Uncertainty regarding the Gaza War feeds into scope of Red Sea disruption

Disruption to shipping in the Red Sea and Suez Canal will remain at a high level for as long as Israel persists with its war in Gaza or for as long as Israeli military operations there continue to result in an unprecedentedly high civilian death toll and damage to civilian infrastructure. Persistent and damaging attacks on Red Sea shipping from Houthi-controlled Yemen are likely to continue until at least April 2024, with a longer time frame possible should a meaningful Israeli de-escalation in Gaza fail to materialize.

Key Developments:

- Since late November, Houthi militants have launched several missile, drone, and boat attacks on commercial vessels transiting the Bab al-Mandeb entrance to the Red Sea. The US has responded by establishing a multinational naval task force and launching airstrikes on Houthi assets. Most major shipping companies continue to suspend Red Sea services and reroute vessels around the Cape.

- Shipping through the Red Sea has fallen heavily. From January 12 to January 16, 114 vessels were observed crossing the Bab al-Mandeb. This is down sharply from the 272 vessels observed during the corresponding period one month prior. The number of cargo ships transiting the Bab el-Mandeb fell to 12 from 53 during the period.

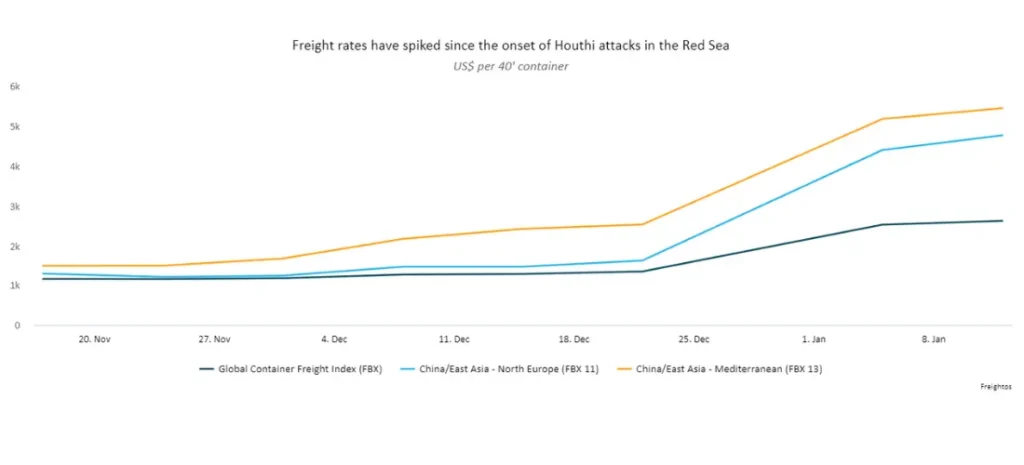

- Freight rates have spiked over recent weeks. The benchmark Global Container Freight Index rose by 150% from US$ 1,048 per 40’ container on October 20, 2023 to US$ 2,613 on January 12, 2024. Over the same period, the price of shipping a container from China/East Asia to North European or Mediterranean ports via Suez shot up fourfold and threefold, respectively.

- Rates for cargoes headed to Israel have risen sharply from already-high levels. In January, shipping giant MSC increased its Israel rate from US$ 6,000 to US$ 7,000 per 40’ container. Meanwhile, a number of East Asian shippers have publicly or silently suspended service to Israel, and there have been reports of ship crews asking not to sail to the country.

Short-term Outlook: FrontierView expects disruptions to Red Sea level to persist at some level until April 2024. A period of at least 2–3 weeks with zero maritime incidents in the Red Sea would likely be needed to lower shipping firms’ risk perception and for traffic in the area to gradually normalize.

US airstrikes on Houthi assets are unlikely to result in a permanent cessation of Houthi attacks, keeping shipping firms’ risk perception heightened over the next 1–2 months. Since 2015, Houthi military capabilities have proven resilient to intensive attacks from the air, and the group has in the past mounted successful attacks against Saudi Arabia and the UAE. It is unlikely that the US will risk expanding the war to include the Houthis’ Iranian backers and the Gulf States by drawing renewed Houthi attacks on neighboring countries.

Risks to Monitor: Monitor the development and intensity of Israel’s military operations in the Gaza Strip and Southern Lebanon to gauge the likelihood of de-escalation in the Red Sea. While a limited military tit-for-tat can be expected to continue over the coming month between the Houthis and US forces, an effective ceasefire in Gaza or at least a substantive Israeli move toward targeted hits on the Hamas leadership would likely lead to de-escalation of Houthi attacks in the Red Sea. Conversely, an expansion of the war to encompass Hezbollah and Lebanon would raise the possibility of disruptions to Red Sea shipping persisting for the whole of 2024. For domestic and international political reasons, the Houthis would be unlikely to persist with attacks in the event of a durable ceasefire or significant de-escalation of the violence in Gaza.

Key Implications:

- Israel: The cost of imported goods will rise in Israel during 2024, reflecting higher shipping and insurance costs. Effects will be concentrated largely in the durable goods category, particularly automobiles. Imported semi-durables will be affected to a lesser extent. However, our base case continues to envision a decline in Israel’s average CPI inflation from 4.2% in 2023 to between 2.0% and 3.0% in 2024, reflecting the impact of the war on consumer spending and confidence. Israel possesses significant domestic shipping capacity and has activated an overland freight route traversing Jordan and the GCC states, putting a cap on the level of prospective logistical disruption. Over the medium term, some Israeli firms may begin diversifying away from Chinese suppliers in light of Chinese shippers’ reported willingness to comply with Houthi demands in the Red Sea.

- Egypt: Disruption in the Red Sea will accelerate the expected trend toward FX volatility in 2024. A decrease of 50% in Suez Canal revenues for a period of two months could cost Egypt nearly US$ 1.0 billion in FX inflows, even as the country faces a record level of debt repayments in 2024. The disruptions also hamper reported plans of securitizing FX cash flows from the canal to help repay maturing external debts. FrontierView continues to expect Egypt’s central bank to begin devaluing the currency from February 2024, with our base case projecting an average depreciation of about 33% to EGP 41.0/US$ over the course of the year.

- Jordan: FrontierView expects Red Sea disruptions to impact Jordanian exports and imports. This will likely result in inflationary pressures through H1 2024. Jordan’s Red Sea port of Aqaba receives nearly one-third of its imports and is used for more than 50% of its exports. The Kingdom’s exports of potash and phosphate fertilizer, which account for about 3% of GDP, largely leave the country through Aqaba, which is also Jordan’s only container port and acts as a crucial hub for transit to elsewhere in the region.

Actions to Take:

- Multinationals should prepare for an increase in shipping costs over the short term and plan for the possibility of significantly increased freight rates in 2024.

- Multinationals should utilize scenario planning to adapt their businesses to a rapidly developing situation and prepare for a range of contingencies and a war of varying length, intensity, and scope.

- Increased price sensitivity among consumers after years of high inflation means that an increase in shipping costs that translates into higher final prices could put further pressure on already-weak consumer recoveries expected for 2024, particularly in Egypt. Any prolonged disruption to inbound shipping from Asia could significantly raise prices for capital goods in 2024, constraining already-tight private investment by Egyptian businesses and further extending project timelines for private and government projects.

- In Israel, anticipate a significant drop in consumer confidence compared to pre-war levels and a decrease in demand for durable goods and big-ticket items through at least Q1 2024.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.