exports. Anticipate a sharp real-terms drop in CAPEX spending and delays in public opportunities in 2024/2025, with repayment delays continuing to average about six months during the period. Firms should expect projects in strategic sectors such as oil & gas, tourism, and accommodation, and renewable energy to benefit from special government focus and a host of subsidies and incentives, including for exports. Most works in 2024/2025 will be concentrated on projects that are relatively near completion, including the New Administrative Capital and select transportation lines.

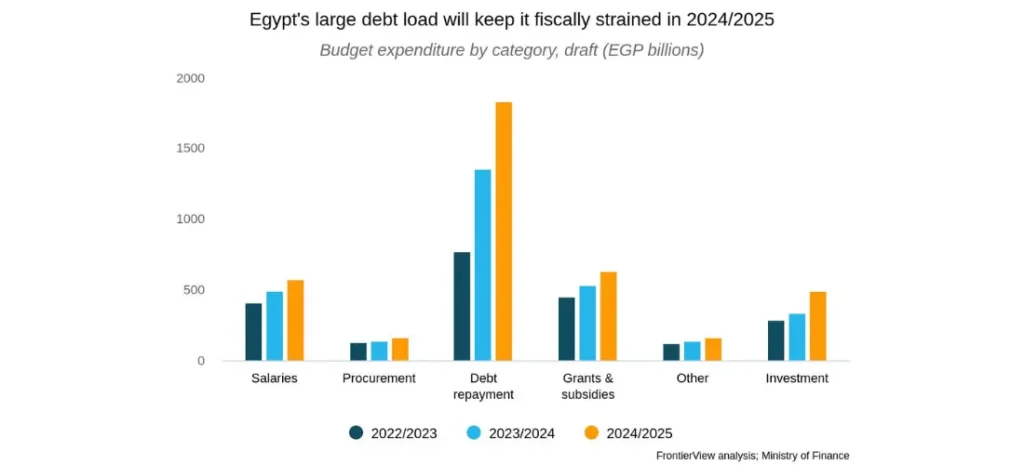

Overview

- In nominal terms, expenditure is budgeted to rise by 29.0% in 2024/2025 from the expected spending for the previous fiscal year, to EGP 3,870.2 billion.

- Consolidated revenues are forecast to increase by 8.5% to EGP 2,625.2 billion in 2024/2025, driven largely by taxes. Tax revenue is projected to rise by 30.4% during the fiscal year—an optimistic target; tax growth in 2023/2024 was budgeted at 32.2% versus the 23.2% projected by the year’s end.

- Egypt’s consolidated fiscal deficit will hit 7.3% of GDP in 2024/2025, up sharply from a projected 4.0% for 2023/2024. However, the primary deficit, which strips out interest payments, is projected at 3.5% for 2024/2025 versus 5.8% one year previously.

- Debt servicing will make up 47.4% of outlays in the proposed FY 2024/2025 budget, up from 37.4% in 2023/2024 and 35.4% in 2022/2023.

- Although spending on grants and subsidies will grow by 19.4% YOY in 2024/2025, such spending will once again fall as a percentage of total expenditure, to 16.4% (2023/2024: 17.7%; 2022/2023: 20.8%).

- Outlays on salaries and wages are projected to increase by 16.4% YOY to EGP 575.0 billion in 2024/2025. This follows on growth of 19.7% in 2023/2024.

- Investment under the general budget will increase by 48.5% YOY to EGP 495.8 billion in 2024/2025. However, this figure gives an incomplete picture, as most public investment is carried out by SOEs and economic agencies with independent budgets, and Egypt’s government has committed to capping total investment at EGP 1.0 trillion in 2024/2025.

- Procurement will grow by 22.1% YOY in nominal terms to EGP 166.7 billion in 2024/25.

Our View

Egypt’s large debt burden means the government will continue to face severe fiscal constraints in 2024. Egypt’s domestic debt will carry a servicing burden of EGP 1,602.3 billion in 2024/2025, an increase of 32.7% YOY. Although this marks a slowdown from the growth rate of 81.3% recorded in 2023/2024, actual spending is likely to overshoot targets once again as the central bank raises interest rates. Servicing on Egypt’s external debt will grow at an even faster rate, climbing by 52.1% in 2024/2025 to EGP 231.6 billion. This marks another year of rapid growth in interest outlays on external debt (2023/2024: 41.6%).

In 2024, fiscal pressures will once again reduce the appetite for public investment. Egypt’s government has committed to capping the value of investments in 2024/2025 at EGP 1.0 trillion as part of its assistance program with the IMF. Direct spending by the treasury on investment projects will increase by just 13% in nominal terms in 2024/2025, and investments under the general budget are largely financed through retained project earnings, with the rate of spending dictated by the availability of funds for reinvestment. Buildings and construction have been allocated 67.4% of investment outlays under the proposed 2024/2025 budget, down from 82.4% in 2023/2024. Nevertheless, spending on this category will increase by 39.0% YOY to EGP 334.0 billion. Meanwhile, spending on machinery and equipment will more than double in 2024/2025 to EGP 111.4 billion. However, it is worth noting that, in the previous fiscal year, investment in the buildings and construction and machinery and equipment categories underperformed targets by 50.3% and 17.2%.

Growth in overall procurement spending is likely to underperform the inflation rate in 2024, marking a real cut to procurement outlays during the period. Maintenance equipment will continue to make up the largest component of procurement spending in 2024/2025, at a projected EGP 23.1 billion—up by 66.5% YOY.

Egypt’s government will continue to prioritize social support measures through the 12- to 24-month horizon as households’ purchasing power comes under renewed pressure. Pension fund contributions will increase by 5.9% YOY in 2024/2025—a similar rate of growth to that seen in 2023/2024. Additionally, social solidarity payments and the Takaful & Karama allowance program will see outlays rise by 8.1% in 2024/2025, following expected growth of 55.9% in 2023/2024. Together, such payments make up 28.7% of Egypt’s budgeted subsidy bill for 2024/2025 (2023/2024: 32.2%).

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.