Multinationals operating in Colombia are unlikely to feel any immediate impact from the reform in 2024; however, it may become a focal point in legislative debates during H2 2024 and early 2025.

A revised tax reform favoring corporations could stimulate both domestic and foreign investment in Colombia, but a substantial hike in individual income taxes could dampen investment in more liquid assets. If the government’s core reforms are ratified, the forthcoming tax reform could potentially disregard or significantly alter any proposed reductions in corporate taxes. This alignment would be necessary to meet the new tax collection requirements aimed at funding the additional spending necessitated by the implementation of one or more of these reforms. Furthermore, in this instance, any gains achieved through a more business-friendly tax reform could be offset by a highly restrictive labor reform.

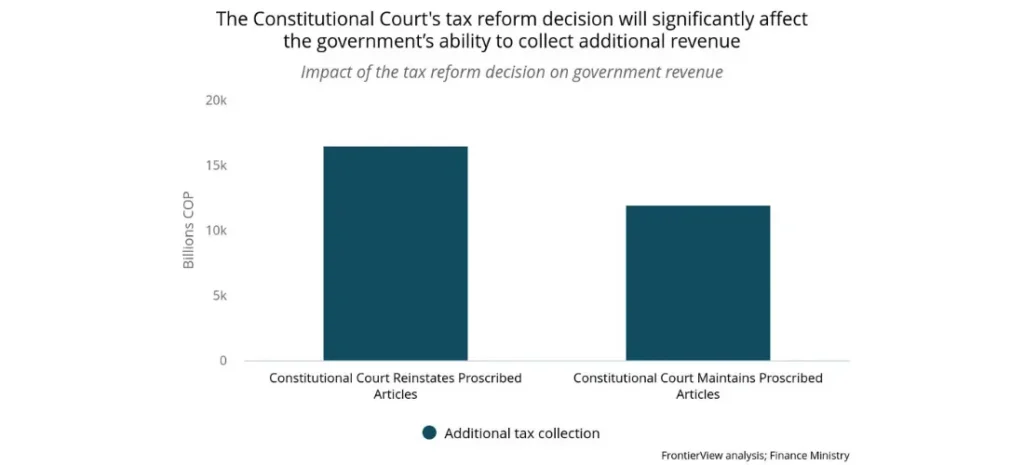

Although unlikely, if the Constitutional Court overturns its decision to invalidate specific articles of the 2022 tax reform, foreign direct investment (FDI) and domestic investment may continue to be restrained, given the heightened cost of capital. However, the government’s urgency to implement a new reform would notably diminish.

Overview

A new tax reform is on the horizon in Colombia. The new tax reform aims to reduce the corporate tax rate from 35% to 30%. However, it also seeks to impose stricter fiscal control not only on corporations but also on their shareholders, who will be subject to heightened scrutiny to prevent tax avoidance.

- While Finance Minister Ricardo Bonilla has asserted that this proposed tax reform will be fiscally neutral, our view is that it will likely lead to tax increases. Not only has the Constitutional Court declared several articles of the last tax reform unconstitutional, restricting the government’s ability to collect taxes, but also, President Gustavo Petro’s ambitious spending agenda will require an increase in total collection.

- Following a series of decisions by the Constitutional Court, the government estimates that its tax collection could decrease by over USD 750 million. Colombia’s Constitutional Court declared an article of the 2022 tax reform that prohibited oil and mining companies from deducting royalties paid to the state from their income tax as unenforceable. Additionally, the Court also declared the 20–35% increase in the corporate tax for free zones from 20% to 35% unconstitutional. The government has decided to appeal the decision of the Constitutional Court, which has agreed to revise its ruling.

- While there is potential for a reduction in corporate taxes, there is a significant likelihood of substantial increases in taxes for high-income individuals.

- Nevertheless, the tax burden on high-income Colombians is already considerable. Therefore, an increase in tax rates on middle-income households will likely be considered as well.

- The government has opted to postpone the tax reform until Congress approves the labor, health, and pension reforms.

Our View

As the Constitutional Court has constrained the scope of the latest tax reform, the Petro government will need to pursue a new reform to advance its ambitious spending agenda while adhering to the fiscal debt limits mandated by the country’s fiscal rule. Although the government has asserted that the new tax reform will maintain fiscal neutrality, we believe this is unlikely. The government’s tax collection capabilities do not align with its fiscal spending objectives. Given the government’s commitment to reducing the fiscal deficit while bolstering social spending, additional tax revenue will likely be necessary for 2025.

The government’s prioritization of other reforms suggests confidence in its ability to navigate these changes through Congress. However, with the growing presence of the opposition and independent legislators, the likelihood of reforms being approved diminishes. If one or more core reforms are enacted, the tax reform will likely need to become more fiscally expansive to accommodate additional expenses imposed by these reforms.

Finally, the potential approval of the tax reform, as initially proposed by the government, could lead to a decrease in corporate tax rates, potentially invigorating private sector investment. Yet, the stringent tax collection measures on individual income may present significant challenges to liquidity within Colombia’s portfolio markets.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.