However, rates will remain elevated in 2024 and beyond

The Fed’s rhetorical pivot toward loosening is positive news, but multinationals should ensure they are not overly optimistic about the timing or the depth of cuts next year. While financial conditions will loosen compared with 2023, companies will continue to face historically elevated borrowing costs—those facing debt rollovers or with business models reliant on low interest rates stand most at risk. Companies selling into rate-sensitive sectors, such as residential and commercial real estate, big-ticket durables, and autos will continue to face disappointing demand until at least 2025. Finally, falling US interest rates will ease dollar strength, although minimally so given the continued attractiveness of dollar-denominated assets.

Overview

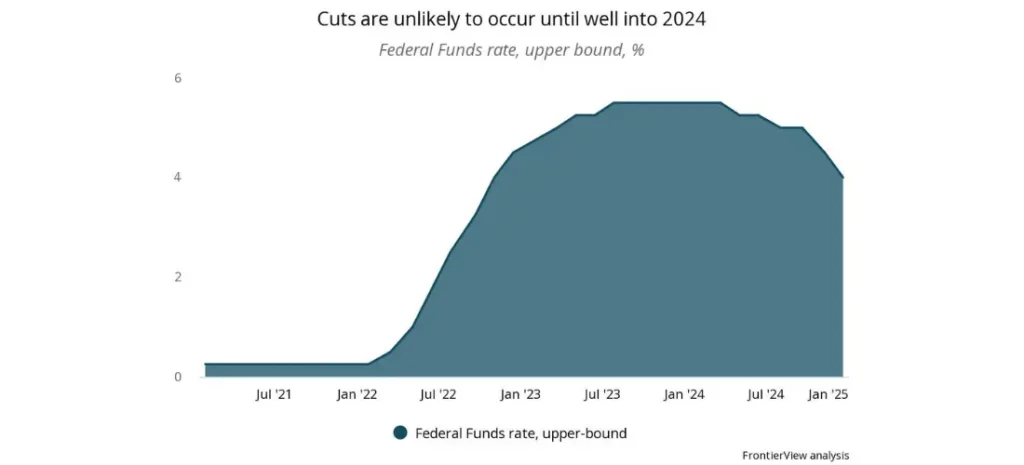

- At its December 2023 meeting, the Federal Reserve kept its benchmark rate unchanged at 5.50% (upper bound) for the third consecutive time.

- This comes following a soft inflation reading, with CPI coming in at 3.1% YOY in November. Inflation has been falling across the board, thanks to lower commodity prices and a rebalancing of labor market conditions that is slowing the pace of nominal wage growth.

- The Fed’s December meeting signaled an important shift in the central bank’s communication: for the first time in this monetary tightening cycle, it spoke about the timing and magnitude of rate cuts.

- FrontierView continues to expect around 150 basis points of rate cuts in 2024, beginning around the May 2024 meeting.

Our View

The Fed’s December meeting marked a turning point in the current monetary tightening cycle, which has been the most aggressive ever. Following cumulative hikes of 525 basis points, the Fed now appears to be done with tightening, after a string of positive inflation readings and labor market indicators showing a rebalancing of the supply and demand for workers.

Markets liked what they saw: equities rallied and bond yields fell following Fed chair Jay Powell’s announcement, as investors priced in further cuts for 2024. However, several Fed officials were forced to tone down some of their earlier statements, fearing that markets were expecting too many cuts.

Our view remains that the first cuts will come in Q2 2024, likely at the May FOMC meeting. These will be slow and tentative as the Fed assesses the impact of the rate cuts on inflation: we expect around 150 basis points worth of cuts throughout 2024, above the Fed’s own median estimate of 75 basis points. Crucially, we believe that much of the impact of higher rates has yet to be felt: one of the reasons the US economy performed so well in 2023, along with low unemployment and high excess savings, is that balance sheets are very healthy, with consumers and businesses alike being very proactive in refinancing during the pandemic when rates were at near-zero levels. But they will eventually need to refinance: the impact of higher interest rates is therefore likely to be felt for months and years to come. Still, we believe there are sufficient tailwinds in the US economy for it to avoid a significant slowdown.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.