While relatively unlikely, the region faces a multitude of risks that could develop rapidly

In our base-case forecast, the eastern CIS countries will enjoy robust performance in 2024 thanks to higher commodity prices, stronger budgets, and moderating inflation. Growth in the western CIS markets of Russia and Belarus will remain stagnant in 2024, as the ongoing war and sanctions are unlikely to end in 2024, while Ukraine is expected to sustain its recovery from the significant downturn experienced in 2022. Looking ahead, the Central Asia & Caucasus region is set to offer favorable business opportunities in the coming year. Doing business in Russia and Belarus will remain challenging amid rising market uncertainties. Meanwhile, some previous risks in the CE region have subsided, but 2024 will continue to pose challenges that will necessitate comprehensive scenario planning and preparation. There are several important potential events that multinationals need to monitor in the CIS and CE markets in 2024 (beyond those mentioned in our global report).

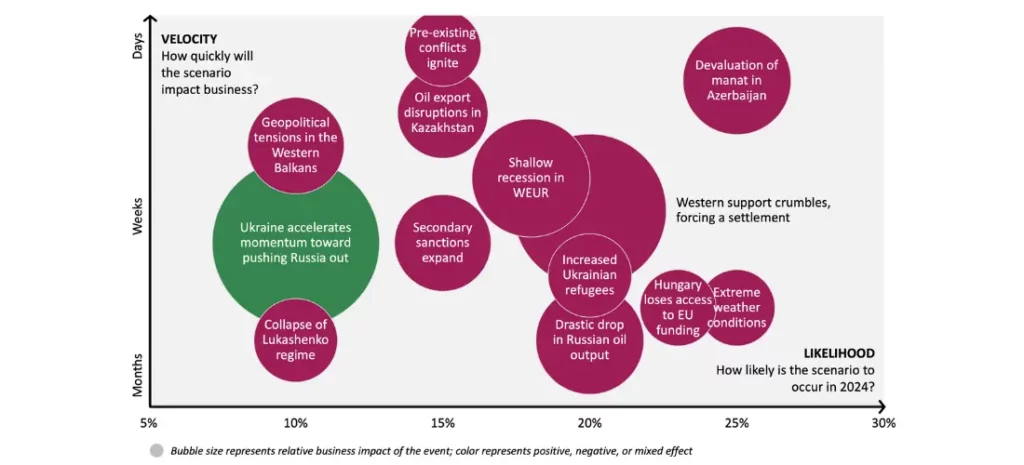

- Ukraine accelerates momentum toward pushing Russia out (10%): US President Joe Biden pushes through the US government’s support package for Ukraine in early January 2024. Ukraine, bolstered by new Western weaponry, successfully pushes back Russian forces on multiple fronts, including in Avdiivka, deeper within Kherson, allowing Ukraine to launch more successful missile attacks into Crimea. This success further reinforces Western support for Ukraine. Meanwhile, the Russian economy falters, resulting in a substantially weakened ruble, with an average exchange rate well above 100 to the US dollar, labor and product shortages, and elevated inflation. The conflict persists into 2025, driven by Ukraine’s unwavering determination to get all its territories back, while political infighting in Russia intensifies, creating domestic political instability. For the first time in more than 20 years, political competition arises for Russian President Vladimir Putin from high-level political figures. The Kremlin, facing a deteriorating economy and military setbacks, becomes more nervous and adopts a hostile stance, intensifying the seizure of foreign businesses/assets from “unfriendly” nations.

- Pre-existing conflicts ignite (15%): With tensions in Nagorno Karabakh appearing to subside, the return to a full-scale war between Armenia and Azerbaijan is highly unlikely. However, Russia’s interference in the domestic affairs of Georgia and Moldova due to their rising EU ambitions, border clashes between the Kyrgyz Republic and Tajikistan, and potential spillover violence from Afghanistan into Turkmenistan, Uzbekistan, and/or Tajikistan, pose ongoing risks to monitor in 2024. This scenario envisions the transformation of these pre-existing conflicts into aggressive domestic fighting, carrying operational risks and macroeconomic implications for multinationals, including currency weakening and higher inflation. However, such conflicts are unlikely to be prolonged or escalate into wider regional conflicts.

- Oil export disruptions in Kazakhstan (15%): About 80% of Kazakhstan’s oil exports to Europe traverse Russian territory via the Caspian Pipeline Consortium (CPC) that ends in the Novorossiysk port in the Black Sea. In 2022, CPC operations experienced four interruptions due to Russia’s retaliation against energy sanctions, an oil price cap, and President Kassym-Jomart Tokayev’s anti-war stance. A minor disruption occurred in July this year, primarily due to a power outage stemming from obsolete energy infrastructure. In August, a drone attack by Ukraine on Russian vessels in the Black Sea heightened the risk of potential disruptions to Kazakh oil exports. Any significant interruptions to CPC pipeline operations, whether from deliberate Russian interference or escalating tensions in the Black Sea, would negatively impact both growth and currency outlooks for Kazakhstan.

- Drastic drop in Russian oil output (20%): Russia’s oil production faces substantial challenges due to lack of Western financial investment, equipment, and expertise, resulting from stringent Western sanctions and the departure of Western oilfield services firms, and additional OPEC+ cuts further exacerbate the pressure on Russia’s oil output. While the base-case expectation is for oil output to average around 9.5 mb/d in 2024), this downside scenario envisions a decline to well below 9 mb/d. Coupled with a low Urals oil price, this sharp reduction in oil revenues triggers an economic decline in 2024. For the broader CIS region, this translates to a mass return of migrant laborers and substantial decreases in remittances and exports to Russia.

- Collapse of Lukashenko regime (10%): Several conditions must unfold for the potential downfall of Belarusian President Alexander Lukashenko. If compelled by Putin to engage in an unpopular and illegal war in Ukraine, Lukashenko, already unpopular domestically, risks destabilizing his regime. If Moscow cannot offer the necessary financing and security services to support Lukashenko’s regime, especially following a potential Russian defeat in the war and threats to Putin’s regime, Lukashenko would be unable to maintain his rule. This could lead to a collapse, both politically and economically, in the country.

- Western support crumbles, forcing a settlement (20%): In contrast to our base-case scenario, which assumes ongoing Western support, under this scenario faltering Western support to Ukraine results in significantly delayed and much smaller-than-anticipated military aid packages for Ukraine into late 2023 and early 2024. While Europe tries to fill in the gap, its ability to provide weapons is limited relative to the US, substantially hampering the Ukrainian war effort. Reduced Western support brings Ukraine to the negotiating table for a settlement with a long-term impact on geopolitics. The two countries engage in a protracted peace negotiation (well into 2025), resulting in a settlement that leaves some Ukrainian territory, plus Crimea, under “permanent” Russian control. Market uncertainty for multinationals continues due to lingering questions surrounding sanctions.

- Secondary sanctions (15%): There have been clear signs of parallel imports from Central Asia and South Caucasus to Russia in 2022–2023; however, only several companies and dozens of individuals from the region with links to Kremlin have been hit by the secondary sanctions so far. Contrary to our base-case assumption of ongoing secondary sanctions, under this scenario we assume that they are extended to large SOEs and banks in the region, and/or the export of certain items with dual use are completely banned to those countries. Such measures erode investor confidence, result in higher inflation for certain product categories, and weaken economic activity.

- Devaluation of manat in Azerbaijan (25%): Under our base-case scenario, the central bank transitions to a managed floating regime by the close of 2025, causing the depreciation of the manat. However, this scenario anticipates a devaluation in the upcoming year, strategically timed after the snap presidential elections in February 2024 to mitigate public discontent. The devaluation results in elevated inflation, negatively impacting consumption and growth prospects. Businesses, particularly those selling premium products, experience diminished demand and declining profit margins. This scenario also carries the risk of triggering financial instability, potentially leading to the closure of a few banks.

- Extreme weather conditions (25%): This scenario assumes acute weather conditions across the globe, and a heatwave during the summer months of 2024 leads prolonged droughts in Central Asia, exacerbating water scarcity for both farmers and households. This significant shock adversely affects agricultural growth, resulting in a surge in regional food prices. As spending on food products constitutes approximately 50% of total expenditures in Central Asia, this spike curtails consumption of non-food items. The escalating water crisis, coupled with difficulties in accessing clean water, also triggers domestic protests and cross-border tensions. This shock could also materialize in the form of heavy rainfall during the harvest period or flooding, with a similar contractionary impact on agricultural output. Severe weather across the rest of Europe could also have a substantial negative effect on the CE region, where a surge in food prices would lead to much stickier and more persistent headline inflation and weigh on the ability of monetary authorities to cut rates through H2 2024, which would derail growth and negatively affect consumption.

- Shallow recession in WEUR (20%): The CE remains highly exposed to shocks to WEUR, and potential disruptive events there could have a substantial effect on the overall performance of key CE markets. The potential of a shallow recession in WEUR, stemming from renewed interest rate pressures or fiscal issues in Italy, should thus also be closely monitored by CE executives.

- Hungary loses access to EU funding (25%): Hungary did not manage to secure access to EU funding in 2023, which has had a significant impact on the country’s fiscal balance and is one of the reasons for the full annual contraction of the economy and the notable easing of the HUF. While the EU has unfrozen some funding, most of it remains tied to the European Commission’s rule-of-law requirements. The Hungarian government will likely seek to obstruct EU policymaking and support for Ukraine in return for tranches of the funding, but should it fail to secure greater access to it, the economy will likely continue to underperform, preventing a more notable rebound in 2024.

- Increased refugee flows from Ukraine (20%): Another wave of Ukrainian refugees into the CE region remains intrinsically linked to the ability of Russia to intensify the conflict in Ukraine and on continuous Western support for Ukraine. Should the latter see a reduction and should Russia increase its bombing campaign over Ukrainian cities, the region will likely face another substantial wave of refugees. This will put significant strain on governments in the region and require considerable budgetary amendments. In addition, this might also increase pre-existing social tensions and translate into a more unpredictable policy environment across the CE.

- Geopolitical tensions in the Western Balkans (10%): Political tensions in Bosnia and Herzegovina, and between Serbia and Kosovo have seen a notable increase and have manifested in violent clashes with the police in Northern Kosovo. Controversial President of Republika Srpska Milorad Dodik has also threatened to declare independence from Bosnia, which would reignite existing ethnic and national tensions. Should tension manifest into regional violence, it is unlikely to translate into a full-scale interstate conflict, but it will likely lead to border clashes that will significantly erode the region’s performance.

Watch a video overview of the Russia & CIS Events to Watch for 2024

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.