The stimulus fails to provide adequate support to increase demand in the short term

Japan’s upcoming stimulus will not significantly boost discretionary consumer spending. The scale and nature of the policies suggest that households will likely spend the excess funds on essential purchases or add them to their savings. As a result, B2C firms should not account for any major shift in their forecasts due to the stimulus. Similarly, the stimulus is not expected to meaningfully raise wages for Japanese workers in the short term. We expect real wage growth to remain negative in H1 2024, with only gradual improvement in H2 2024.

The domestic production-linked incentives will continue to attract firms in these industries to increase manufacturing in Japan. However, in the short term, these measures will only increase demand for firms in the construction industry. Greater sales opportunities will only materialize for other B2B firms once these production incentives translate into manufacturing activity on the ground.

Overview

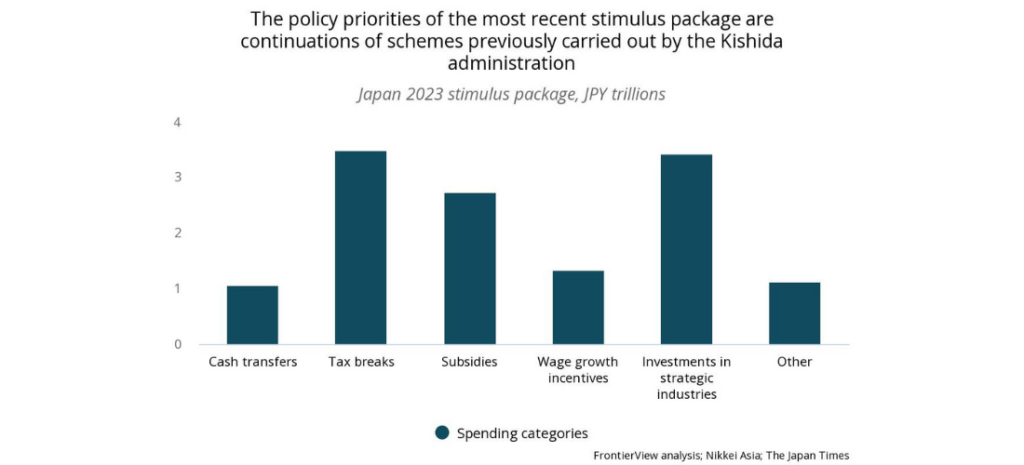

Tokyo is set to release a stimulus package of JPY 13.2 trillion (US$ 87 billion) in the coming weeks. The package is aimed to address the rising cost of living on households and spur consumption growth through tax cuts for all, and direct cash handouts to low-income households. The package closely mirrors the stimulus package passed around this time last year, with cost-of-living support to households and measures to raise wages and incentivize domestic manufacturing in strategic areas. The key features of the stimulus include:

- Tax cuts: Income and resident taxes will be cut by JPY 40,000 (US$ 263.8) per person. However, these tax cuts will only be implemented in June 2024.

- Cash transfers: Low-income households that are exempt from paying taxes will receive direct transfers of JPY 70,000 (US$ 461.6) before the end of the year.

- Subsidies: JPY 2.74 trillion will go toward inflation reduction measures, mainly through the energy subsidies that the government has been funding since the start of the year. These energy subsidies will now be extended until April 2024.

- Wage growth incentives: Tokyo will provide JPY 1.33 trillion to support wage growth in Japan. The funds will be distributed through tax benefits for SMEs that implement wage increases for employees and programs to provide skills training for workers to help them find more lucrative jobs.

- Incentives for strategic industries: The government will increase funding for local manufacturing in strategic industries such as semiconductors and generative AI by JPY 2 trillion.

The stimulus package has currently been approved by the cabinet and is expected to pass the legislature before the end of the current parliamentary session on December 12.

Our View

The upcoming stimulus package is not expected to have a meaningful impact on the growth trajectory of the Japanese economy. The measures put forth are either too small in scale to change consumption behavior or are already under way in some form or another. For example, the cash transfers to low-income households will provide some inflation relief and help them purchase everyday essentials but will not meaningfully raise their discretionary spending. Similarly, the tax breaks are a small, one-off benefit to households, and they will only kick in after six to eight months. Moreover, estimates from the Dai-ichi Life Research Institute indicate that 90% of households have seen their annual costs increase by more than JPY 40,000 due to inflation. As a result, these policies are too small in scope and delivered ineffectively to get the desired effect of boosting consumption.

The other key measures of the stimulus, namely energy subsidies, wage growth incentives, and production incentives for strategic industries, have all been in place for the past several months to varying degrees of success. The energy subsidies have helped lower Japan’s inflation levels since the start of the year. Electricity prices in September were down by nearly 25% from the same time last year. However, these measures have been in place since February and will not raise consumer spending in the short term, as households have gotten used to the lower prices. The wage growth incentives have also been in place for a year but have only had limited success, as most Japanese firms have been unable to raise wages due to the growing cost and profitability pressures that have emerged at the same time. As a result, real wages have been contracting since H2 2022, eroding the purchasing power of most households. The domestic production-linked incentives have been successful in attracting major semiconductor manufacturers like TSMC to Japan, and with more funds available to spend in this area, we are likely to see this trend continue. However, these measures are longer term in nature, as the factories constructed because of these policies will only be operational in 2024–2025 at the earliest.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.