The 2024 growth outlook is contingent on the continued decrease in inflation and the mitigation of negative impacts from adverse climatic events and political risks

Despite disappointing growth in 2023, Peru still offers areas of potential, especially within high-income segments and the primary sectors. Given lower inflation pressures, clients should ensure their supply chains are robust to meet surging demand and prevent stockouts, especially in H2 2024. Moreover, multinationals should contemplate restraining price increases to protect market share, especially in lower- and middle-income demographic segments. Regarding the B2B sector, companies should provide flexible financing solutions to customers in areas impacted by climate conditions, particularly SMEs and those in the northern regions, whose cash flow may be particularly affected by the El Niño climate phenomenon. Finally, multinationals should strengthen relationships with influential and emerging politicians from various parties, given the current government’s instability and high potential for policy changes.

B2C dynamics:

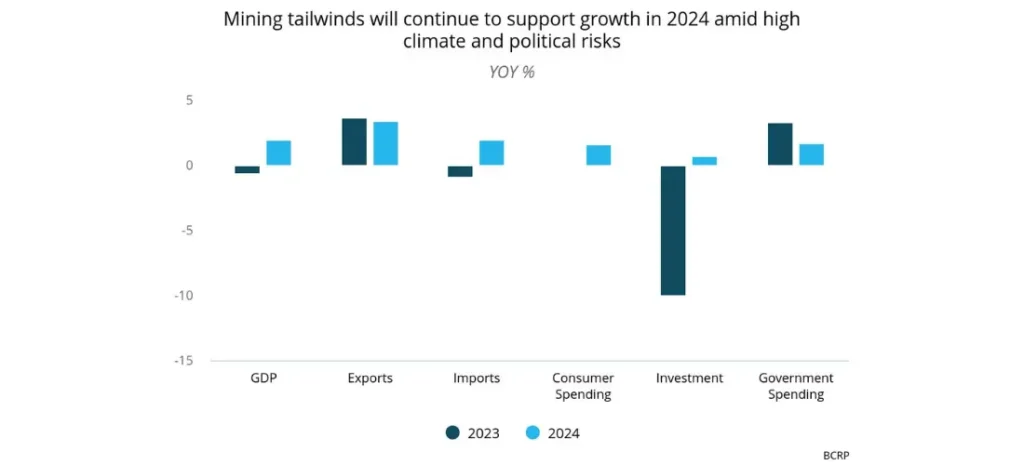

- Consumer spending in 2023 registered (0.1% YOY) its lowest growth rate in 23 years, excluding the pandemic. This significantly weak performance was primarily due to diminishing real wages amid notable inflationary pressures. Despite some upside risks due to adverse climate conditions, annual inflation (3.3%) is clearly under control, approaching the central bank’s inflation target. The decline of real wages, especially for the formal sector, has stalled since Q4 2024.

- Moreover, according to the Monthly Macroeconomic Expectations Survey published by Peru’s central bank, 12-month expectations for the retail sector remain optimistic, and surveyed businesses foresee increased demand and employment in the coming months.

- In 2024, given lower price pressures and borrowing costs, FMCG and durable goods are expected to rebound, while service consumption and high-income consumers will remain resilient.

B2B dynamics:

- In 2023, the considerable contractions in the construction (-7.9% YOY) and non-primary manufacturing sectors (-8.2%) were due to high borrowing costs, low levels of private and public investment, and elevated political instability. Additionally, the adverse climatic effects of Cyclone Yaku and the Niño Costero phenomenon resulted in pronounced declines in the agricultural (-2.9%), fishing (-19.7%), and primary manufacturing (-1.8%) sectors. In contrast, the mining sector increased by 9.5% YOY in 2023, driven by the beginning of the Quellaveco project and better-quality ore in other copper and iron mines.

- Most B2B sectors, notably manufacturing and mining, anticipate a rise in demand by H2 2024, with long-term expectations approaching the optimistic threshold.

- Thus, in 2024, the mining outlook remains positive, given stable external demand and commodity prices, while manufacturing and construction dynamics are expected to improve in the upcoming months, given more favorable financial conditions. However, the agriculture sector will continue to decline due to the Niño Costero, affecting production in the northern regions of Peru.

B2G dynamics:

- In 2023, the country failed to adhere to the fiscal rule, indicating a deteriorating fiscal outlook. The 12-month moving average fiscal deficit reached approximately 2.8% of GDP, exceeding the fiscal rule threshold of -2.4%.

- The persistently high fiscal deficit could lead to credit rating downgrades in the medium term, increasing external credit costs and diminishing investment opportunities.

- In 2024, we expect higher public investment execution rates due to better subnational-level results; however, expenses on goods and services should significantly decline given the fiscal consolidation path.

Our Overall GDP View: After a notably negative 2023, we anticipate a moderate recovery of 2.0% in 2024. Reduced inflation pressures and a relatively robust labor market are expected to boost consumer spending (1.6% YOY). Although the monetary easing cycle implies improved financial costs, we do not anticipate a robust recovery of private investment (0.7%), given elevated political and climate risks. Meanwhile, limited disruptions in the mining sector and consistent copper ore quality will sustain the growth momentum of exports (3.4%). Government spending is projected to register a weak growth of 1.7% due to improved subnational budget execution rates; however, the elevated fiscal deficit will limit the upward trajectory. Finally, while we do not foresee presidential elections in 2024, given President Dina Boluarte’s critical alliances with traditional parties, the government and Congress remain highly unpopular, leaving an elevated risk of further instability.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.