MNCs should continue to use scenario analysis to navigate heightened uncertainty

Representatives from the US and China held two-day trade talks in Geneva, Switzerland, over the past weekend. The US delegation was led by Treasury Secretary Scott Bessent and US Trade Representative Jamieson Greer, and the Chinese delegation was headed by Vice Premier He Lifeng. At the conclusion of the negotiation, the US agreed to lower the base level of tariffs on most Chinese goods to 30%, down from 145%, while China agreed to reduce its levies on US products to 10% from 125%. China also agreed to cease certain non-tariff measures it implemented in retaliation to the US tariffs. The 30% rate now imposed by the US includes a levy related to China’s alleged role in the fentanyl crisis plaguing the US — an issue discussed in the talks over the weekend.

However, the US tariff on many Chinese products will be higher than 30%, as tariffs on steel, aluminum, and autos remain in place, along with some earlier tariffs on specific Chinese goods imposed during President Trump’s first term and the tenure of former President Joe Biden.

Business implications:

MNCs that supply the US from China should act swiftly to take full advantage of the 90-day window to fulfill as many export orders as possible. Besides maximizing their China-based production capacity, they should promptly collaborate with partners along their supply and logistics chains to secure raw materials and shipping slots. The coming 90 days will likely be a hectic period for exporters, and MNCs must operate with agility and a quick-response strategy.

There will be cost implications for MNCs, as the current tariff levels remain significantly higher than they were before President Trump’s “liberation day” announcement. Regional executives should enhance communication with headquarters to discuss strategies for managing the rising costs of their products. Options include passing part of the cost increase to customers or absorbing some of it themselves. Regardless of the approach, it is crucial for regional teams to collaborate closely with headquarters to assess the precise impact on the company’s revenue and profit projections.

MNCs that supply China from the US can take a breath for now, especially those involved in the agricultural value chain, but they should remain vigilant. They should also make the most of this 90-day window to restock extensively. Meanwhile, companies that import raw materials and components from the US should persist in diversifying their sources of imports.

In the global market, the immediate threat of an influx of cheap Chinese goods may be temporarily alleviated, but MNCs should remain diligent in preparing for increased competition from Chinese companies. Given the high level of uncertainty surrounding the progress of US-China trade negotiations over the next 90 days, MNCs should use our scenarios to prepare for the worst-case outcome, such as a collapse in negotiations.

Despite the temporary de-escalation in the trade relationship between the US and China, MNCs with exposure to both countries should continue to invest in political acumen by engaging in diplomatic and strategic dialogues. This will help them stay informed about policy changes in both Beijing and Washington while advocating for their interests.

With US-China trade tensions likely to remain volatile in the near future, it’s imperative for MNCs to proactively develop and implement robust strategic plans. We consistently advise MNCs to use our scenarios to pressure test their forecasts and anticipate potential disruptions. Additionally, they should continue exploring alternative market opportunities to safeguard their operations and maintain their competitive advantage in an increasingly volatile global landscape.

Our View:

The outcome of the talks was more favorable than we previously anticipated, and we believe it benefits global trade and the economy, despite the “ceasefire” lasting only 90 days. The developments post the 90-day period remain uncertain.

What happens during the 90-day tariff pause?

Trade flows between the US and China will likely rise significantly as US customers aim to maximize the 90-day window to restock extensively. Similarly, China-based manufacturers will likely ramp up production to export to the US as much as possible. Factories might operate at full capacity, and slots on container ships bound for the US could fill up rapidly.

Domestically, the pressure on the Chinese government to release additional stimulus packages will lessen, making it more likely for China to reserve more resources until after the 90-day period expires in case the negotiations collapse. The issue of overcapacity will likely become less severe, and the amount of Chinese goods initially planned to be diverted to non-US markets will likely decrease as well.

Overall, China’s industrial production and GDP growth in Q2 will likely be revised upward. We are currently working on the numbers and will release them as soon as they’re available. The likelihood of China achieving its annual 5% growth target has increased.

Our new US-China trade war scenarios:

Based on the joint statement issued by the two countries following their discussions, we have revised our US-China trade war scenarios for the end of the 90-day tariff truce as follows:

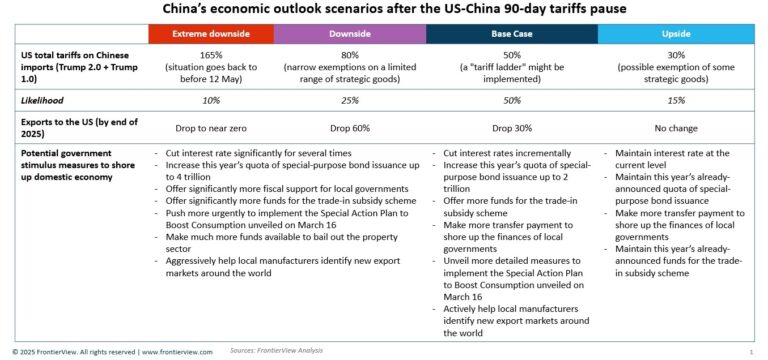

Upside (constructive rollback: 15% likelihood): In this scenario, during the US-China negotiations, China makes sincere and genuine pledges to crack down on fentanyl and perhaps even achieves significant progress in the 90-day period. Additionally, China would permanently remove most of the non-tariff measures implemented in retaliation against US tariffs, such as lifting export controls on critical rare earth elements and removing some US firms from its “Unreliable Entity List”. Furthermore, China’s antitrust cases against US MNCs, such as Google and DuPont, would likely be dropped.

This development greatly pleases President Trump, leading him to agree to remove the 20% so-called “fentanyl tariff”. As a result, US tariffs on Chinese goods would be reduced to 30%, comprising 10% from the universal tariffs under Trump 2.0 and 20% from tariffs under Trump 1.0. Some strategic goods would be even excluded from the 10% universal tariffs.

Base case (status quo extension: 50% likelihood): In this scenario, the US and China engage in multiple negotiation rounds during the 90-day period, but due to the complexity of their bilateral trade relationship, they are unable to conclude the discussions. However, President Trump is pleased with the progress and genuinely believes that a significant deal with China can be achieved — he simply needs more time. China also favors continuing the negotiations. Consequently, both sides agree to extend the negotiation period and maintain the existing tariffs at the level specified in the May 12 joint statement. For the US, this would mean that average tariffs on Chinese goods remain around 50%, comprising 10% universal tariffs, 20% fentanyl tariffs from Trump 2.0, and 20% tariffs from Trump 1.0. However, a “tariff ladder” might be implemented, such as 30% on consumer goods, 40% on intermediates, and over 50% on strategic goods, to better address the concerns of domestic industries and minimize the impact on them.

On the international stage, China would continue to apply a “divide and conquer” strategy to court countries traditionally aligned with the US, including select EU and ASEAN countries, as well as South Korea and Japan. This approach would further complicate the geopolitical landscape and increase uncertainty in economic and trade relations.

Downside (volatile tariff fluctuations: 25% likelihood): In this scenario, the US-China negotiations remain inconclusive after 90 days, and President Trump is dissatisfied with the progress. As a result, he reinstates some of the tariffs to exert more pressure on China in the hopes of expediting the negotiation process. US tariffs on Chinese goods would then be increased to 80%, consisting of 60% tariffs from Trump 2.0 and 20% tariffs from Trump 1.0. This is an amount Trump had publicly touted on social media the day before the US-China talks commenced in Switzerland. There will be exemptions, although these are likely to be narrow and apply only to a limited range of strategic goods. This approach aims to provide relief for US industries where necessary without significantly undermining the overall tariff strategy.

China is unlikely to remain passive. Globally, China will intensify its propaganda efforts, particularly within international organizations like the UN, to vilify the US and its allies. Concurrently, it will seek to bring as many Global South countries as possible into its orbit, focusing on nations in Southeast Asia, Latin America, the Caribbean, and Africa. Domestically, China might tighten export controls on select rare earth elements again and reopen investigations into prominent US-based MNCs with significant operations in China. Tools like the “Unreliable Entity List”, sanctions on US MNCs, or even a devaluation of the RMB will be reconsidered. Meanwhile, China will expedite the release of additional stimulus measures to bolster growth, particularly in consumption.

Extreme Downside (trade breakdown: 10% likelihood): In this scenario, US-China negotiations collapse after 90 days, or potentially sooner, prompting an angry President Trump to reinstate all previously imposed tariffs on China. Consequently, US tariffs on Chinese goods would be restored to 165%, consisting of 145% tariffs from Trump 2.0 and 20% tariffs from Trump 1.0.

China would almost certainly retaliate by reinstating all previously imposed tariffs on the US from February onwards, along with reintroducing all non-tariff measures. As a result, a full-blown trade war between the US and China resumes, and their trade relations would revert to the state before the May 12 joint statement, with trust plummeting to new lows and acrimony reaching new highs. This upheaval would cause new and more severe disruptions in the global trade system, and the risk of escalating geopolitical tensions would increase further.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.