Expect intensifying customer pushback on price increases

Consumer goods companies should plan to face higher levels of demand elasticity and higher propensities to trade down among APAC households in 2024. This dynamic will be especially pronounced in segments where demand was supercharged by the pandemic and replacement cycles are extended (e.g., consumer durables). It will also be pronounced in China, where low inflation levels (or possibly even continued deflation) will leave companies little breathing room on pricing.

As a result, manufacturers serving consumer goods companies should expect to see intensifying pushback over incremental price increases, particularly in industries with relatively subdued input cost environments. Where possible, B2B sales and marketing teams should highlight cost savings and tangible product improvements in their scripting, as these value propositions are likely to resonate this year even more than they did last year.

Overview

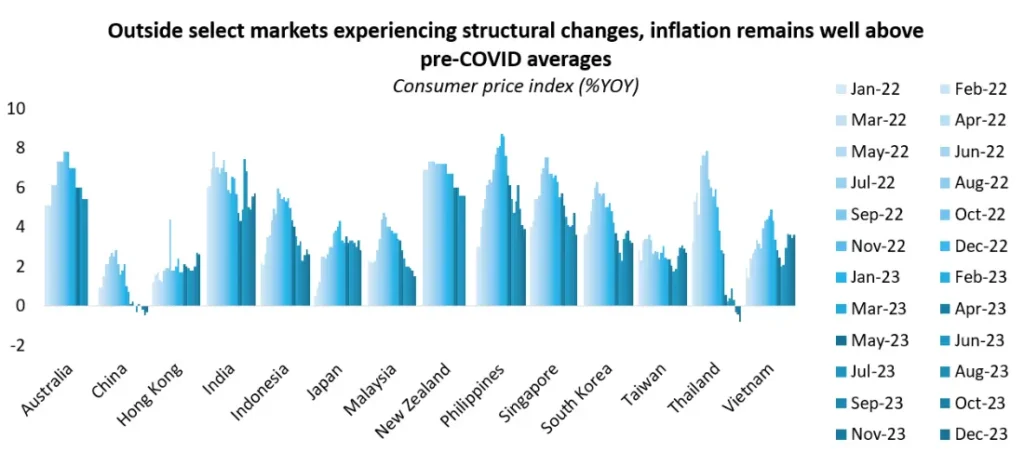

- Most Asia Pacific markets ended last year with uncomfortably high levels of consumer price inflation (CPI).

- This was particularly true in developed markets. For example, the latest CPI readings for Japan and Australia came in, respectively, around 2.3 and 2.2 percentage points above their 2010–2019 averages.

- The one market that clearly broke with this trend was China, which has been flirting with deflation since Q2 2023 due to weak consumer demand. It ended the year with three straight CPI readings between 0% and -0.5% YOY.

Our View

CPI rates have been elevated across most APAC markets over the last few years for the same reasons they have been elsewhere: supply-side issues (e.g., shortages and input cost inflation) and companies’ drive to recover margins squeezed by the pandemic. In some markets, inflation was also bolstered by government stimulus and strong household balance sheets.

While supply-side pressures have largely subsided, companies are still pushing price increases, and most APAC markets still have some way to go before achieving the inflation rates seen prior to the pandemic. Some markets, such as Australia, Japan, and New Zealand, are dealing with especially high rates (relative to their historical levels). Others, such as South Korea and Vietnam, have recently seen inflation figures bounce back.

As a result, while CPI rates in most markets should continue to slow over the course of the year, they are likely to remain elevated relative to pre-pandemic norms.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.