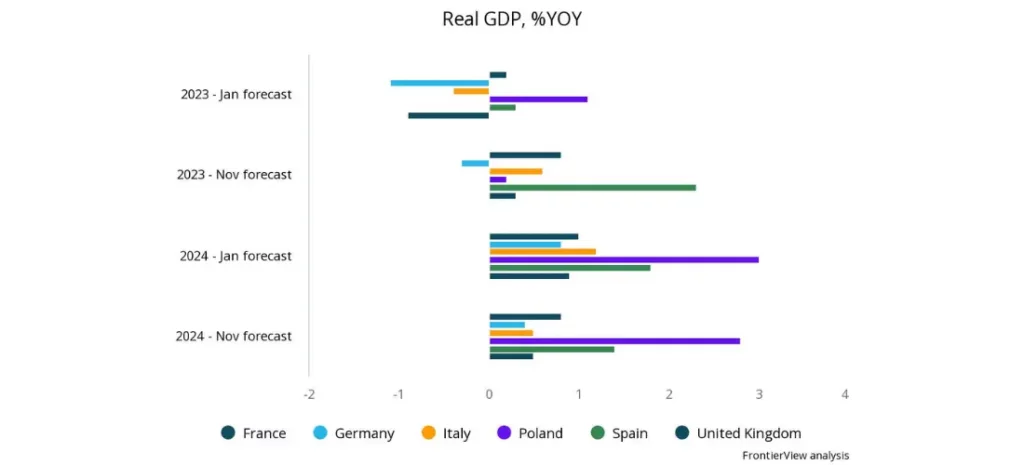

In retrospect, European markets outperformed our start-of-the-year expectations, but long-term prospects remain subdued

While Europe has outperformed in 2023, compared to our initial expectations at the start of the year, European economies are set to experience weaker performances in 2024. MNCs should account for these dynamics and adjust their expectations and growth objectives to reflect a period of sluggish growth. While the outlook remains cloudy, the worst should be behind us, and the operational environment should be more predictable in 2024 than in 2023. Executives, however, should also note that the divergence between markets and customer segments will remain pronounced and continue to necessitate strategic adjustments to business operations that account for the difference in opportunities through 2024. Customer and market prioritization strategies will thus be an indispensable tool going forward. MNCs should also note that despite the downbeat outlook, some markets, especially in Southern and Central Europe are set to outperform, and while these are unlikely to offset the weakness in large markets, such as Germany, they can offer some new business opportunities.

Overview

- The German economy contracted by 0.4% YOY in Q3 2023 in line with our expectations and will likely continue to experience a contraction through Q1 2024.

- The French economy outperformed most of its peers and expanded by 0.6% YOY during the same quarter, but a contraction of 0.1% in QOQ terms suggests that activity will slow notably through Q1 2024.

- The UK economy contracted by 0.3% MOM in October 2023 on the back of rising borrowing costs and weakness in consumption.

- Eurozone PMI increased slightly to 44.2 in November 2023 from the 43.1 reading in October on the back of a slower decline in new orders.

- Consumer confidence in the eurozone has also seen a mild improvement but remains in deeply negative territory at -16.9 in November 2023.

Our View

In January 2023, 2023–2024 expectations assumed a broad normalization in activity in Q4 2023 and sharper contraction in activity through Q2/Q3 2023. European economies, however, proved more resilient, especially Southern European markets, such as Spain and Italy, with the former seeing a substantial upward revision throughout the year. The ongoing slowdown across the eurozone resembles a soft-landing scenario instead of the initially feared sharp contraction. The higher-than-expected tightening by both the European Central Bank and the Bank of England through the summer months of 2023, however, highlights the fact that the weakness is set to extend, and the growth pace in 2024 will be much milder than initially expected, with weak activity likely to persist through Q1 2024 and be followed by a period of stagnation.

Despite these challenges, we still expect 2024 to be mildly better than 2023, and the gradual recovery in industrial and consumer confidence through the eurozone supports the assumption that the worst of the shock should be behind us. Monetary policy cuts in mid-2024 should also be relatively quick to transfer to the real economy and have a positive effect on demand and investment dynamics through the latter half of 2024. Overall lending rates will, however, remain elevated for longer and continue to prevent a further acceleration in demand. While a more conservative fiscal policy throughout the continent will also add to the ongoing operational challenges, overall policymaking should be more predictable, which, coupled with subsiding inflation, should alleviate some of the structural challenges that European markets are experiencing.

At FrontierView, our mission is to help our clients grow and win in their most important markets. We are excited to share that FiscalNote, a leading technology provider of global policy and market intelligence has acquired FrontierView. We will continue to cover issues and topics driving growth in your business, while fully leveraging FiscalNote’s portfolio within the global risk, ESG, and geopolitical advisory product suite.

Subscribe to our weekly newsletter The Lens published by our Global Economics and Scenarios team which highlights high-impact developments and trends for business professionals. For full access to our offerings, start your free trial today and download our complimentary mobile app, available on iOS and Android.