The growth outlook remains subdued ahead of the May 2024 elections

Companies should prepare for muted demand across industries and customer segments that will last until at least the May 2024 elections. Firms must prepare for intensifying competition and persistent price sensitivity among both public and private sector customers. Meanwhile, financial and operational risks will remain elevated amid rand volatility, high interest rates, and worsening power shortages that will raise costs and squeeze margins. Raising marketing spending to capture market share will help firms achieve their commercial goals, as will focusing on resilient industries and customer segments including ICT, financial services, private sector healthcare, and high-income households.

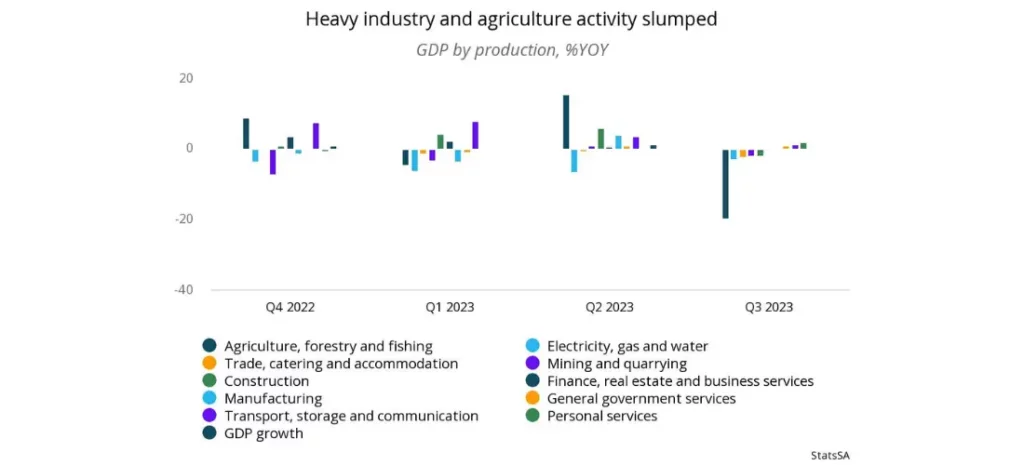

Overview

- GDP contracted by 0.1% YOY in Q3 2023, representing a sharp slowdown from the 1.3% YOY expansion registered in the previous quarter.

- The slump was caused by a 13.2% YOY contraction in gross domestic investment. However, a slowdown was avoided because exports (+2.7% YOY), government spending (+2.6 YOY), and consumer spending (+0.5% YOY) continued to expand.

- Agriculture (-19.9% YOY) posted its sharpest decline since Q4 2003. Most heavy industry continued to contract, including mining (-2.2% YOY), construction (-2% YOY), and utilities (-3.2% YOY), although manufacturing (+0.3% YOY) narrowly avoided a decline.

- Hospitality and wholesale and retail trade (-2.3% YOY) posted its fourth consecutive quarter of contraction, which was also its deepest since Q1 2021. Financial services (-0.1% YOY) posted its first decline since Q1 2021. In contrast, other services grew, including personal services and healthcare (1.9% YOY), transport and storage (+1.2% YOY), and government services (+1% YOY).

Our View

The economy will grow by a meager 0.5% YOY in 2023, avoiding recession only because Q2 growth of 1.3% YOY exceeded expectations. Private sector investment will be stifled by the slump in credit growth that took hold after the South African Reserve Bank raised interest rates to a 14-year high in March 2023. Industrial activity will be curtailed by the worsening electricity crisis, illustrated by Eskom’s electricity output in September 2023 falling below May 2000 levels. The economy will continue to struggle in 2024, growing by just 0.9% YOY. The anticipated modest fall in interest rates and the recovery in tourist arrivals will be largely offset by deteriorating public finances, worsening power shortages, and weaker consumer and investor sentiment ahead of the May 2024 elections.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.