Low demand and increasing price sensitivity will be challenges for manufacturers in 2024

The global manufacturing sector is experiencing its longest contraction in over 20 years, as it reckons with the impact of high inflation and elevated interest rates. Businesses should expect this dynamic to continue for the foreseeable future: interest rates will remain elevated well into 2024, and consumers will need time to rebuild their purchasing power. B2B multinationals should therefore expect subdued demand from the manufacturing sector, as well as increased price sensitivity from B2B customers. B2B companies may need a combination of product portfolio flexibility, service-based offerings, as well as strong differentiation with customers to sustain demand and pricing power. Multinationals should also ensure they are identifying and capturing opportunities in sectors such as defense, clean energy, electric vehicles, and semiconductors, which are subject to different, more positive dynamics.

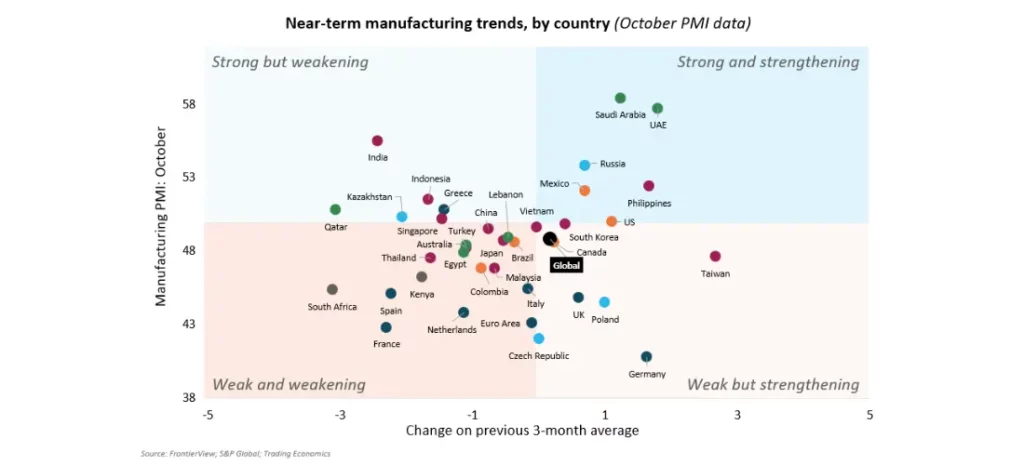

Overview

- The Global Manufacturing PMI Index came in at 48.8 in October, its fourteenth consecutive month in contractionary territory, marking the longest period of deterioration in over 20 years.

- The Output sub-index contracted for the fifth consecutive month, as global demand conditions continue to deteriorate.

- While the sluggishness is broad based, conditions are particularly poor in Europe, where low domestic and external demand are leading to contractions of manufacturing activity in almost all countries.

- Other major manufacturing economies, notably China and Japan, are suffering from low global demand, while also facing uncertain internal dynamics.

- Input costs have picked up in recent months, in large part due to the sizable increase in oil prices seen in Q3 2023. However, lower demand is deteriorating corporate pricing power and companies’ ability to pass higher energy bills to customers.

- Optimism among manufacturers has fallen to an 11-month low, leading to moderate cutbacks in manufacturing employment.

Our View

The manufacturing sector is down in the doldrums and shows few signs of improving anytime soon. Across the world, almost all economies are witnessing a deterioration in conditions, predominantly due to the continued softness in demand for manufactured goods, itself a product of high inflation and elevated borrowing costs. Manufacturers who, until now, had relied on backlogs to sustain activity and offset slowing order books, such as in the auto sector, are now facing a slowdown.

While manufacturers continue to expect conditions to improve globally in the next 12 months, the strength of this optimism is waning and reflects developments in the macroeconomic outlook. With 2024 set to be a year of high interest rates, continued price sensitivity, and historically elevated energy prices, there is limited scope for a strong rebound in manufacturing activity. This is leading to cutbacks in employment, which are likely to continue for the foreseeable future. However, these are and will continue to be moderate: manufacturers continue to face hiring difficulties and are therefore reluctant to shed their workforce too much.

Europe is the primary pain point, with Germany continuing to suffer a particularly acute manufacturing contraction as global demand for German durable goods grinds to a halt. Other major European economies, such as France, the UK, and Spain, are also beginning to show signs of a sustained contraction. In the US, a recent stabilization in manufacturing conditions has boosted optimism, but this belies a darkening outlook: growth is set to slow in 2024 in the US as consumers cut back on discretionary spending, while dollar strength will continue to weigh on the competitiveness of its exports.

The Chinese manufacturing sector is suffering the double whammy of weak domestic and global demand. At home, Chinese consumers are facing a crisis of confidence, and their spending is overwhelmingly directed toward services. Abroad, demand for durable goods, China’s main export, remains flat as inflation-hit consumers cut back on purchases of big-ticket, discretionary items. Manufacturers have resorted to discounting in order to stimulate demand, leading to deflation at factory gates. China’s recent CNY 1 trillion fiscal stimulus was a welcome announcement, but it remains to be seen the extent to which it will boost consumer and business confidence, and therefore manufacturing activity.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.