Government spending priorities in 2024 have been significantly altered by the war in Gaza

B2G firms should continue to expect limited opportunities in infrastructure development and housing in 2024. Prepare for uncertainty and heightened risk of muted demand as a higher-than-expected deficit leads to significant spending cuts at most line ministries. Firms should also anticipate strong pressure for an overall retrenchment in government spending in 2025 and thereafter due to the large increase in Israel’s fiscal deficit this year. Meanwhile, B2C firms should not expect a strong positive impact on consumption from the revised budget. Prepare for continued price sensitivity among Israeli consumers in 2024, with confidence likely to recover only slowly due to war impacts.

Overview

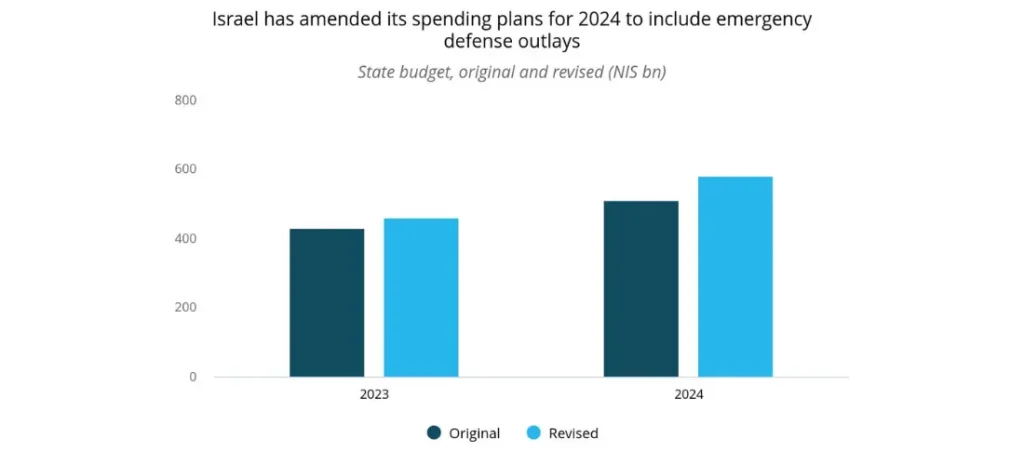

- Israel’s cabinet approved an amended state budget for 2024 in January. The original plan had been passed by the Knesset in March 2023. Total spending under the revised plan will increase by 13.6% (NIS 70 billion) to NIS 582 billion.

- About 80% of the spending increase has been earmarked for additional defense expenditures and war damage compensation programs.

- Although higher allocations have been made for a handful of civilian ministries including healthcare and education, across-the-board cuts of 5% have been implemented at most line ministries. As a result, overall base spending has been reduced by about NIS 20 billion compared to the original 2024 plan. This locks in headcount reductions at most ministries over the course of 2024 and 2025.

- Although VAT has not been increased in the revised budget, the government has indicated it will raise the VAT rate from 17% to 18% in 2025. It has also raised tax rates on tobacco products for 2024 and is increasing the tax on bank profits from 17% in 2023 to 26% in 2024–2025.

- Israel’s Ministry of Finance now expects the fiscal deficit to reach 6.6% of GDP by the end of 2024, up sharply from just 0.9% prior to the outbreak of the Gaza War.

Our View

Israel’s outlook for public investment is largely unchanged, with most public works projects set to proceed according to schedule, although CAPEX plans for 2024 were relatively weak to begin with. Public investment in transport infrastructure and roads are still falling sharply from 2022 levels, and an ongoing ban on the entry of 200,000 Palestinian workers will lead to extended completion timelines and possible cost overruns.

FrontierView assesses that the revised 2024 budget will have a neutral or slightly negative effect on consumer spending this year.

Although the government has proposed grants of up to NIS 8,400 per month for reservists on active duty, with an additional NIS 4,500 per month for each child under the age of 14, the maximum base reservist compensation amounts to just 65% of Israel’s average monthly salary of about NIS 13,000. The large number of Israelis expected to be performing reserve duty in 2024 could thus face significant purchasing power pressures during the year.

Additionally, impending redundancies at most government ministries in 2024 and 2025 will negatively affect consumption. The public sector employs about 20% of Israeli workers, or about 870,000 individuals. Headcount reductions of 2–5% in the public sector would negatively impact spending by about 17,400 to 43,500 consumers and their families.

Although the revised budget has increased the healthcare allocation by NIS 1 billion for 2024, the increase has been deployed for an increase in mental health service coverage, meaning additional growth in salaries as opposed to procurement or CAPEX expenditures.

Meanwhile, the sharp increase in Israel’s tax on bank profits could moderate the effect of expected interest rate cuts by the Bank of Israel (BOI) in 2024. Lending standards at banks could remain tighter than they would otherwise have been in a year of expected monetary easing, keeping financial pressure on some firms and households. The large fiscal deficit expected for 2024 means the BOI will take a more conservative approach to monetary easing than would have been the case otherwise.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.