As the tax reform advances in Congress, it further veers from its original intent—with multiple exceptional tax regimes being created

While specific tax burdens will be better defined in 2024, MNCs should expect changes to tax burdens across sectors and closely monitor how the changes will impact their operations and partners. Among the sectors that tend to be most affected by the unification of taxes are services, which will lead to a price increase for consumers. Conversely, the reform will benefit Brazil’s manufacturing and export sectors at first, as it helps address the restrictions on the use of tax credits that burden industrial activity.

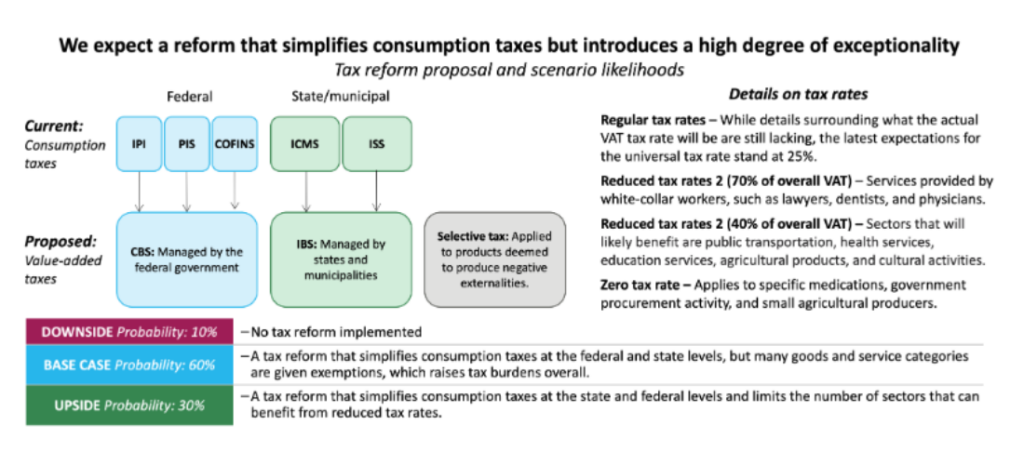

Overview

On November 8, Brazil’s Senate approved Brazil’s tax reform bill in a two-round vote with a 53-24 margin, a key step toward simplifying Brazil’s tax code. Because the Senate implemented changes, the bill must return to the Chamber of Deputies to discuss those changes, where it will require another two-round vote and a 60% majority. Among the Senate’s most notable changes, it increased the number of sectors that will benefit from specialized tax regimes and see lower VAT rates, such as travel agencies, infrastructure concessionaires, sanitation companies, and telecom operators.

Our View

While the approval timeline remains tight, FrontierView still expects the constitutional amendment to be approved before the end of 2023. The tax reform will represent a significant improvement to Brazil’s current tax system, helping reduce litigation in the tax payment system, bringing more clarity to MNCs by standardizing tax regulation across states, and limiting the cost associated with tax compliance in Brazil. At the same time, the reform does have its shortcomings: to gain sufficient political support for approval, the Senate increased the number of sectors that will be incorporated into specific tax regimes. With the creation of new specific tax regimes, the general VAT tax will likely be higher to ensure no revenue collection losses. Companies must also manage a long transition period before the reform is fully implemented, generating tax compliance costs given the need to operate with two parallel regimes for a few years. Additionally, as the reform only provides general rules regarding the changes to the tax system, many key details will still need to be defined in early 2024, including the composition of the food basket that will see tax exemptions, the rules and tax rate of the Selective Tax. As a result, MNCs should expect ongoing lobbying efforts by various sectors to be incorporated into specialized tax regimes, which may limit the benefits for the proposed tax reform simplification.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.