While Latin America’s macroeconomic environment is expected to remain broadly stable in 2024, the region faces several key political, fiscal, and climate risks

As we enter 2024, Latin America faces a wide span of potential risks that could upend our expectations for the next 12 months. While these risks are not part of our base case, multinationals operating in the region should take note of potential disruptions that could emerge throughout the year and factor them into their scenario planning processes. Here are the most important potential events to monitor in Latin America (beyond those mentioned in our global report):

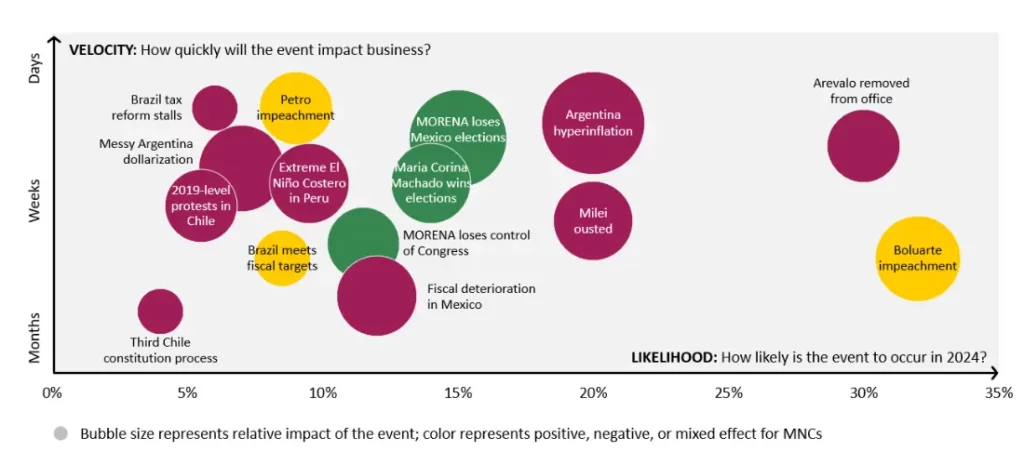

Argentina:

- Argentina enters hyperinflation: Our base case scenario assumes higher inflation pressures in the first semester of 2024 due to the implementation of policies to correct the current macroeconomic imbalances. Particularly, given the expected devaluation, we foresee monthly inflation ranging from 10% to 13% in Q1 2024. However, Argentina’s inflation trend is clearly unsustainable, and we cannot dismiss a hyperinflation process as part of our downside scenario. Generally, this process is defined as price increases above 50% per month. The last time Argentina experienced a similar process was in 1989, after high political turmoil and debt default fears. The main drivers of a new hyperinflation process could include the implementation of unclear fiscal policies and a disorderly dollarization program.

- Argentina implements a messy dollarization program: Javier Milei’s recent announcements, coupled with Emilio Ocampo’s rejection to become the president of the central bank (Ocampo being a former investment banker and an expert on dollarization), signal that the dollarization program will be postponed at least until the end of 2024. Therefore, our base-case scenario assumes the new government will focus primarily on reducing the fiscal deficit and increasing the net reserves of the central bank. Nevertheless, in our downside scenario, the risk of a messy dollarization remains relatively high, as this monetary system was the main campaign promise of Milei. A disorderly dollarization implementation and lack of foreign exchange reserves will imply significant upward pressures on the foreign exchange market, leading to a bank run and a major financial crisis.

- A fragile Milei government ends abruptly: Given Milei’s lack of legislative power to secure an absolute majority for his agenda, the Libertarian Party must adopt a consensus-building approach to advance its policies. We expect the party to secure an alliance with the more right-wing factions (PRO) of Juntos por el Cambio and to negotiate with provincial deputies and senators. Our downside scenario envisions an abrupt end to Milei’s government due to ineffective management of the high political and social costs associated with correcting the current macroeconomic imbalances. According to the constitution, an impeachment must be approved by two-thirds of both chambers, which could be achieved with the votes of the leftist parties, the Peronist bloc, the centrist faction of Juntos por el Cambio, and the collapse of the alliance with the PRO.

Brazil:

- Brazil is able to work within its 2024 fiscal targets: Given the current trajectory of government spending and revenue collection, our base case assumes that Brazil will perform more negatively than the fiscal targets previously approved in Q2 2023. Hoping to avoid incurring the penalties associated with non-compliance with the fiscal targets, our base case also assumes that Brazil’s Congress will seek to amend the primary deficit targets at some point in H1 2024 to avoid lifting government spending rates in 2025. However, Congress is currently discussing several proposals that aim to increase revenue collection—mostly through one-off measures. While it remains uncertain Brazil will be able to make up all the shortfall, our upside scenario assumes that Brazil will be able to approve all revenue-increasing measures and zero the primary deficit; however, this scenario also assumes lower budget execution to ensure fiscal commitment, potentially limiting the use of pork barreling funds, which could jeopardize agenda setting.

- Brazil is unable to approve a tax reform: Our base case assumes that in H1 2024, Brazil will be able to approve a watered-down income tax reform—one that increases levies on high-income earners but does not create a tax on dividends. However, our downside scenario foresees the subsequent phases of the tax reform and fiscal anchor take a turn for the worse on the back of lower popular and, subsequently, political support. Limited political support prevents the approval of an income tax reform. Unable to pass an income tax reform poised to increase tax collection, the credibility of the newly approved fiscal anchor is called into question, denting the confidence of market participants in Brazil’s fiscal commitment.

Chile:

- 2019-level protests emerge in Chile: Chile’s economy has begun to recover, propelled by increased consumer spending mainly due to diminishing inflationary pressures. Furthermore, the beginning of new mining projects and reduced supply disruptions are poised to boost export performance in 2024. We expect this dynamism to strengthen the labor market in 2024, leading to a reduction in unemployment rates, which are currently substantially higher than pre-pandemic figures. However, our downside scenario acknowledges that the labor market’s recovery may be protracted. Consequently, a less robust recovery, coupled with public discontent with the political system and the support of left-wing groups, who have lost confidence in the current government, could incite widespread protests akin to those in 2019.

- Chile’s government pursues a third constitutional process in 2024: The government’s spokesperson, Camila Vallejo, recently announced that the current administration does not intend to initiate a third constitutional process. Instead, the Boric administration’s immediate goal is to gain approval for a fiscal pact in 2024. This pact is expected to increase government spending in key areas such as pensions, security, and healthcare. Since these policy areas can be advanced without enacting a new constitution, a third constitutional process is not anticipated. However, despite its low probability, a third process could emerge due to a constitutional rejection in December, followed by escalating social unrest.

Colombia:

- Gustavo Petro is impeached: While our base-case scenario is that President Petro will remain in power during 2024, the constant scandals surrounding him could lead to impeachment, which would be more likely if they uncover more links to illegal financing in his campaign. Although Petro is not pro-business, his impeachment would have to be preceded by a series of crises that would most likely negatively impact business sentiment and the overall functioning of the public sector. Furthermore, due to Colombia’s institutional characteristics, this would be a process marked by significant friction between the executive and other branches of government. On the other hand, his impeachment would imply the non-approval of disruptive reforms, which could be positive for the country and the private sector.

Mexico:

- MORENA loses the 2024 presidential election: Based on the most recent poll results, Claudia Sheinbaum, MORENA’s presidential frontrunner, is well positioned to win the 2024 election. Sheinbaum currently holds a comfortable lead, garnering 48% of voter preference, compared to 24% for Xochitl Gálvez, the candidate from the opposition bloc, Frente Amplio. While an opposition victory is considered unlikely, Gálvez could potentially close the gap and emerge as a more competitive contender. A Gálvez presidency would mark a significant departure from AMLO’s policies, emphasizing greater private sector involvement and a transition to green energy. However, the extent of Gálvez’s policy agenda would depend on the outcome of the congressional elections and the resulting legislative layout.

- Mexico experiences significant fiscal deterioration: Concerns mount over Mexico’s potential loss of investment-grade rating following the approval of the 2024 federal budget. The budget has raised alarm bells due to its high fiscal deficit of 5.4%, the highest since 1988. Our base case assumes that a sovereign credit rating downgrade is unlikely, as Mexico maintains a low level of indebtedness compared to other similar countries thanks to its record of fiscal prudence. However, risks to the country’s pro-investor image persist. The budget’s focus on tax cuts for Pemex and high social spending dims Mexico’s fiscal outlook. Heightened fiscal risks could trigger capital flight, undermining the growth capacity of key sectors such as manufacturing and financial services.

- MORENA loses control of Congress: Given AMLO’s high approval rating and MORENA’s popularity in key states of the country, our base case assumes that the ruling party will keep its control over both houses of Congress. Currently, MORENA’s coalition (Juntos Hacemos Historia) holds 274 of the 500 seats in the Chamber of Deputies and 74 of the 128 seats in the Senate. If it manages to maintain a simple majority, a potential President Sheinbaum would have the green light to approve her policies without any trouble. However, the opposition bloc (Frente Amplio) might recover lost ground in the northern and central states and thus put an end to MORENA’s dominance. In this way, the opposition would be able to halt some of the most radical policies of the so-called Fourth Transformation (4T) agenda.

Peru:

- Extreme El Niño Costero climate event ensues in Peru: According to the Geophysical Institute of Peru, there is a 5% chance of no occurrence of a Niño Costero, a 17% chance of a weak event, a 38% chance of a moderate event, a 39% chance of a strong event, and a 1% chance of an extreme event. Our base-case scenario anticipates notable supply disruptions due to a moderate-to-strong Niño Costero, leading to higher food and beverage prices in the first half of 2024, along with a slowdown in GDP growth and consumer spending. While an extreme event is highly unlikely, the probability of a strong-to-extreme event has been increasing since November, signaling potentially greater adverse impacts on the agricultural, fishing, and retail sectors.

- President Dina Boluarte is removed from office: Despite significantly low levels of approval, President Boluarte has managed to remain in office by empowering traditional parties in Congress and maintaining a moderate policy agenda. Nevertheless, our downside scenario considers that the current economic crisis and a major corruption scandal could reignite protests and force Boluarte’s resignation. The impeachment would force Alejandro Soto, head of Congress, to assume leadership of Peru’s government. Worsened social and political tensions would then likely lead to a weak economic recovery, stemming from reduced private consumption and investment.

Guatemala:

- President-elect Arevalo is removed from office: Our base case assumes that Bernardo Arevalo will be sworn in as president of Guatemala on January 14, 2024, and will be able to remain in office throughout the year. Nonetheless, Arevalo is in the crosshairs of several prosecutors from the public ministry, who have taken legal action to suspend his political party (SEMILLA) and revoke his immunity. Our downside scenario foresees Arevalo’s removal from office under pressure from the right-wing dominated Congress. This would lead to strong social unrest that would translate into widespread protests, thus disrupting economic activity and weakening the country’s already-fragile rule of law.

Venezuela:

- Venezuela’s Maria Corina Machado wins the 2024 presidential election: A peaceful transition of power remains a distant prospect in Venezuela. Nonetheless, if Machado manages to win the election and assume office, it would have an outsized effect on investor confidence and democratic values. Furthermore, an extended relief from sanctions would allow for a gradual recovery of the country’s extractive industry. Although the country will hardly reach the heights of its 3,000,000 bpd, even in the long term, the sector’s recovery requires the kind of long-term investment that would be almost impossible to achieve if President Nicolas Maduro remains in power. Market consensus is that Venezuela will reach the 1,000,000 bpd milestone by the end of 2024, a recovery that will undoubtedly pick up if the opposition is elected. The country’s sovereign debt bonds have already experienced a rally on the news of sanctions relief, from 10 cents to 20 cents on the dollar, a trend that will surely pick up if a peaceful transition of power is achieved. A debt restructuring deal under Machado could possibly mean access to foreign capital markets after Venezuela defaulted on its obligations in 2017. This would ensure a recovery of investment, and it would probably ease the government’s need to finance its budget through monetary expansion, taming inflation in the process. Altogether these factors could probably push Venezuela toward a strong growth trajectory in the upcoming years, although the magnitude of the collapse of the Venezuelan economy under Maduro (output shrank three-quarters) means that pre-crisis per-capita GDP levels remain a long-term prospect that would need a further strengthening of all the other democratic institutions in the country.

Watch a video overview of the LATAM Events to Watch for 2024

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.