Egypt’s central bank seeks to eliminate the gap between official and parallel exchange rates for the EGP by floating the currency and raising interest rates to unprecedented levels

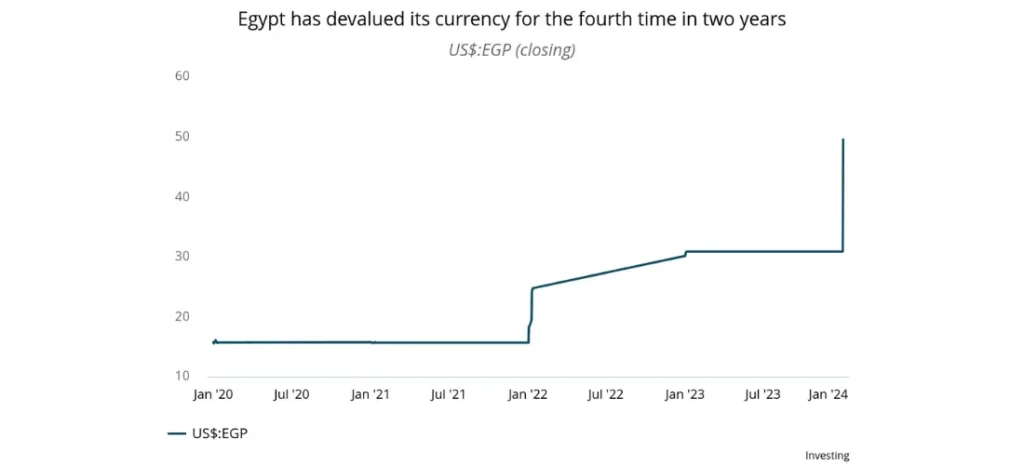

On the morning of March 6, the Central Bank of Egypt (CBE) announced that it would allow the exchange rate of the EGP to be determined by market forces. By day’s end, official exchange rates at Egypt’s banks had settled at about 50/US$. This marks a depreciation of approximately 62% from the 30.9/US$ at which the currency had been officially held over the previous 12 months.

The move effectively eliminated the gap between Egypt’s official exchange rate and rates on the parallel market, which had widened sharply over recent months as markets quickly lost faith that official rates were reflective of the pound’s fair value. Banks have been instructed by the regulator to provide trade credits at an EGP exchange rate of 52/US$. Egypt’s government has also announced that it has reached an agreement with the IMF to upsize its existing support package with the fund from US$ 3 billion to US$ 8 billion. Meanwhile, the CBE has pushed through its largest-ever one-time rate hike, raising lending rates by 600 basis points to 28.25%.

Business Implications:

- In the near term, multinationals should monitor Egypt’s parallel exchange rate market to assess whether authorities have successfully managed to unify exchange rates across the economy. The continued existence of a parallel market will pose a significant challenge to any normalization of operational conditions in the Egyptian market.

- For the 12- to 18-month horizon, firms should utilize scenario planning to prepare for a range of outcomes regarding the path of the EGP exchange rate and the resultant level of inflationary pressures. Firms should also closely monitor the degree of compliance by Egypt’s government with its commitments to the IMF and other partners regarding monetary and fiscal policy rationalization. Backsliding in this regard significantly increases the risk of a return to cycles of FX scarcity and sharp depreciations.

Drivers:

- Egypt is seeking to stabilize the EGP exchange rate after parallel rates spiked in recent months, briefly surpassing the 70/US$ in January 2024 before falling back toward 50/US$ prior to the devaluation. With FX inflows dwindling, importers had been directed to provide cash cover for trade financing, helping drive demand for FX to the parallel market over the past year.

- Egypt’s FX crunch resulted in a large backlog of merchandise building up at the country’s ports, while receivables to foreign suppliers and international oil companies built up, and multinationals have faced difficulties in repatriating profits from Egyptian operations, deterring foreign investment into the country. Meanwhile, Egypt’s government faces a large debt repayment burden in 2024, with about US$ 22.4 billion payable on bonds and loans.

- Egypt’s receipt in March of the first US$ 10 billion tranche of funds from an Abu Dhabi investment package will have bolstered the CBE’s reserves and given it the confidence to devalue the EGP toward a rate more in line with the parallel market while retaining the ability to head off an overshoot of the exchange rate.

- Bailout conditions from the IMF have stringently emphasized the need for a flexible exchange rate that prices the EGP fairly, to avoid depletion of Egypt’s foreign reserves. Egypt’s dependence on imports for strategic commodities such as food had made the issue of exchange rate flexibility a significant sticking point in negotiations with the IMF and led to long delays in reaching an agreement.

Looking Ahead:

- FrontierView expects the CBE’s move to practically eliminate the parallel exchange market by Q2 2024. We are anticipating a largely stable exchange rate through the remainder of the year, albeit with moderate downward pressure on the pound as suppressed demand for imports revives. Pressure on homegrown FX sources, such as Suez Canal revenues and natural gas exports, further contributes to our expectation of moderate downward pressure over the immediate term.

- We expect the EGP to close 2024 at a rate of about 52–54/US$, with access to FX through the banks gradually improving as firms and high-income households de-dollarize, flows are rechanneled from the parallel market toward the banking system, and foreign investment picks up.

- FrontierView anticipates significant progress on major state asset sales to GCC investors by Q3 2024, with a significant likelihood of major new FDI inflows or support packages from GCC partners. Depreciation of the EGP toward fair value clears a significant obstacle to investor confidence in the Egyptian market.

Inflation Outlook: FrontierView continues to expect Egypt’s inflation rate will remain very high in 2024, with a base-case range of 24.8–29.3% for the year, compared to 33.8% for 2023. Residual supply disruptions will continue to put pressure on firms to pass rising costs onto consumers, resulting in high inflation. Meanwhile, the sharp depreciation in the EGP will yield higher import costs, due both to pricing pressures and to customs and VAT rates being assessed using the new exchange rate.

Consumption Outlook: The latest devaluation marks the fourth time in two years that the EGP has been devalued and will help keep strong pressure on purchasing power for most Egyptian households, mainly by contributing to very heightened inflation in the market. FrontierView forecasts weak consumption growth of about 2.8% in 2024—slightly higher than in 2023 but still marking a per capita growth rate in the range of just 1.0%. Spending on imported durables and big-ticket items may recover markedly in H2 2024 as improved FX availability allows distributors to restock at new price points.

Investment Outlook: Private business activity will remain depressed overall in 2024. Many of the negative themes in place during 2023 will carry over through 2024, including sharp cost inflation, including for labor and raw materials. Businesses will be faced with sharply higher financing costs following the CBE’s sharp interest rate increase. As of March 2024, lending rates were 11 percentage points above their level one year previously. This will constrain firms’ scope to borrow for CAPEX purposes. Additionally, subsidized interest rates for firms operating in certain sectors are being phased out as part of an IMF-sanctioned reform program. Meanwhile, the government is likely to raise prices for goods and services provided by public entities, including utilities and energy, putting further pressure on business costs.

Public Spending Outlook: Egypt’s government is likely to significantly constrain public investment expenditure in the FY 2024/2025 budget. PM Mostafa Madbouly has stated that the government will cap total public investments at EGP 1.0 trillion, a decrease in real terms from the figure announced for FY 2023/2024. The sharp increase in interest rates significantly increases Egypt’s domestic debt repayment burden. FrontierView expects the government to continue prioritizing OPEX items such as public sector salaries and social support measures in light of the inflationary environment. We anticipate significantly extended project timelines as well as price reduction pressures through 2025.

Operational Outlook: Banks should be able to freely meet FX demand by Q2 2024, by which time multinationals should find it easier to repatriate profits from Egypt operations. Cash cover requirements should also be removed by H2 2024, with importers no longer requiring parallel providers to source FX. However, multinationals’ improvement in access to FX through the banks will be gradual. Additionally, while Egypt is likely to make significant progress in reducing its import backlog, priority will likely be given to strategic items such as food and medicine through Q3 2024. Egypt’s government will also leverage increased FX availability to meet its arrears to international suppliers and contractors, although priority here will be given to international oil companies.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.