Multinationals should review monetary policy on a national basis, as Central European rate policies diverge

Multinationals should assess the impact of rate changes on their operations on a national level across Central Europe, with increasing divergence in monetary policy. A broad trend of falling inflation and falling or stable rates, however, will ease financing pressures and support the expected rebound in consumer spending across the region.

Multinationals should review scenarios for Polish rates remaining higher than expected in H2 2024, with the National Bank of Poland (NBP) expressing concerns about resurgent inflation later in the year. The NBP’s inflation forecast, due to be released in March, will signal its direction for H2 2024.

Risks to the easing cycles across Central Europe remain, particularly if the European Central Bank (ECB) and US Federal Reserve choose to delay their easing cycles from Q2 2024. Multinationals should review downside planning to account for higher rates in Central Europe if ECB loosening begins later than expected, which would lead to higher credit costs and dampen the demand outlook.

Overview

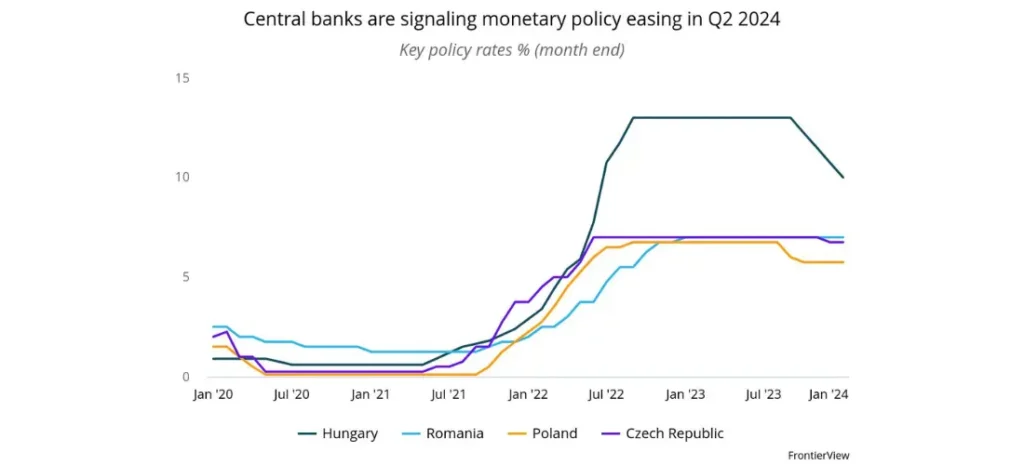

- The Czech National Bank has begun its easing cycle, cutting base rates 0.25% in December and a further 0.50% in February, as it became the first Central European country to see inflation fall to its target level in three years.

- Hungary’s central bank has cut rates 0.75% each month since November. Hungary’s rates are the highest in Europe, following large increases in core inflation, which reached as high as 25.7% YOY in Jan 2023.

- The National Bank of Poland signaled neutrality following a surprise 0.75% rate cut in September, which saw the zloty plunge 1.5% against the euro. Rates have held steady at 5.75% since October, with an announced hold on cuts until 2024, which calmed markets ahead of the parliamentary election that took place in December.

- The National Bank of Romania has kept rates steady at 7% since January 2023 and signaled it will leave rates unchanged until at least Q2 2024.

Our View

Monetary policy across Central Europe presents a nuanced picture, yet underlying commonalities among the nations persist. We anticipate a broad decline in rates across the region in 2024, following historically tight policies, with more pronounced easing expected from Q2 2024 onward. Our base-case scenario forecasts terminal rates in Poland at 4.75%, Romania at 5%, Hungary at 7%, and the Czech Republic at 4% by the end of 2024.

Inflation has noticeably receded since its peak in early 2023, largely due to significant moderation in energy prices. The Czech Republic and Hungary have seen inflation fall within their respective tolerance bands, indicating potential for imminent cuts in March and April 2024. However, Poland’s inflation rate stood at 3.9% in January, exceeding the NBP’s upper limit of 3.5%, thereby limiting options for further monetary policy loosening in Q1 2024. The NBP has been cautious in announcing a timeline for future cuts, opting to wait until it revises its inflation forecast in March, citing concerns over potential resurgent inflation in H2, following the expiration of energy subsidies and VAT cuts on food and beverages. Meanwhile, Romania continues to grapple with inflation significantly above its upper limit of 3.5%, with January’s year-on-year inflation rising by 0.8% MOM to 7.4%. Nonetheless, the National Bank of Romania provided moderately dovish indications when announcing policy would remain unchanged in February, emphasizing that inflation decreased faster than expected in Q4 2023, alongside a lower-than-expected fall in January’s inflation.

Still, some inflationary pressures persist, with double-digit increases in minimum wages across the region expected to increase upward inflationary pressure throughout H1 2024. We anticipate this pressure to manifest in inflation figures in Q2 and Q3 2024, as the lag effects of rebounds in consumption and increased wage costs, which producers are passing onto consumers, takes hold. Consequently, central banks in the region are likely to proceed with caution, with smaller 0.25% rate cuts in Q2 appearing more probable.

Foreign exchange pressures, characterized by divergent goals regarding the valuation of domestic currencies in the region, are further complicating the easing cycle. Romania’s central bank has signaled a reluctance to see its currency appreciate, owing to its large current account deficit following a 6.4% strengthening over the past two years, indicating that cuts are likely to be synchronized with the ECB. In contrast, the Czech Republic’s central bank in January suggested that rate cuts would have commenced sooner if not for a weak koruna. It further underscored how devaluation of the koruna is temporary and will be relieved when ECB rates loosen. While our viewpoint maintains ECB cuts will begin in Q2, any delay to easing would limit the extent of dovish policy by Central European central banks in Q2 2024.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.