The scale of the package is meager, so its impact is likely to be limited

Multinationals operating in the infrastructure or construction sectors are expected to gain from the stimulus package, particularly after the commencement of projects. However, this progression might be protracted due to a couple of reasons. First, most of the regions slated to receive the funds are in northern China, where winter weather conditions could potentially cause project delays in the next few months. Second, only half of the funds are allocated to be spent this year, thus it will take some time for the demand to gradually filter down the value chain.

Multinationals that are not directly involved in the industrial sector, such as those operating in the B2C space, are less likely to directly reap benefits from the stimulus package. Nevertheless, when all projects begin and the construction process gains momentum, there is a high possibility of overall demand improvement. This can be attributed to the payment received by workers, as well as small and medium-sized suppliers. Through the multiplier effect, the stimulus funds will thus be infused into the real economy, thereby increasing people’s disposable income, bolstering purchasing power, and boosting consumer confidence.

However, multinationals should not be overly optimistic about the stimulus package. First, the size of the stimulus is relatively modest by China’s standards, thus limiting the potential benefits that multinationals can accrue. Second, because a significant portion of the funds will be allocated to projects focused on disaster relief, the extent of their impact on the nationwide economy remains uncertain. Third, it is not unprecedented in China’s recent history for a substantial portion of stimulus funds to be wasted on unproductive and futile projects, commonly referred to as “white elephants,” which ultimately fail to stimulate growth. Given this historical context, one should not be surprised if history repeats itself.

Overview

- China recently announced that it will issue additional sovereign debt worth CNY 1 trillion (US$ 137 billion) to support growth.

- The issuance will happen in Q4 this year. CNY 500 billion of the proceeds will be used before the end of this year, and the other CNY 500 billion will be spent next year.

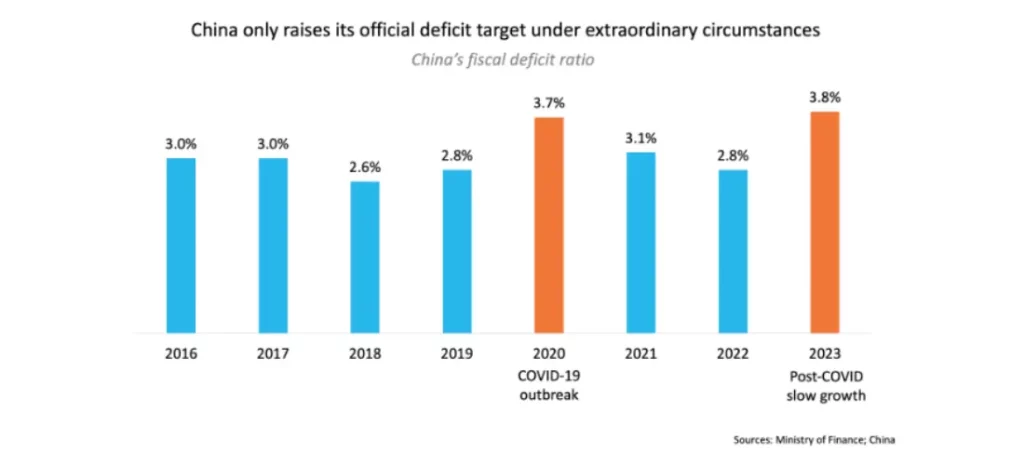

- As a result, China’s fiscal deficit ratio this year will rise to 3.8% of GDP, up from the target of 3% that was set at the beginning of 2023.

- China has explicitly stated that the funds generated from the new issuance will be allocated to local governments for their utilization, while the debt incurred will be shouldered by the central government.

- Furthermore, state media noted that the newly acquired funds should primarily be employed for addressing disaster relief and facilitating the post-disaster reconstruction efforts in regions severely affected by this summer’s floods.

Our View

A CNY 1 trillion stimulus package may appear substantial, but it is comparatively modest in the context of China’s historical standards, especially when compared to the CNY 4 trillion package that China swiftly implemented in response to the global financial crisis in 2008. (For comparison, the 2008 package amounted to more than 13.3% of GDP, while this package amounts to only 0.8% of GDP).

The impact of the stimulus is also likely to be extended over the next several quarters instead of concentrated in Q4 2023 or even Q1 2024. China has explicitly stated that only half of the funds will be allocated for expenditure this year, while the remaining half will be utilized in the following year. Additionally, because the majority of the natural disasters that struck China this year occurred in the northern and northeastern regions during the summer, and considering that these areas are now entering the winter season, it is likely that there will be minimal activities happening there regardless.

Nevertheless, this funding remains crucial for the recipient provinces, as it provides them with a substantial injection of capital without burdening them with debt concerns, because the central government bears the financial liability. Therefore, local governments will have the opportunity to effectively utilize these funds to stimulate growth through infrastructure initiatives and new construction projects (albeit those concentrated in disaster relief and post-disaster reconstruction), facilitating local economic recovery and fostering growth.

Although the stimulus package is not overwhelming in size, it carries a message. The new bond issuance will push China’s deficit ratio above this year’s target of 3%. The government generally sticks to its target and only surpasses it during times of serious stress (the last time China surpassed its deficit ratio target was in 2020, the year when the COVID-19 pandemic broke out). Thus, the decision to issue debt underscores the central government’s recognition of the gravity of the local governments’ debt issues and the intention of senior leaders to help them address these problems with a more radical approach.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.