GDP growth fell short of market expectations, indicating a slower-than-anticipated economic recovery

Businesses operating in Colombia should anticipate a sluggish recovery for the country’s economy in 2024, albeit with a slightly improved consumption outlook. Persistent political uncertainty and elevated capital costs are likely to restrain investment throughout the year.

Overview

Colombia’s GDP growth fell short of market expectations, registering 0.6% growth. Although the country avoided a technical recession, discounting public spending, the economy endured three consecutive quarters of negative growth during the year of -1%, -1.5%, and -0.3% YOY.

Despite the country’s ability to avoid negative growth, the economy has been significantly weakened due to high lending costs, subdued consumption resulting from persistent inflation, declining investment prompted by political uncertainty, and poor budget execution, particularly evident in public works investment.

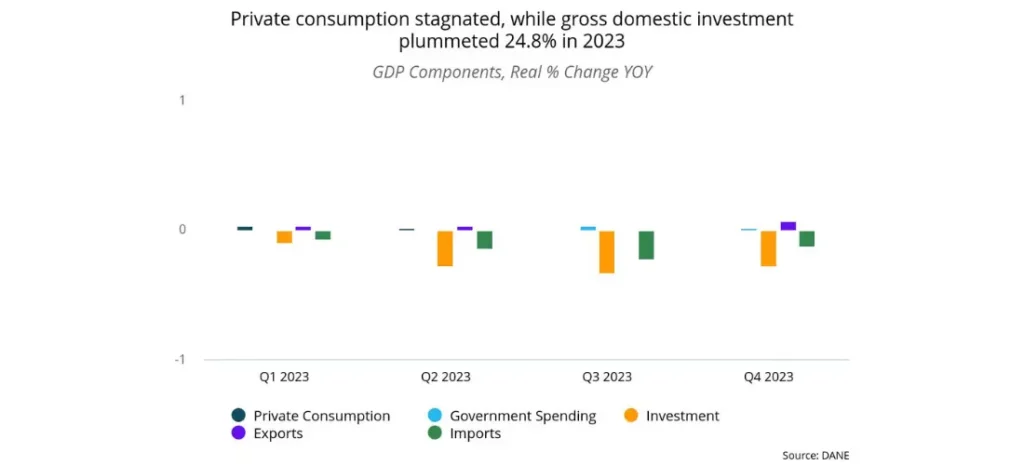

- In 2023, consumer spending maintained positive growth, albeit stagnant since Q1 of 2023, with a YOY increase of 1.1%. Notable increases in consumption were observed in categories such as alcoholic beverages and tobacco products (5.2% YOY), health (5.0% YOY), and recreation and culture (3.0% YOY). Conversely, certain categories experienced declines, including clothing and footwear (-4.3% YOY), furniture and home goods (-3.1% YOY), restaurants and hotels (-3.7% YOY), and transportation (-0.1% YOY).

- Although the government increased public spending in the last two quarters, annual growth only reached 0.9% YOY.

- Gross domestic investment experienced the most significant decline, plummeting by over 24.8% in 2023. This category bore the brunt of the economic challenges throughout the year.

- Gross fixed capital formation declined 9.4% YOY, with investment in machinery and equipment decreasing 16.2% YOY, non-residential building and other constructions shrinking 4.9% YOY, and housing investment falling 1.6% YOY during 2023.

- Exports demonstrated a positive trajectory, experiencing a 3.1% growth in 2023. However, upon closer examination of Colombia’s exports in USD at Free On Board (FOB) prices, they registered a significant decline of 12.9% YOY. This downturn was marked by a 12.8% YOY reduction in agricultural goods exports, an 18.6% YOY slump in commodities, a 3.8% YOY downturn in manufactured goods, and a 14.3% YOY increase in other exports.

- Imports decreased 7% YOY during 2023, with significant declines observed across various categories, including agriculture, livestock, hunting, and forestry (-15% YOY), industrial processed food products (-15% YOY), and textiles (-31% YOY). By contrast, notable growth was recorded in the mining sector imports (127% YOY). Additionally, some sectors experienced marginal changes or remained relatively stable, such as pharmaceutical goods (0% YOY).

- Inflation for 2023 concluded at 9.28%, after a steady nine-month decline. With this consistent downward trend in inflation, Colombia’s central bank has commenced interest rate cuts, culminating in a benchmark policy rate of 13% by December.

- After hitting a record low of 9.38% in April, unemployment began to rise, reaching a rate of 10.8% by the end of 2023.

Our View

Given the subdued GDP growth figure, we anticipate Colombia’s economic performance in 2024, while an improvement over the previous year, to remain relatively lackluster with a modest 1.1% YOY growth projection. We foresee a marginal uptick in consumption, expanding by 1.7% YOY, with government spending surpassing 1.5% YOY. Meanwhile, exports are poised to continue their upward trajectory at a rate of 3.2% YOY. However, gross domestic investment is expected to see only a slight increase of 0.5% YOY, attributed to persistently high capital costs and political uncertainty, particularly impacting public infrastructure projects and subsidized housing construction initiatives.

The alleviation of inflation, coupled with monetary easing from the central bank, is expected to have a favorable effect on both consumption and investment. However, it’s important to note that changes in monetary policy typically exhibit a lag of 6 to 18 months before manifesting in the broader economy. Therefore, while we anticipate positive developments, the full extent of these improvements may become more evident in 2025.

Still, risks remain on the horizon. Recent political developments pose a potential threat to growth, particularly concerning the risk of escalating public spending leading to non-compliance with Colombia’s Fiscal Rule. This could have adverse effects on public finances, elevating the country’s risk profile and consequently raising borrowing costs. Additionally, a recent draft decree aimed at granting President Gustavo Petro authority to allocate national resources across entities and ministries could severely undermine infrastructure investment in the country by centralizing control over investment projects and future appropriations.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.