The deal will provide economic stability to the country, but will require tough reforms from the government

Pakistan and the IMF have come to a new staff agreement for a $7 billion deal. The new agreement is part of the IMF’s Extended Fund Facility and is a 37-month financing arrangement, a marked improvement from the nine-month, $3 billion Stand-By Agreement secured in July 2023. The new deal still needs to be approved by the IMF’s Executive Board, but this is largely just a formality.

Over the next three years, the IMF will aim to assist Pakistan in securing macroeconomic stability and creating more inclusive economic growth. These objectives will require further reforms to fiscal and monetary policy, a stronger tax base, and better management of state-owned enterprises. The Fund will also expect the government to invest in export-oriented industries, education, human capital, social protection schemes, and fair economic competition.

Business Implications

While the new deal with the IMF was widely expected, its confirmation will endow businesses with confidence in the stability of the economy. The threat of a debt default is no longer an immediate concern. The longer agreement with the IMF will also allow policymakers the necessary time to implement economic reforms and secure a stronger economic foundation for the market. Firms can look forward to economic, policy, and relative FX stability over the next 2-3 years, and contingency planning can take a back seat.

However, the economic stability that Pakistan has achieved will also limit its growth prospects in the near-term. The IMF deal comes with strict conditions, especially around increasing the tax-to-GDP ratio for the market. Higher taxes on salaried workers, agricultural incomes, and corporate incomes, as well as sales tax hikes, will weaken purchasing power across the economy. The increased tax burden will also limit investment and consumption growth. Firms should thus focus on optimizing their sales channels, marketing, and strategy execution in the near-term.

Finally, while economic stability will persist, political stability is not guaranteed. The country is likely to experience bursts of political instability or public unrest that will hinder, but not derail the government’s economic agenda. Strict enforcement of tax increases will heap additional pressure on a population that has had to endure an intense cost-of-living crisis, extreme weather events, and political unpredictability. Moreover, the Pakistan Tehreek-e-Insaaf (PTI), Imran Khan’s political party, has recently been banned. This is another source of public frustration, as the PTI was the most popular political party in February’s general election. Thus, the greater challenge for the government will be to secure buy-in from the public, its coalition partners, and other stakeholders to commit to these economic reforms over a three-year period.

Execution of policy reforms is now the key challenge

With the IMF deal secured, the onus is now on the government to follow through on the economic reforms it drafted. This will not be an easy task, as the key reform advocated by the IMF is to raise taxes. The government will face pushback on these policies, as well as their plans to raise electricity tariffs. Political maneuvering from opposition and coalition parties will mean that the Sharif-led administration and the Pakistan Muslim League-Nawaz (PML-N) must bear this criticism alone. Such conditions will make it challenging for the government to get buy-in from the public to accept these reforms.

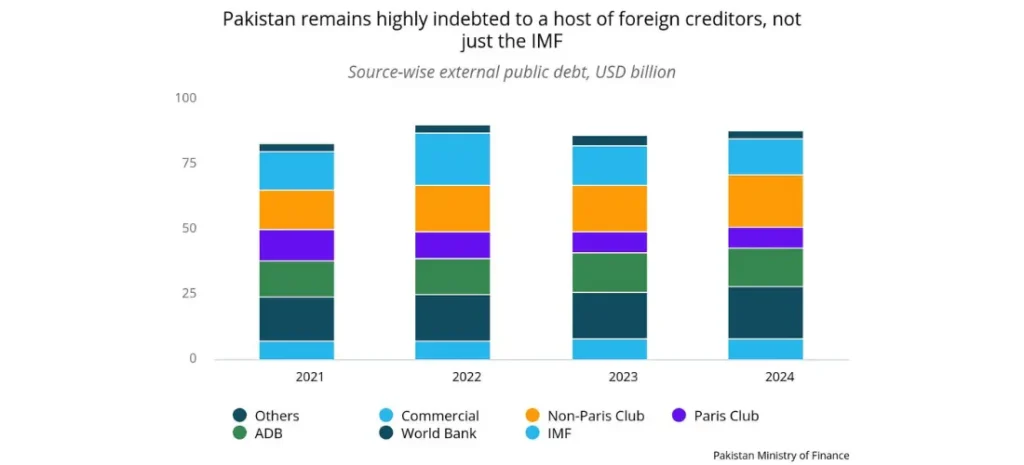

The government must maintain its commitment to reform despite these challenges. The funds are set to be released by the IMF in stages, and it is crucial for the government to demonstrate its willingness to make tough choices to retain the IMF’s support. The success of the caretaker regime and interim government in following the IMF’s guidelines paved the way for a more substantial deal with the IMF this time. However, those governments were not accountable to the public, unlike the current government. Strong resolve demonstrated by the government in the face of public pushback will be necessary to appease foreign lenders. The government’s willingness to initiate reform, along with the continued support from the IMF, will also instill confidence in other lenders such as China, Saudi Arabia, and the UAE to extend their debt payments and provide favorable financing conditions to Pakistan moving forward.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.