MENA remains a source of growth for multinationals, but regional risks could thwart its large potential for 2024

In 2024, the MENA region faces a large number of risks on the political, security, social, and economic sides that could spell a notable disruption for growth projections. While these risks are not a part of FrontierView’s base case, they continue to necessitate a significant focus on medium- to long-term scenario planning. The fact that much of these risks are driven by external or political factors complicates the manner in which we can effectively respond and contain their impact on our business. Nonetheless, multinationals ought to take note of such risk-episodes and plan against them for both, their regional and global portfolio performance. Here are the most important potential events to monitor in MENA (beyond those mentioned in our global report):

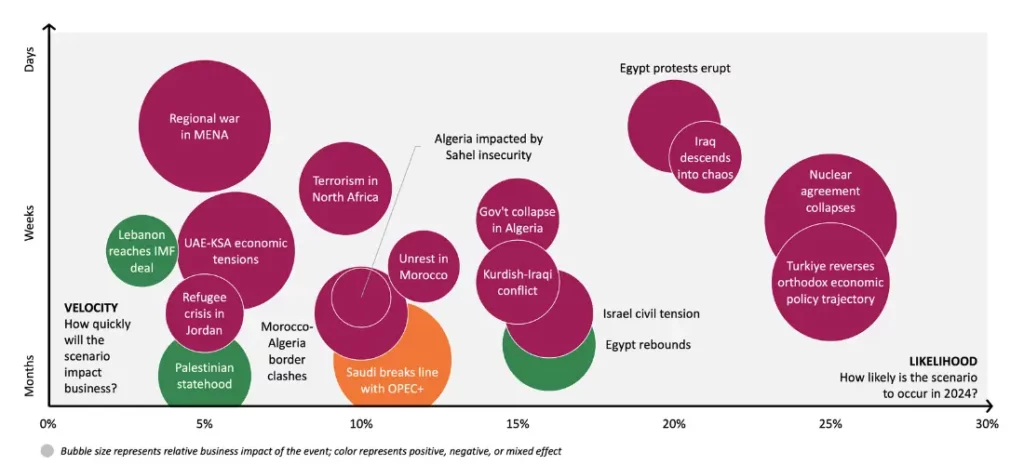

- Algeria’s cost-of-living crisis deepens political discontent and triggers mass protests and government collapse (15%): Fiscal pressures result in further adverse import restrictions and reduced state ability to provide further household support. This triggers cost-of-living protests and raises public criticism of the government. Approval ratings have been low since President Abdelmadjid Tebboune took office and were exacerbated by the government’s handling of the pandemic. Friction between President Tebboune and other Algerian elite figures widens and forces a government collapse. Market disruptions and halted public investments would worsen in 2024.

- A combination of poor harvest in Morocco and high commodity prices triggers mass protests and boycotts of imported brands due to high prices (12%): Adverse weather conditions severely harm crop yields in Morocco, coinciding with high global food commodity prices, which drive up high prices on imported food articles. Morocco’s price sensitivity results in protests against foreign multinationals (seen in the previous decade) and a rapid trend of boycott activities.

- Prospects of a nuclear agreement comprehensively fail (25%): With the increasingly likely prospect of former President Donald Trump winning re-election in the US in 2024, Iran and the US fail to reach any compromise, resulting in complete abandonment of the agreement. Iran works its way into becoming a nuclear power. This triggers a sudden and notable increase in security risk across MENA, impacting US assets in Iraq, international commercial and oil trade in the strait of Hormuz, and further polarization in the Middle East. Iraq sees weakening consumer spending, Lebanon’s political situation exacerbates, and a direct conflict emerges between Iran and Israel.

- Iraq descends into violent chaos (21%): The war on Gaza triggers more pronounced and heavier attacks on US targets across Iraq, resulting in a return of US military presence in Iraq. Clashes erupt between US army personnel and Iraqi militiamen as well as Iraqi army personnel, dragging the country into a state of open conflict. Private consumption grows increasingly depressed and public investments falter.

- Egypt descends into mass protests and violent crackdowns (18%): Severe austerity measures imposed after a heavily criticized President Abdel Fattah al-Sisi win result in mass protests, only to be met with violent crackdowns from the military. Egypt defaults on its debt, and the pound crashes aggressively, depressing purchasing powers. Widespread disruptions to tourism, private consumption, and public investments ensue.

- Israeli occupation recedes, and Palestinian statehood emerges (5%): The war on Gaza reopens serious conversations on the topic of Palestinian statehood. The PA is reinstated in Gaza, the Palestinian border is widened, and both economic reforms and incentives are paid to the state. An international accord, heavily funded by the Arab world, creates a fund to support the rebuilding and enhancements of industrial presence, infrastructure, public institutions, and other strategic areas of investments. Security risks in MENA drop slightly, and Palestinian consumption recovers strongly.

- Israel descends into civil conflict (16%): Heavy criticism of PM Benjamin Netanyahu’s war tactics and the intelligence failure reignites a deep fracture in Israeli society, causing marked polarization. The extremist, right-wing party steps up attacks on the opposing side and their supporters, with clashes turning violent with the presence of live ammunition. Civil conflict erupts, causing mass disruption to political stability, private consumption, and investments.

- Saudi breaks OPEC+ consensus and floods supplies (11%): Oil prices remain low despite significant production cuts. With Saudi Arabia lifting the bulk of the production burden, it decides to reverse its significant production cuts and flood the market with supplies in an attempt to create a price shock large enough to incentivize better future commitments from other OPEC+ members and more aligned compliance from US producers. Oil prices fall below US$ 63/bbl. Saudi revenues are slightly hit in 2024, with some extensive delays in deprioritized PIF projects.

- Lebanon reaches IMF agreement (6%): The severe state of insecurity in the south triggers Lebanese parties to align on a presidential candidate and finally adopt all IMF reforms, including an effective devaluation of the lira as the banking sector absorbs some of the losses. Lebanon receives its IMF bailout and, more importantly, is granted access to the CEDRE fund. Up to US$ 18 billion of investments and grants are approved, putting Lebanon back on track toward economic recovery. Economic stability allows for a recovery in the middle-income segments, allowing for a wider addressable market size and boosting private sector investments.

- Regional war breaks out in MENA (5%): The war on Gaza spills over, roping in Iran, Iraq, and Jordan, and intensifies the activity from Hezbollah and Houthis. Iran and Israel are caught in a direct confrontation, with Iranians aiming at Israeli targets in response to Israeli attacks inside Iranian borders. This results in significant instability across Lebanon, Palestine, Egypt, Israel, Jordan, Iraq, Iran, and Yemen. Security risks rise in the GCC, with FDI and tourism inflows rapidly dwindling. Both oil and commercial supply chains are heavily disrupted, pushing up prices markedly.

- UAE-KSA competition escalates (5%): Despite early wins in the Saudi regional headquarters program, competition between Saudi Arabia and the UAE intensifies. This could take the form of higher tariffs or retaliatory regulatory reforms in the UAE, necessitating considerable capital and human investments in the UAE, or other forms of visa restrictions. A deteriorating relationship between the countries results in a significant cost burden passed onto multinationals, requiring a dual presence in a wide and comprehensive format across the two leading markets in MENA.

- Terrorist attacks in North Africa rise (10%): Political polarization between the region and the West worsens. The humanitarian crisis in Gaza as a result of the Israeli war, combined with further violations of UN laws from the Israelis, triggers a wave of extremist attacks in key tourism hotspots in MENA. As a result, Morocco, Egypt, and Tunisia see a notable drop in tourism activity and private consumption. Increased risk will also trigger a recalibration of fiscal prioritization, with more operating expenditure toward military commitments at the expense of household support and public projects.

- Mass refugee flow into Jordan destabilizes the country (5%): Israeli annexation of Palestinian land, including Gaza or in the West Bank, sees waves of refugee flows into Jordan. The influx worsens economic pressure in the country, with unemployment already above 22% (and 46% among those under age 25). Pressures result in protests and potential civil disobedience, resulting in economic contraction, high inflation, and further depressed private consumption.

- Flaring tensions in Iraq explode into a Kurdish-Iraqi conflict (15%): Ongoing disagreements between the KRG and government in Baghdad worsen, resulting in armed clashes. A civil conflict breaks out in northern Iraq and the Kurdistan Region in Iraq, resulting in severe security risk, widespread attacks, and a rapid reversal of the recovery seen in the country. Private investments are quickly halted, GCC projects are canceled, and the recovering private consumption in the north contracts as a response. Iraq sees economic contraction and disruption in exports.

- Security threats and tensions in the Sahel spill over into southern Algeria (10%): With Algeria taking a more pronounced role in vocalising support or opposition in some Sahel regional tensions, it risks exposing itself to attacks from armed groups. Such attacks extend into its southern gas and oil fields, causing mass disruption to production. Exports and revenues take a hit, and Algeria faces economic contraction accompanied by a reduction in consumer spending and public procurement.

- Morocco–Algeria border clashes flare up (10%): The Western–Sahara and Polisario conflict spirals, triggering a heated confrontation between Rabat and Algiers. Exchange of fire, closure of airspaces, and economic sanctions result in disruptions of European and other FDI inflows into Morocco, along with a drop in tourist arrivals. Furthermore, a reactionary increase in military spending results in deprioritized public spending elsewhere, adversely impacting purchasing powers and public projects.

- Egypt receives large financial support, driving a strong rebound (16%): In a bid to shield Egypt from further spillover of insecurity risks and economic collapse, GCC partners, the EU, WB, IMF, and other international institutions extend generous support to Egypt, allowing it to get back on track with public investments and household support. The newfound economic stability allows for a faster recovery in middle-income growth projections. The Egyptian pound stabilizes at a new rate, private investments in hospitality, energy, and FMCG recover quickly. Public investments in transport and gas improve employment and exports. Austerity measures are no longer necessary, with purchasing powers regaining steam and private consumption growing above 4.6% in 2024. Multinationals are able to drive better regional performance with the re-emergence of opportunities in Egypt.

- Turkiye: Reversal of Orthodox economic policy trajectory (25%): After the May 2023 general elections, President Recep Tayyip Erdogan revamped his economic management team and allowed for a gradual shift toward more orthodox economic policy, simplifying financial regulations, moderating growth, and raising interest rates. However, there is an important risk of a reversal of such policies after the March 2024 elections. If key economic personnel, such as the head of the central bank governor or ministry of finance, are replaced suddenly, if rate cuts begin prematurely, or some of the interventions in the financial system return, alongside a return to unreliable inflation reporting, Turkiye will witness yet another Turkish lira crash. This will further derail the fragile recovery path Turkiye is on.

Watch a video overview of the MENA Events to Watch for 2024

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.