Consumer demand will remain weak in 2024 due to an elevated price environment and weak wage growth

B2C firms should plan for consumer demand in Singapore (especially for durable goods) to remain under pressure over the next 12 months as multiple headwinds weigh on spending. Households will remain highly price sensitive and be more open than usual to trading down, so firms should think carefully before raising prices next year. Companies looking to gain or retain market share should consider utilizing promotions and discounts where suitable. Middle-income households will likely be the most price-sensitive segment, because they are vulnerable to price pressures but are receiving relatively little government support. (Singapore’s leaders are actively channeling support to low-income consumers.) Additionally, spending by high-income consumers will likely remain the most resilient, providing the strongest top-line growth opportunities. However, due to substantial increases in luxury taxes, demand among the lower echelon of this income group may soften to some degree.

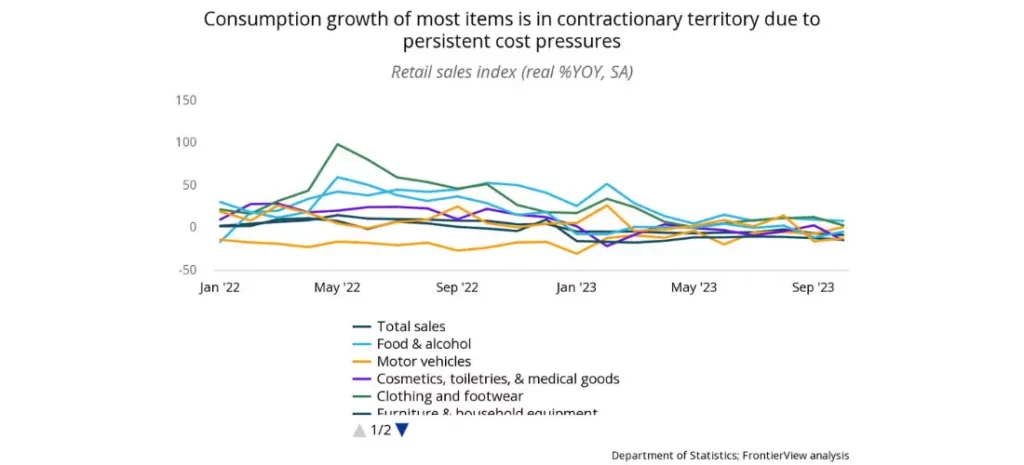

Overview

- On a real seasonally adjusted basis, total retail sales contracted by an average of -6.2% YOY since the start of Q3 2023.

- Spending fell across most items, including motor vehicles, cosmetics, medical goods, furniture, watches, jewelry, and computers.

- Spending on food and alcohol was strong, rising by an average of 8.8% YOY since the start of Q3, primarily due to strong demand for alcoholic products (including those sold in duty-free shops). However, spending on food remained under pressure due to elevated food prices.

- Additionally, services spending in restaurants and fast-food outlets declined by -7.1% YOY and -2.0% YOY respectively in October, due to weak domestic spending and a slow recovery of the tourism sector.

Our View

Despite some subsidy support by the government, retail sales have weakened across most sectors in Singapore due to elevated inflation and weak wage growth. Looking ahead to 2024, although consumption growth will return to positive territory due to base effects, spending will remain under pressure due to multiple factors. Inflation, which has been extremely high over the last two years, will remain elevated in 2024 as well. This is primarily due to elevated fuel and food prices, as well as increases in Singapore’s carbon tax and goods and services tax next year. Credit costs will also remain high next year, as interest rates will only decrease marginally. Concurrently, a softening labor market and weak wage growth will prevent substantial increases in real disposable income. Lastly, while the tourism sector will continue to recover in 2024, it will likely not return to pre-pandemic levels, as Chinese tourists (who previously accounted for roughly 20% of tourists to Singapore) will not visit in the same numbers or spend in the same way as they did pre-COVID.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.