Multinationals operating in Russia may face further seizures as part of retaliatory measures by the Kremlin

Businesses should anticipate the war extending into 2025, as neither side shows a willingness to compromise on their maximalist objectives. The recent decision to secure a $50 billion loan from future revenues of frozen Russian sovereign assets is likely to provoke retaliatory actions from the Kremlin. This could potentially target Western companies, especially those from G7 countries, in areas where domestic capabilities can replace these firms, such as the retail sector. Multinationals operating in Central Asia, the South Caucasus, Turkey, UAE, Saudi Arabia, and China should be particularly cautious due to the risk of expanding secondary sanctions. It is also crucial for multinationals operating in CIS to work closely with their legal and compliance teams to avoid sanctions exposure. While country-wide sanctions against these nations seem unlikely, the situation demands vigilant monitoring and strategic adjustments to ensure business continuity and compliance.

Overview

On 24 June, the EU adopted its 14th sanctions package, which includes bans on helium imports from Russia, the re-export of LNG to third countries via EU territories, and new investments in ongoing Russian LNG projects such as Arctic LNG 2 and Murmansk LNG. This is the first package that targets Russia’s gas sector. However, the package does not prohibit the import of LNG to European countries which has in fact increased since the start of the war in 2022. The package also includes 61 new entities that help Russia import dual-use goods, including companies located in third countries such as China, Kazakhstan, the Kyrgyz Republic, Türkiye, and the UAE. The EU has also banned its entities from using Russia’s SPFS financial messaging service, Bank of Russia’s alternative to SWIFT, and from conducting transactions with certain listed entities utilizing SPFS outside of Russia. Earlier on June 12, the US Treasury imposed new sanctions on Russia, targeting foreign banks dealing with sanctioned entities, which also included the Moscow Exchange (MOEX) and its subsidiaries, forcing MOEX to halt dollar and euro trading, and redirecting transactions through banks.

Our View

The latest EU sanctions package demonstrates the EU’s commitment to crippling Russia’s war efforts and targeting third countries aiding Russia in bypassing sanctions. However, it is unlikely to significantly hinder Russia’s ability to acquire critical military components or substantially drain its financial resources. Approximately 10% of Russia’s LNG transshipments occur through Europe, and these sanctions are expected to cost Russia millions rather than billions of euros. On the other hand, oil revenues, Russia’s primary export earnings, are projected to rise by approximately 20% in 2024 compared to 2023, supporting its war machine.

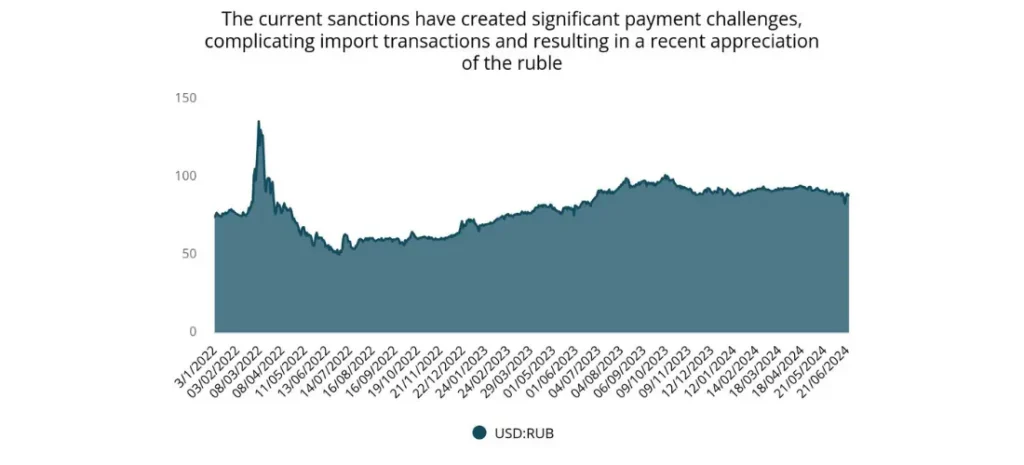

Concurrently, Russia’s payment problems have become more acute. The US financial sanctions have exerted considerable pressure on financial institutions in China, Türkiye, the UAE, and other countries, urging them to limit or cease transactions with Russia. This has led to noticeable moderation in Russian import growth, while exports remained robust, recently causing the ruble to temporarily appreciate to 82 per USD on June 19, the highest since June 2023, before stabilizing at 88-89 per USD. Continued payment limitations may further constrain imports, potentially exacerbating supply constraints and lowering productivity. While the recent sanctions on the Moscow Exchange are unlikely to result in a ruble crash, they will increase transaction costs for FX market participants.

On the domestic front, the situation is expected to remain fragile due to high terrorism-related risks and increased Ukrainian attacks deep inside Russia, leading to increased radicalism and armed attacks, particularly in Muslim-majority regions. The recent armed attack on the synagogue and churches in Derbent and Makhachkala, resulting in 20 deaths, including police officers and a priest, highlighted the country’s vulnerability and resource limitations to combat such threats amid the ongoing war. On the battlefield, Ukraine’s intensified attacks on Russian soil, supported by Western military supplies, will further worsen the situation, exemplified by the recent Crimea missile attack that caused civilian casualties. Nevertheless, we do not expect a major breakthrough on the battlefield in 2024 that could decisively end the hostilities and result in a clear victory for either side.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.