Senior officials of the US State Department announced a six-month relief of most sanctions imposed on the Venezuelan oil and gas industry. The decision comes after a breakthrough in the ongoing negotiations between Venezuelan government officials and opposition parties. Under the agreement, President Nicolas Maduro’s administration grants a series of electoral guarantees for the upcoming presidential election, such as setting a date in late 2024 and allowing the presence of international observers. Maduro’s concessions, although limited, are explained by the government’s need to finance its budget and its deep reliance on the energy sector, factors exacerbated by the country’s de facto dollarization and its need for foreign currency. Over two-thirds of the public budget is financed through oil revenue, making the country especially vulnerable to a commodity crisis. Lower-than-expected oil prices in late 2022 and decreased tax revenue strained the government’s fiscal situation coming into 2023. Companies operating in Venezuela will benefit from increased currency flows that will help support private demand. Holders of sovereign debt have also benefited, as Venezuelan bonds have rallied in the past week. Foreign companies looking to resume operations in Venezuela should look for guidance from the US State Department in order to comply with other sanctions imposed on Venezuelan entities. However, the relief should make it easier to do business in Venezuela for foreign suppliers of machinery and other capital expenses of oil operations, as payments will be less restricted. Nonetheless, a transition of power in Venezuela remains a remote possibility, as well as its past positioning as a world leader in oil exports.

Overview

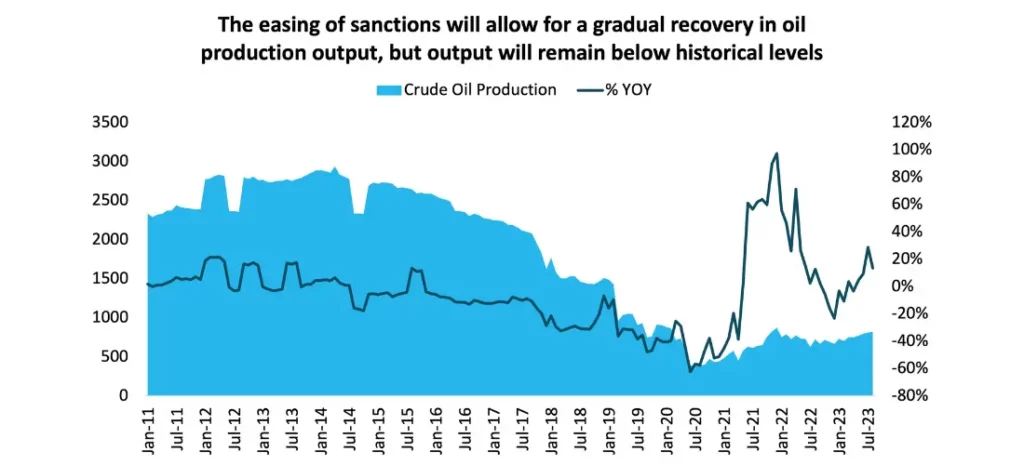

Although Venezuelan exports of oil to the US have risen since January after a complete halt implemented in 2019, the country’s production will remain far from historic highs. The country’s oil output had been on a declining trend even before the imposition of sanctions, as economic mismanagement of PDVSA hindered the company’s operability, currently producing 790,000b/d. The US Energy Information Administration estimates that Venezuelan oil production will rise to 900,000 b/d by the end of 2024, an insignificant change to global oil markets. Nonetheless, most of this output will come from Chevron’s joint ventures, as well as a larger trend of redirecting Venezuelan exports. Under the sanctions, Venezuela was forced to sell most of its crude to China at a significant discount due to transportation costs. The relief package will not only allow the country to expand its capabilities, but it will also significantly raise profits by redirecting its output to the Gulf of Mexico. The move will also benefit PDVSA’s creditors, as it will be able to pay back its debt through crude exchanges, as it has been doing with its Russian and Chinese counterparts. The country would need significant long-term investment to greatly expand its current oil production, a highly uncertain prospect, as investor confidence will remain historically low for as long as Maduro remains in power.

Our View

Although the relief will have a limited effect on global oil prices, the domestic impact will be widespread. The redirection of oil exports and the expanded production will provide much needed funding to the Venezuelan government and benefit supply chains surrounding the energy sector, and the foreign currency entrance should support private demand. The significantly more favorable context should make the central bank’s job of reining in inflation easier, as it will not be under pressure to finance the deficit through monetary expansion. It should also enhance the government’s capability to cut back spending without pushing the country into a depression. Nonetheless, as the easing of sanctions is currently a temporary effort, it will fail to spur any long-term investment, the kind needed to greatly enhance Venezuela’s export capabilities and achieve sustainable growth. The migrant crisis at the US border, a highly contentious issue in the US presidential election, underscores the need by US President Joe Biden’s administration to stabilize the Venezuelan economy through a soft-hand approach. Under this context, Maduro is in an especially favorable position to engage in negotiations to concede just enough to save face while securing his place in power, all while greatly expanding the country’s oil income. As such, our base case is that Nicolas Maduro will remain in power for the foreseeable future. The prospects for the Venezuelan economy will most likely include a few years of growth spurred by oil revenue, with GDP well below the levels experienced before the economic collapse endured this past decade.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.