Firms should prepare for changes in Japan’s operational environment that will likely arise due to higher interest rates

The immediate business impact of Tokyo’s small interest rate shift will be minimal; however, firms should note several items that are likely to emerge and intensify in the quarters and years ahead.

First, while the impact on the yen has been negative so far, a more hawkish stance from the Bank of Japan (BOJ) along with rate cuts from major central banks like the US Federal Reserve is likely to lead to substantive yen appreciation later in the year. Firms should develop their business plans for H2 2024 with this appreciation in mind. A stronger yen will provide greater pricing flexibility to firms that trade in USD, lower costs for local distributors and importers, and improve consumer sentiment.

Second, the cost of government debt repayments will increase. Nearly a quarter of the national budget was allocated toward debt obligations in FY 2024. As interest rates increase, this debt repayment burden will grow, and the government will have fewer funds to allocate to other budget items. Firms with B2G operations should re-evaluate their medium-term demand forecasts under higher interest rates and lower public spending.

Third, bankruptcies among Japanese “zombie firms”—unprofitable firms that have come to rely on cheap credit to stay in business—will increase. Even with negative interest rates, there were estimated to be over 550,000 zombie firms in Japan. With interest rates at 0.1%, this estimate rises to over 630,000 firms. A high incidence of bankruptcies among these firms will disrupt Japan’s operating environment, as these firms are crucial in retail distribution networks, supply chains for domestic producers, and regional tourism industries. Multinationals should proactively engage with local teams and partners to prevent any disruptions to cash flows and operations that could result due to higher interest rates. For example, after the BOJ policy decision, Honda Motor announced that it will pay its local suppliers in lump-sum payments instead of installments to improve their cash flow and prevent any operational disruption.

Overview

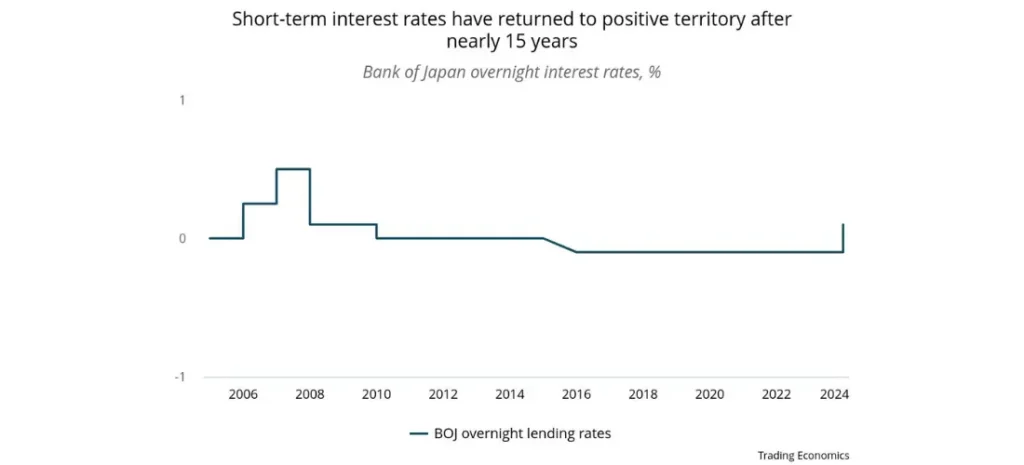

The Bank of Japan (BOJ) raised short-term interest rates for the first time in 17 years, ending an era of negative interest rates in the market. Overnight lending rates at the central bank were raised from -0.1% to a range of 0% to 0.1%. The central bank also announced that it would end its yield curve control program, where the BOJ would buy 10-year government bonds to ensure that their interest rates remained close to zero. Similarly, the central bank will stop purchases of exchange-traded funds (ETFs) and real estate investment trusts (REITs).

However, while yield curve controls have ceased, the BOJ will continue its purchases of government bonds for two reasons. First, by maintaining its bond-buying programs, the BOJ will ensure that long-term interest rates do not rise too rapidly. Second, by keeping long-term interest rates low, the central bank will maintain moderate stimulus in the economy to support growth, given subdued domestic demand trends.

In the days following the BOJ’s announcement, yields on 10-year government bonds fell by 0.05%, and the yen depreciated from approximately 149 against the USD to 151.

Our View

The BOJ’s decision to raise interest rates from -0.1% to a range between 0 and 0.1% was a largely symbolic move. It was a declaration that Japan has shifted away from its deflationary mindset and that the economy is on track to achieve a “virtuous cycle” of sustainable inflation and wage growth. To that extent, interest rates have nudged up ever so slightly, and therefore, any impact on the economy and financial markets is likely to be minimal in the short term. In fact, markets were expecting this move from the BOJ to come in March or April and were prepared to accommodate it. This is why the yen experienced depreciation after the increase in interest rates. A move away from negative interest rates was expected, but there was uncertainty about the forward guidance central bankers would provide. This forward guidance was decidedly dovish. The BOJ governor stated that the central bank would maintain an accommodative monetary policy and future rate increases would only come through slowly.

This approach was prudent. It seems unlikely that market conditions will evolve in such a way that allows for markedly higher interest rates. While the recent wage negotiations are a positive sign—with labor unions winning wage increases of 5.3% year over year—it remains to be seen whether similar levels of wage increases will go to all workers, as only 16% of Japanese workers have union representation. This is why even though unions secured 3.6% wage growth in 2023, average wages only went up by 1.3% YOY in the first nine months of FY 2023. Most SMEs do not have the capacity to raise wages at a similar pace as larger employers, especially as they are exposed to higher input and import costs. Without wages keeping pace with or surpassing inflation in 2024, consumer demand will remain lackluster, growth will be subdued, and inflation will continue trending downward. These will not be ideal conditions for the central bank to continue raising interest rates.

As a result, we do not expect additional substantive interest rate hikes in 2024. Short-term interest rates are likely to be raised just once more in 2024, with interest rates ending the year at a maximum of 0.25%. Two-year government bond yields are also near the 0.2% mark, signaling that markets also do not expect more than one rate hike in the next two years.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.